The Office for National Statistics (ONS) published its latest official population projections for the UK on Tuesday 28 April 2026, although it stresses that its projections are largely based on past and current trends and cannot predict future changes in international migration, births or deaths.

More people

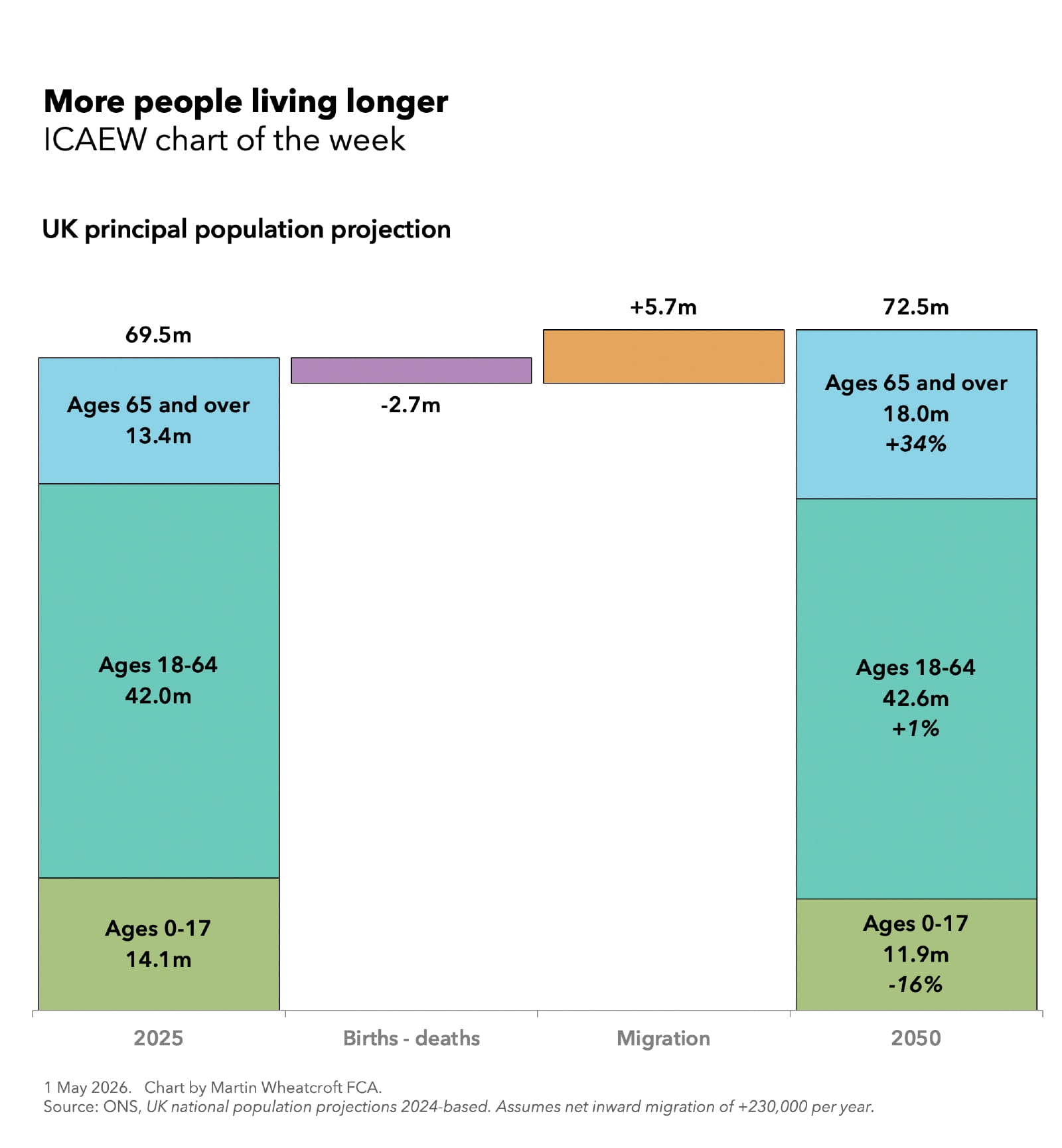

The ONS’s principal population projection forms the basis for this week’s chart, starting with the provisional estimate for the UK population of 69.5m in June 2025. This is projected to reduce by 2.7m from deaths exceeding births over the next 25 years but increase by 5.7m because of net inward migration – a net increase of 3.0m to reach just under 72.5m in June 2050.

