The verdict up front

Auditing standards require the auditor’s opinion to be presented up front, but some auditors are going further to ensure readers aren’t left hunting for the key takeaway. Right from the opening line of the opinion section, they’re making their conclusion leap out in bold boxed text: “Our opinion is unmodified.” It’s simple, yet effective, cutting straight to what matters most.

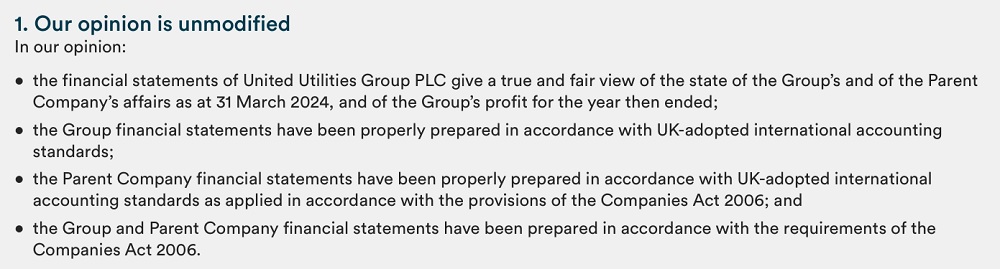

Example 1: Bold headings

Impossible to miss – a bold heading highlights the opinion in the opening line, as illustrated below.

Materiality made simple

Materiality is one of those audit buzzwords that often leaves readers scratching their heads. But it doesn’t need to be. Some auditors' reports are leaving behind the dense explanations and opting for clear tables that lay everything out at a glance.

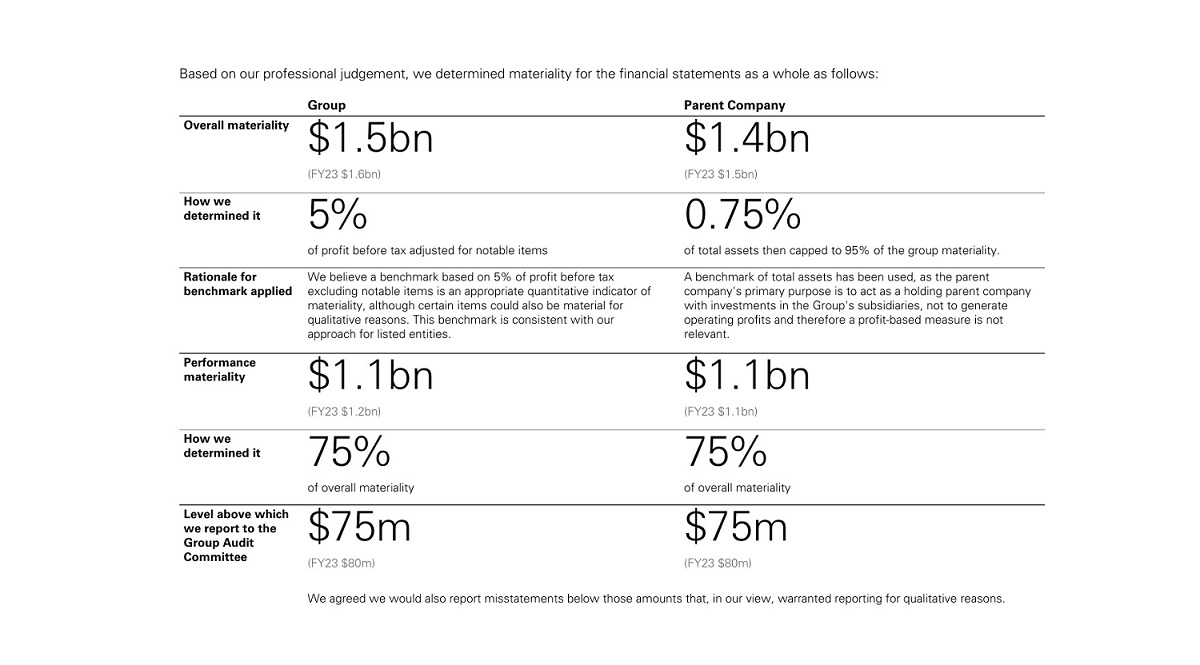

Example 2: Straightforward subheadings

Clear subheadings provide effective signposting, helping direct readers to easily understandable definitions for areas such as materiality.

