Unparalleled insight

The research provides a structured view of how UK mid-tier accountancy firms are responding to a changing operating and regulatory environment. The findings highlight areas of convergence across firms, where challenges are widely shared, as well as points of divergence where approaches, priorities and confidence levels differ.

Consistent with prior years, ICAEW invited Managing Partners and CEOs of UK mid-tier member firms, those with 11 to 249 principals, to take part in the research between February and March 2026. The participation rate was consistent with previous years with 35 firms responding (32%). These firms were broadly evenly split between smaller (up to 20 partners), medium-sized (21–50 partners) and larger (more than 50 partners) size firms in the mid-tier.

ICAEW's research plays an important role in testing assumptions and grounding anecdotes in evidence, helping to validate what firms believe to be true about the market, to identify where pressures are easing or intensifying, and to provide direction as firms look ahead.

Consolidation activity remains high

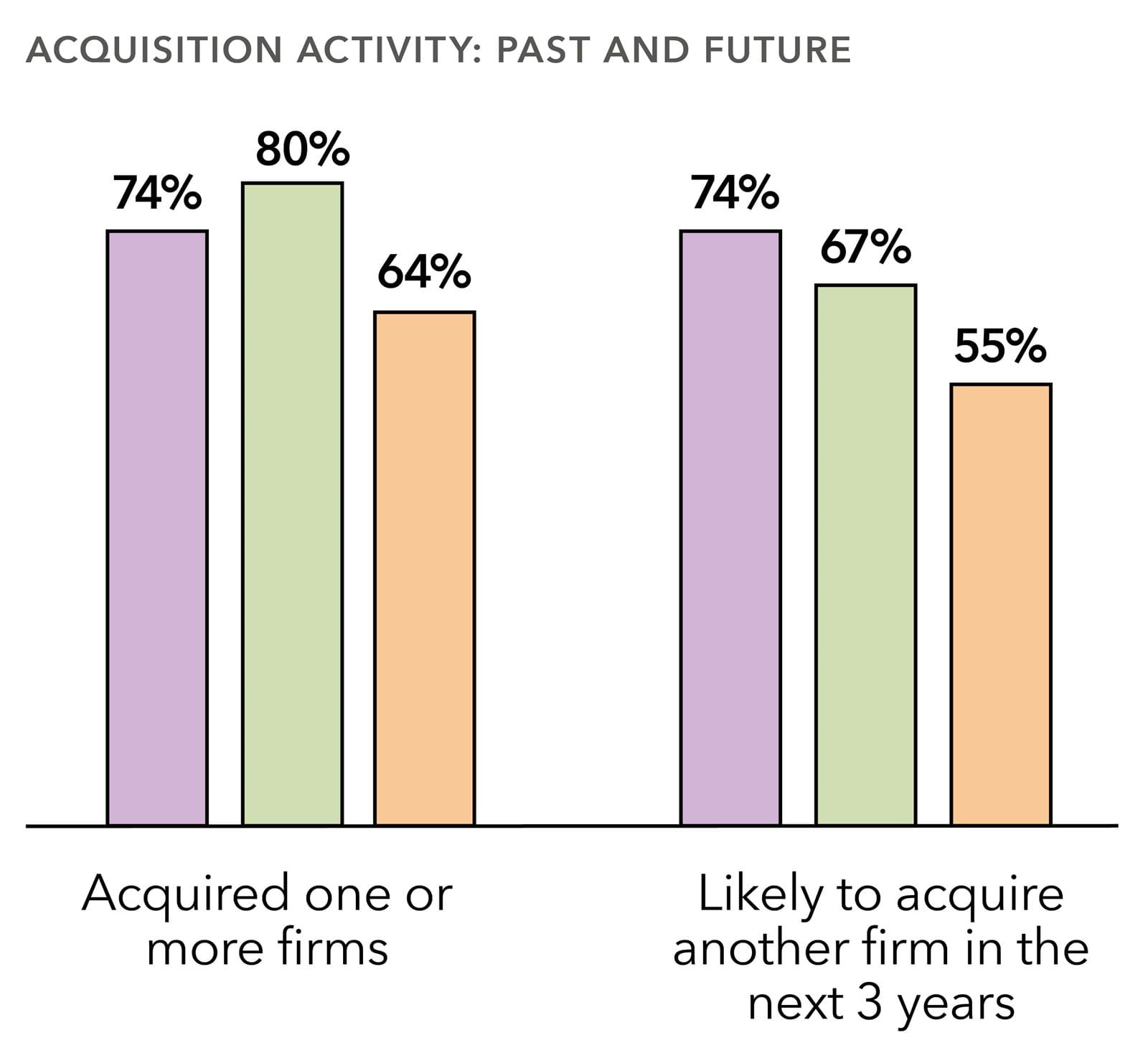

Consolidation continues to be a defining feature of the mid-tier accountancy landscape. Acquisition activity is widespread, with nearly three-quarters of firms reporting that they have acquired another firm, and appetite for further acquisitions over the next three years remaining strong. Larger firms and those with private equity (PE) investment are significantly more likely to be acquisitive.

PE investment has become an increasingly prominent feature of the sector. Nearly half of responding firms are now PE-backed, and for these firms external capital is widely associated with acquisitions, investment in technology and talent, and operational change.

However, PE investment is not an attractive route for all. Only a small minority of independent firms are considering PE investment, potentially suggesting that appetite for PE investment may be reaching a plateau across the firms responding. Independent firms not pursuing PE investment cite cultural and ethical alignment and a desire to preserve their firm’s distinct identity and values as the main reasons.