This compares with a net increase of 10.6m over the previous quarter of a century (not shown in the chart), starting from 58.9m in June 2000, adding 3.3m from births exceeding deaths and 7.3m from net inward migration to reach 69.5m in 2025.

The net increase of 3.0m is equivalent to population growth of 4% over the next 25 years or an average annual increase of just under 0.2% per year (compared with 18% or approximately 0.7% a year over the previous 25 years to mid-2025).

The projections for births and deaths are based on existing trends, with a falling fertility rate projected to result in 16.0m births over the next quarter of a century (down from 18.4m in the previous 25 years) while more people in older age groups means the number of deaths is projected to total 18.7m (up from 15.1m between 2000 and 2025).

Projected net inward migration of 5.7m (down from 7.3m over the previous 25 years) is based on the latest forecast of 138,000 for the year to June 2026 and a long-term assumption of 230,000 a year from July 2026 onwards, equivalent to average of 228,000 over the period (down from an annual average of 294,000 between 2000 and 2025).

The long-term assumption is higher than the 202,000 estimated in the year to June 2025, but is much lower than the 739,000,

906,000 and 624,000 estimated net inflows of people from migration in the years to June 2024, 2023 and 2022 respectively.

The combination of a falling birth rate, a rising death rate and lower net inward migration lead the principal population projection to peak at just over 72.5m in 2054 before declining to 71.3m in 2075 and 68.0m in 2100.

Living longer

Our chart also highlights how the number of people aged 65 or older is projected to increase by 34% from 13.4m in 2025 to 18.0m in 2050. This is significantly greater than the just over 1% projected increase in the working population between the ages of 18 and 64 from 42.0m in 2025 to 42.6m in 2050 and contrasts with a projected 16% fall in the number of children from 14.1m to 11.9m.

According to the ONS, the number of people aged 75 or older is projected to increase by 52% from 6.7m in 2025 to 10.2m in 2050, while the numbers aged over 90 are expected to increase by 123% to 1.4m.

The ratio between the working age population (ages of 18 to 64) and the number aged 65 or more is expected to fall from 3.1 working age people per senior to 2.4 working age people per senior.

Costing more

This change in the demographic makeup of the UK is going to be a huge challenge for the public finances, which are already in a fragile position after a series of economic shocks during the first quarter of the 21st century.

People over the age of 65 generally take out more in benefits than they put in, especially once they become eligible for the state pension, while health and social care costs multiply as people get older. And, while the increase in the state retirement age (to 67 this year and to 68 in the late-2030s or mid-2040s) reduces the percentage increase in the number of state pensioners to 22% (from 12.6m pensioners over the age of 66 in 2025 to 15.4m over the age of 68 in 2050), the pension triple lock policy would, if continued into future parliaments, offset much of that saving by ratcheting up the state pension faster than the rise in average incomes.

The cost of pension credit and housing benefit are also likely to rise as the next generation of over 65s is less likely than current pensioners to receive ‘gold-plated’ final salary pensions or to own their own home outright.

Fewer children and young adults should reduce the cost of the education budget, but this will be offset by a defence budget going in the opposite direction, in line with the new NATO commitment to raise defence spending from 2.0% of GDP to 3.5% of GDP by the mid-2030s. Governments are no longer able to raid the defence budget to find extra money for the NHS as they been able to over the past 50 years.

The plan, to the extent there is one, is to rely on a combination of economic growth, non-pensioner welfare reform, and very tight spending settlements over the next 25 years to keep the public finances under control, if not exactly healthy.

The problem is that economic growth has been stubbornly weak since the financial crisis even before considering current developments, which hopefully are just temporary. Welfare reform is difficult. And deteriorating public services tend to get governments fired.

More people living longer is of course a very good thing.

The challenge for this and future governments is how to find the money that will be needed to pay the pensions, health, social care and other costs that result from that otherwise very welcome trend.

Latest charts

Further resources

ICAEW Community

Public Sector Community

The go-to place for guidance on issues affecting finance professionals working in and with the public sector. With a range of dynamic services, ICAEW provides valuable tools, resources and support tailored to the public sector.

Resources

Economy explainers

ICAEW experts offer simple guides to help understand the technical, economic jargon that is discussed when talking about public finances and the economy.

Find out moreICAEW support

Training and events

Browse upcoming and on-demand ICAEW events and webinars offering support on technical areas, such as assurance, reporting and tax, as well as personal development.

Events and webinars A-Z of courses