Concise sentences and an organised layout help users understand the criteria for determining materiality without being overwhelmed by unnecessary details. Presenting materiality in this way, along with simple explanations of how these figures were set and, crucially, why, cuts through the confusion.

Example 3: Contrasting typography

Vital information is provided in a concise, visual format that is easy to digest.

Easy to navigate

One of the requirements of the auditing standards is for KAMs to refer to the relevant disclosures in the annual accounts. But jumping between the auditor’s report and the rest of the accounts can feel like a game of hide and seek. While the ultimate responsibility for the annual report sits squarely with the company, not the auditor, there’s a growing trend towards genuine collaboration in pursuit of greater clarity.

Some companies are now weaving the auditor’s report into the annual report by employing the same tools and design principles found throughout the accounts. These reports come with handy click-throughs and tabs, allowing readers to navigate straight to the relevant section of the annual report without losing their place.

Example 4: Interactive page navigation

Tabs provide user friendly click-throughs between sections for easier navigation.

Breaking the mould

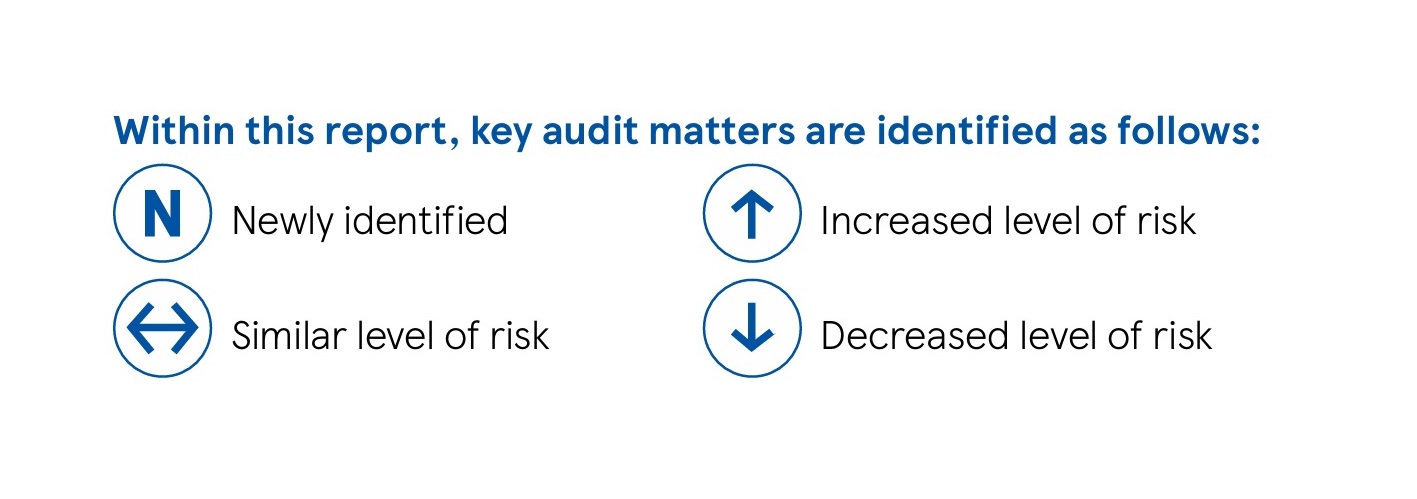

Traditional auditors' reports can be tough going and test even the keenest reader’s stamina. But the landscape is changing, with audit firms injecting some much-needed flair into their reports. ICAEW’s Auditor Reporting Lab has kept a close eye on some of the techniques cropping up.

Take the use of symbols, for example. Instantly recognisable icons flag up when there’s a new risk or the profile of an existing KAM has shifted, making it easy to spot what’s new at first sight. It’s a simple tweak that transforms the auditor’s report into something altogether more inviting.