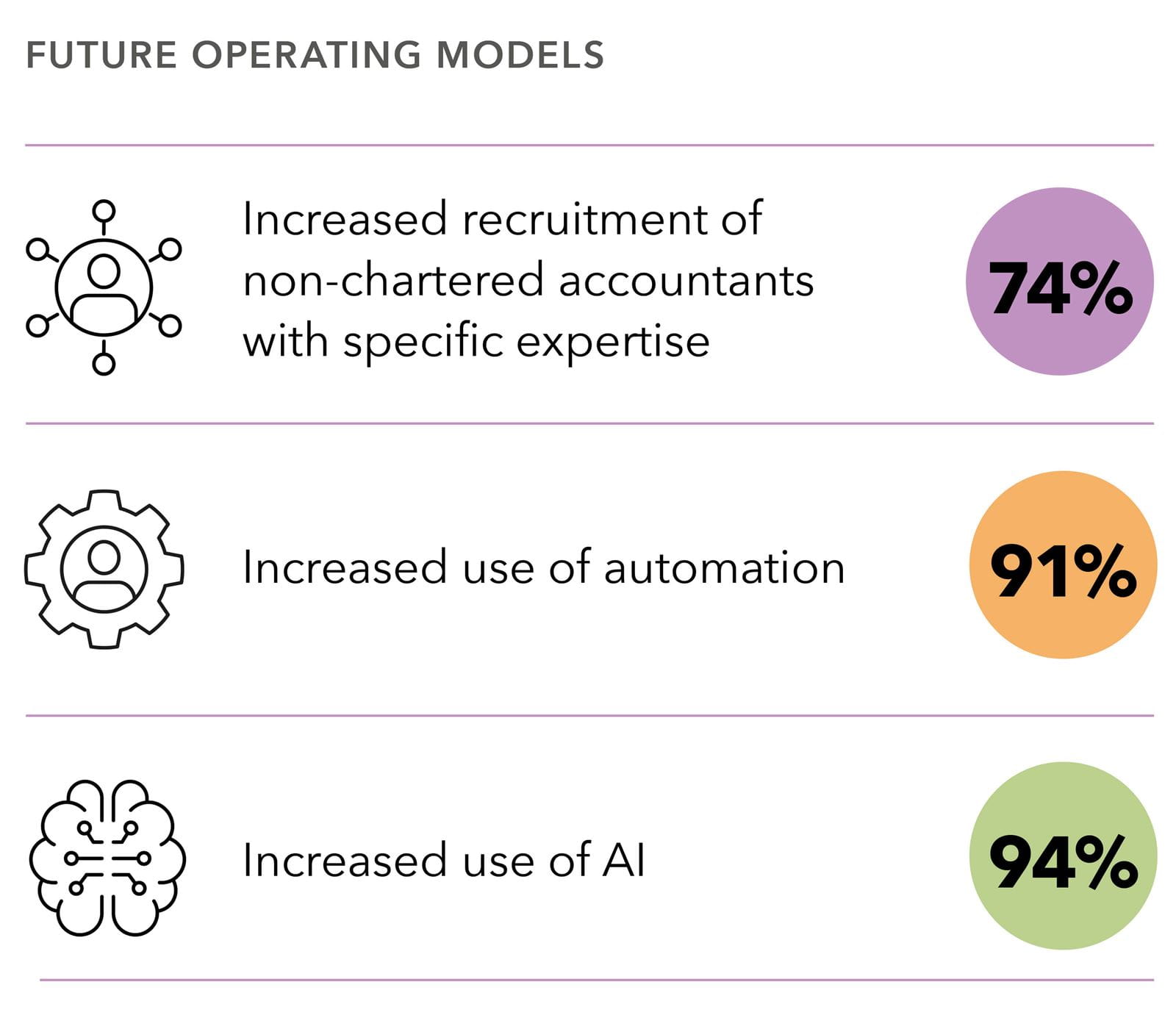

86% of firms have a technology strategy that explicitly includes AI adoption.

AI and operating models

The impact of technology, particularly AI, is woven throughout the 2026 findings. Almost all firms agree that technology plays a key role in delivering their strategic objectives. Most regard themselves as early majority adopters of AI and believe they are adopting at the right pace.

AI use is already widespread across firms, spanning core service lines as well as for internal knowledge management and client support functions. However, AI use is typically moderate rather than extensive.

Firms overwhelmingly expect both AI and automation use to increase significantly over the next three years and firms have indicated that they will increase the recruitment of specialist expertise, particularly in data and technology-related roles. However, relatively few firms feel confident in assessing the impact AI will have on their workforce, with only 17% expressing confidence in this area.