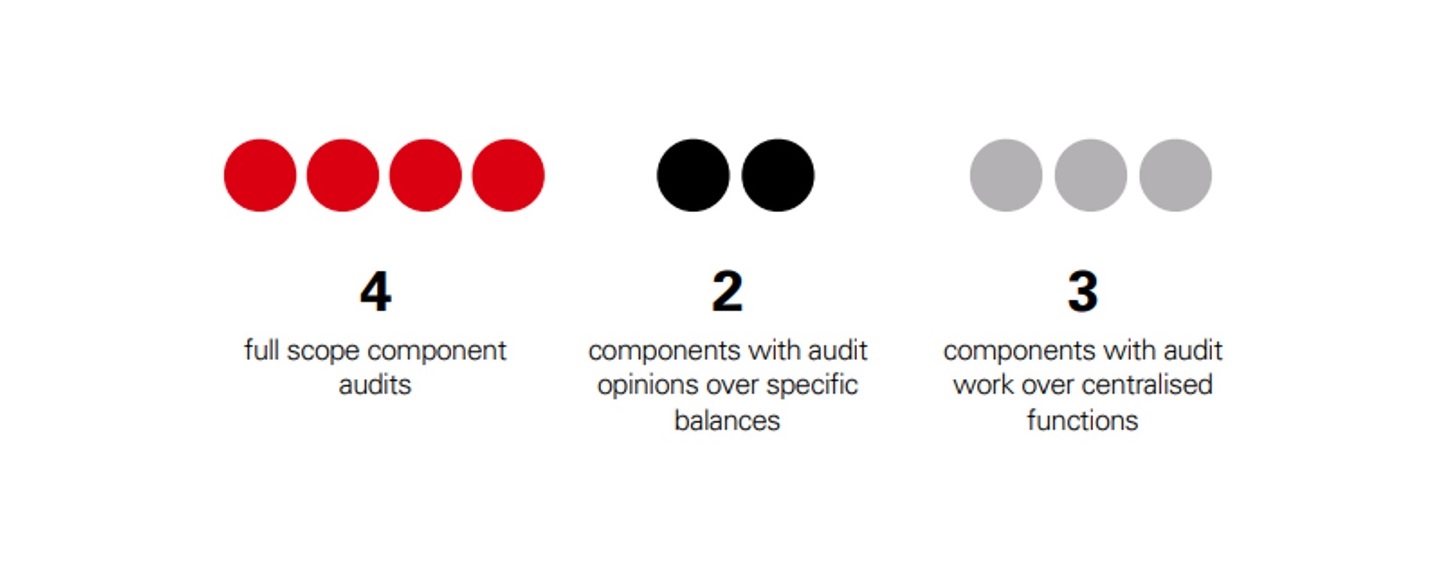

Example 5: Visual aids

Diagrams, symbols and keys, for example, do the heavy lifting and can help to elevate the report and provide a clear overview.

We’ve noticed that some sections, such as the audit approach and audit scope, are particularly ripe for innovation — and some examples are not just informative, but eye-catching. The best reports serve up crucial details in easy-to-grasp snapshots that draw the reader in.

Example 6: Visual snapshots

Highlighting crucial details in easy-to-grasp snapshots to draw the reader in.

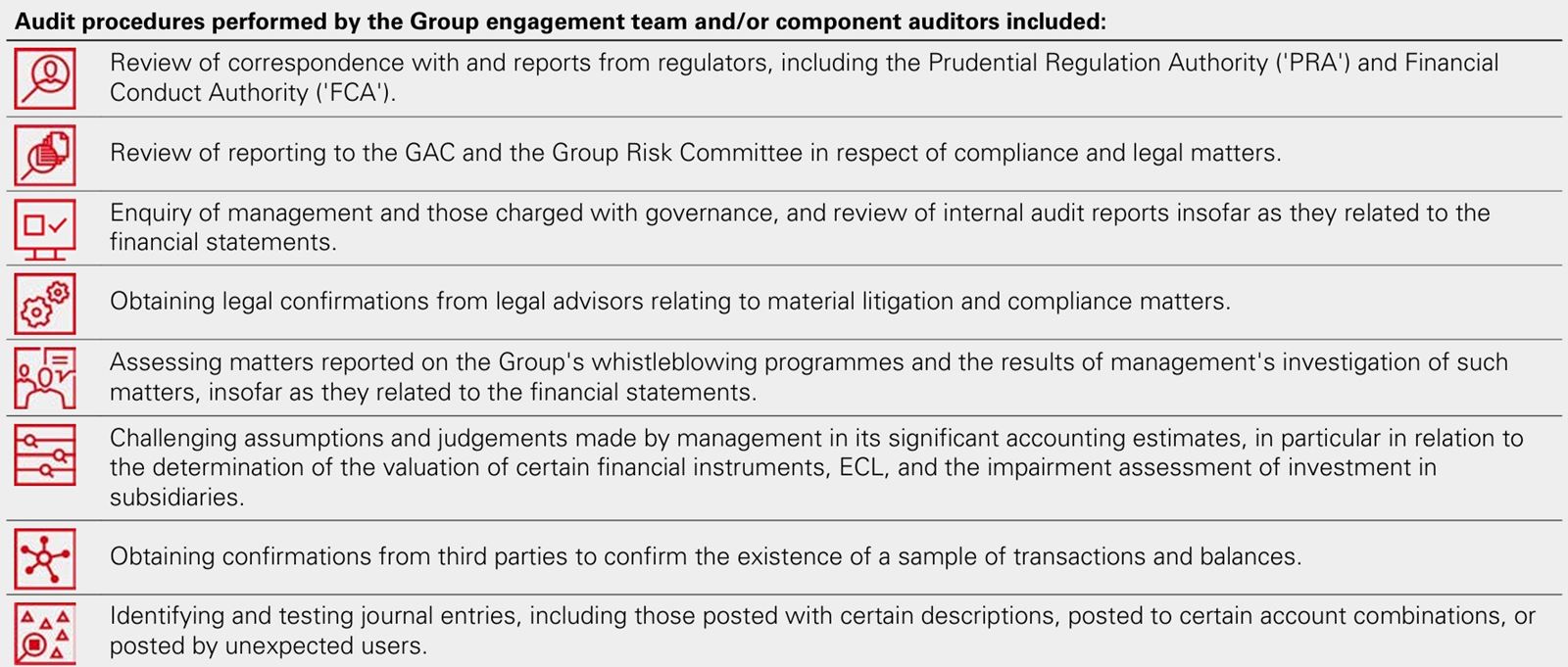

Example 7: Succinct format

Rather than burying procedures about, for example, non-compliance with laws and regulations, in unreadable blocks, some reports now opt for snappy tables, visuals and no-nonsense language.

Some reports have also included QR codes that take the reader straight to the FRC website for full details of the auditor’s responsibilities, instead of the hyperlink in the small print. It draws attention to the existence of the link and is useful in printed copies – just a smartphone scan away.