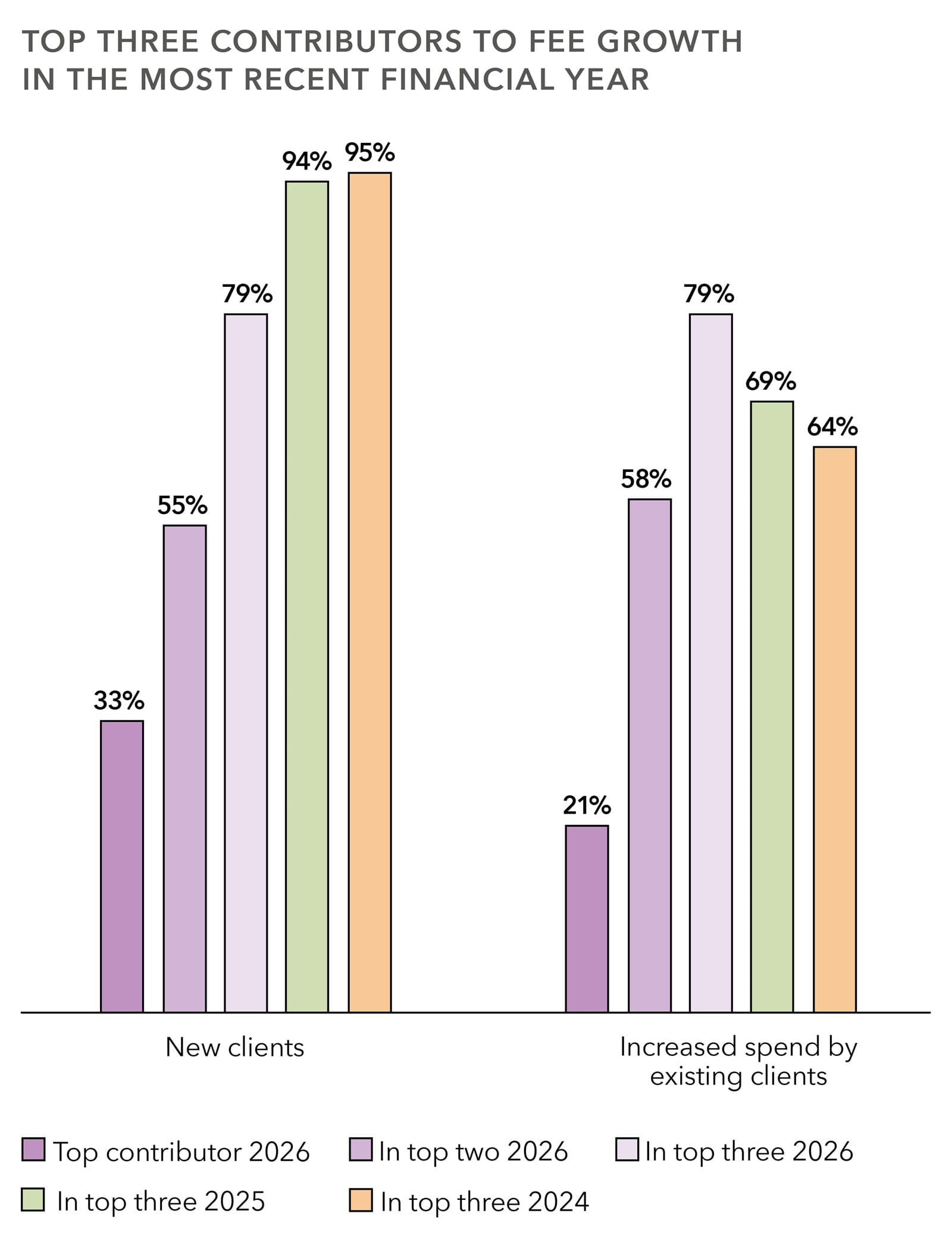

94% of firms reported fee growth in their last financial year.

Growth remains strong

Growth across the mid-tier continues, with almost all firms reporting fee growth in their most recent financial year, and the vast majority expecting growth to continue over the next three years.

The top factors contributing to this growth are increased spend from existing clients, a factor which has been trending upwards since 2024, together with growth in fees from new clients, a factor which conversely has fallen in prominence since 2024.

Service line offerings remain relatively stable. Tax, accounting, audit and advisory continue to dominate, with sustainability-related services developing more gradually. Several firms identify further opportunities for growth in their existing core audit and tax service lines in the future.

When asked about macro trends driving change in the profession, the impact of regulation was cited less frequently in 2026 than in previous years. However, firms continue to identify it as a constraint on growth. Audit regulation is most often highlighted as challenge, together with anti-money laundering requirements and employment regulation.

The future of the profession

The nature of roles, skills and career pathways is changing, but confidence in the long-term relevance and value of the profession remains strong.

The findings show that firms have a high level of confidence in the future of the profession, with most agreeing that accountants will remain in demand but for a redefined profession where the focus of roles will shift towards judgement, systems thinking and ethical oversight.

Firms view AI as an opportunity to enhance their service offering; however it will also lead them to reshape their workforce models with an anticipated reduction in more junior roles and a broadening of capabilities at a senior level.

Very few believe that the profession will be less attractive as a result of being replaced by AI.

The future accountant

- 83% agreed that demand for accountants will continue, but for a redefined profession.

- 83% agreed that the role of the accountant will pivot from compliance and reporting to judgement, systems thinking and ethical oversight by 2030.

- 71% agreed that AI will enable firms to move up the value chain in terms of their service offering.

- 68% agreed that AI will reduce the need for early career accountants, compress mid-tier roles and require more senior accountants to have broader capabilities.

- Only 12% agreed the attractiveness of the profession will decline with the perception that accountancy will be replaced by AI.

Related content

Previous research

Evolution of mid-tier accountancy firms

Read ICAEW's previous annual research into how mid-tier accountancy firms in the UK are navigating change and pursuing opportunities.

2024 report 2025 reportSupport

Latest practice news

Stay informed with the latest practice news from ICAEW. The Practicewire Newsletter is tailored to keep sole practitioner and practices up to date with the latest developments.

Find out moreSupport

Practice resources

Access all the technical content and guidance, latest news and events to support your practice.

Explore the hub