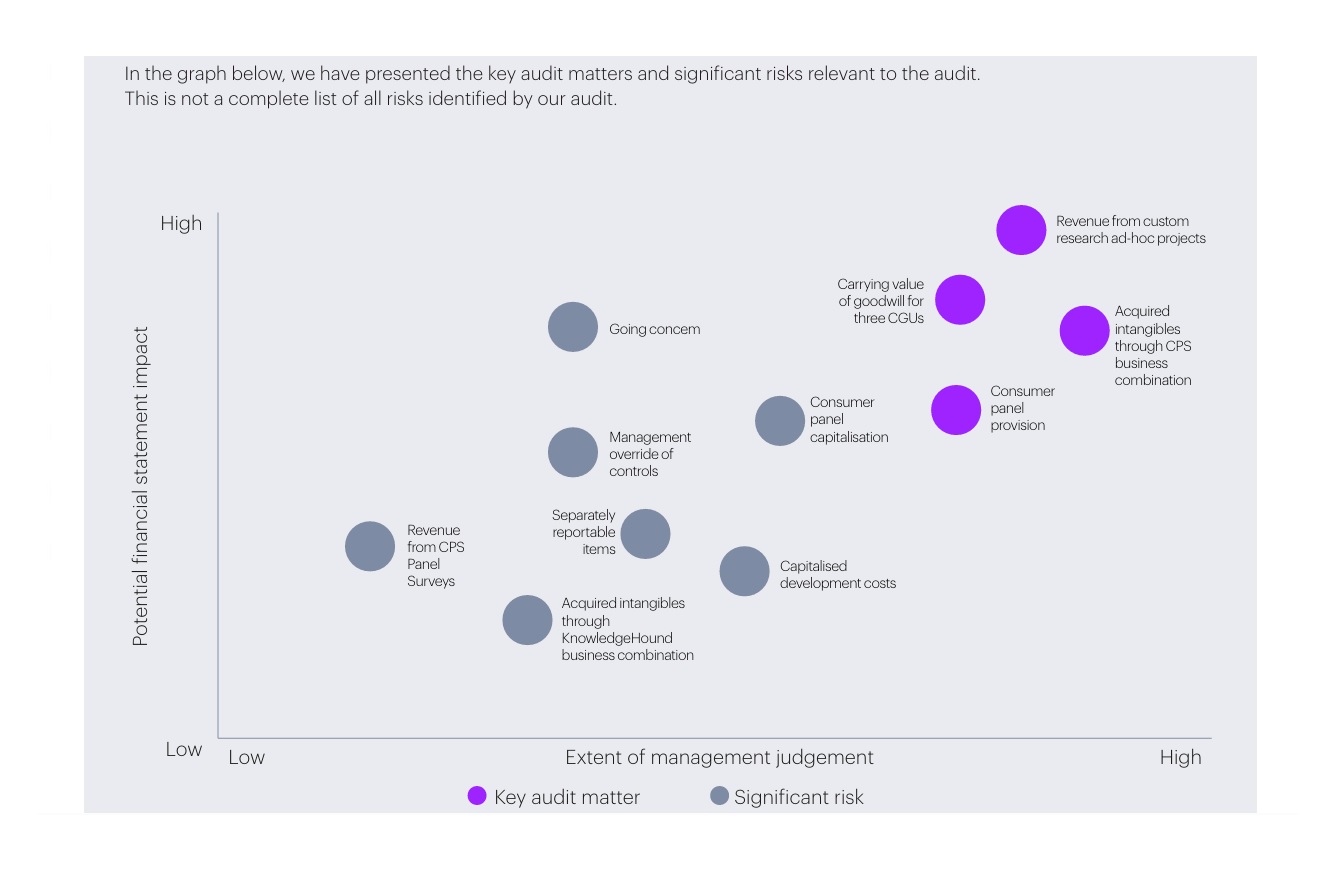

Example 8 : Simplify complex topics

Diagrams and graphs help to break down complex topics, like the identification of significant risks and KAMs, making them easier to grasp.

Clear, concise and cutting through the clutter

KAMs are designed to shed light on the most significant issues found during an audit and, naturally, they’re often the first port of call for investors seeking insights. Yet, for all their intended value, KAMs often present a challenge: spanning several pages and packed with detail.

But some auditors are now splitting KAMs into clear sections with neat layouts. Effective subheadings and signposting, for example, to 'areas of particular auditor judgement', 'our results' and 'communications with the Audit Committee', help readers to more easily find what they need.

Example 9: Easy to follow sections

Layouts divided into simple, clear sections make KAMs and materiality easier to navigate and comprehend.

The use of boxed callouts, pops of colour, bullet points and bold type guide the readers’ eyes to the key information. It’s often the subtle aspects of formatting that can make a real difference.

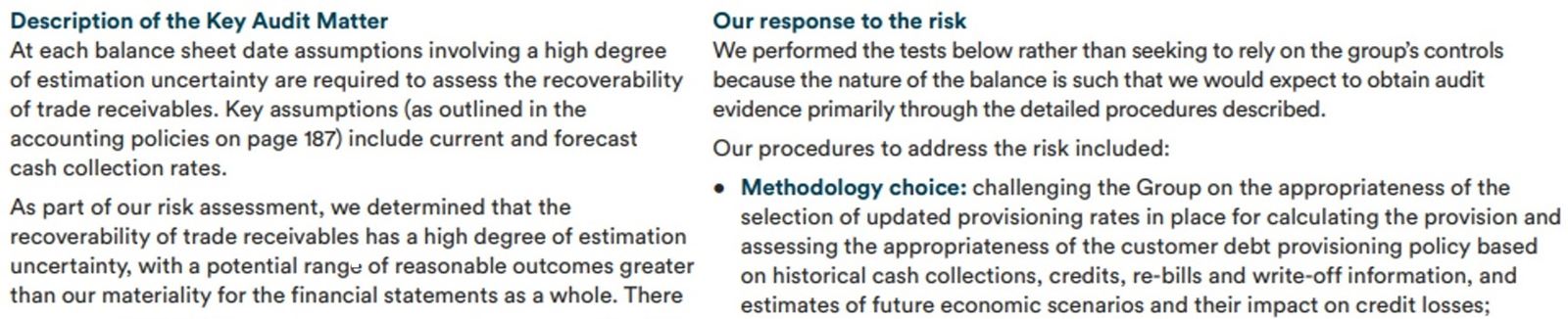

The auditor’s approach to addressing the risks in each KAM can be a lengthy statement, often with pages of catch-all procedures that sometimes leave readers none the wiser. But rather than serving up an inventory of tests performed for each assertion, some auditors are taking a step back with reports that just pinpoint the specific audit procedures tailored to address each particular risk.

Example 10: Clear, focused responses

Crisp commentary provides readers with confidence that the risks have not only been identified but addressed with well-judged responses.

Assessing management’s judgements

An important question for investors is just how rigorously auditors are probing the decisions made by company management. Some auditors' reports are now revealing more about how auditors have interrogated management’s assumptions, explaining exactly what has been done to challenge them and just how resilient those assumptions are when prodded. Whether it’s stress-testing the sensitivity of an impairment model or grilling the robustness of future projections, some auditors' reports are now telling the story of how those numbers were put to the test (see also The use of experts).

Example 11: Explaining procedures

How auditors challenged management’s assumptions.

Example 12: Giving the auditor's perspective

The auditor’s views on management’s judgements.

What’s changed?

Shining a light on how this year’s audit approach differs from the previous year, and explaining exactly why, offers readers real, practical insight into the work auditors have carried out. What prompted a tweak in procedures? Has a new risk emerged? By explaining these differences, such as the difference in the performance in cash generating units year on year, auditors' reports don’t just tick a compliance box, they provide greater clarity, helping readers understand the rigour and direction of the audit process.

Example 13: Comparisons with the previous year

How and why the audit approach has changed.

Example 14: The removal of a KAM

How the risk profile has changed.

The use of experts

Some auditor’s reports now make a point of explaining exactly how experts have been used, flagging not just where specialists were involved, but why they have been used. Was it a quick consult, or did the experts play a pivotal role? By providing this level of detail, reports become more informative, and readers gain invaluable context about the audit’s depth and rigour. It means that investors aren’t left in the dark because now they can see where specialist insight has shaped the audit and judge for themselves just how robust the audit process has been.

Example 15: Expert insights

The use of specialists during the audit process.

Conclusions and recommendations

Auditor reporting is evolving, with some auditors transitioning away from conventional, text-heavy auditor’s reports. The integration of design elements, such as clickable navigation and the use of symbols, tables, and diagrams, enhances both the navigability and readability of auditor’s reports. Many of the most helpful auditor’s reports contain KAMs that are thoughtfully crafted to focus on details most important to investors and are presented in a way that makes them easy to understand.

We encourage auditors to place readability at the heart of their auditor’s reports. By embracing visual aids and adopting straightforward, succinct language, auditors can ensure that key insights are communicated effectively for all stakeholders. By doing so, auditors can help set new standards for transparency and user engagement, ensuring their reports remain relevant and impactful in an age where information is everywhere and attention spans are short.

Example reports

Please note the examples in this article are extracts for illustrative purposes only.

Auto Trader Group plc Annual Report and Financial Statements 2024 – KPMG LLP

HSBC Holdings plc Annual Report and Accounts 2024 – PricewaterhouseCoopers LLP

JD Sports Fashion Plc Annual Report & Accounts 2025 - Deloitte LLP

RM plc Annual report and financial statements for the year ended 30 November 2024 – Deloitte LLP

Serco Group plc Annual Report and Accounts 2023 – KPMG LLP

SSE Annual Report Financial Statements 2024 – Ernst & Young LLP

Tesco PLC Annual Report and Financial Statements 2024 – Deloitte LLP

YouGov plc Annual Report & Accounts 2024 – Grant Thornton UK LLP