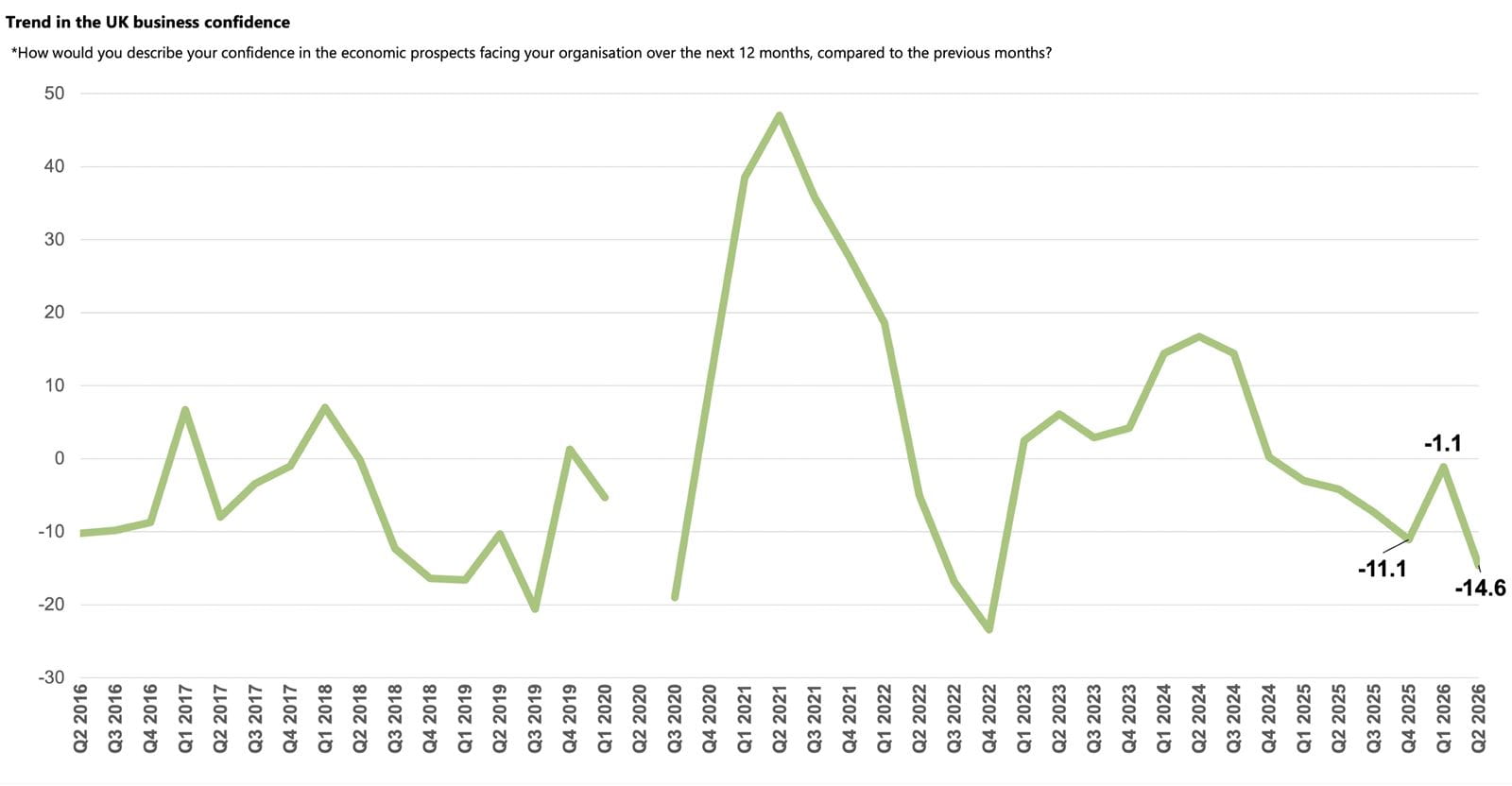

The latest national Business Confidence Monitor (BCM) shows that the Iran War significantly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

Key points

- The Business Confidence Index dropped to -14.6, the lowest score since Q4 2022 with geopolitical risks linked to the Iran War the most widely cited growing challenge to performance.

- Annual domestic sales were resilient, but exports growth slowed, and companies have revised down their expectations for the year ahead for both compared to the previous quarter.

- Input costs rose sharply and selling prices edged up, with businesses planning to increase their prices at a similar rate next year. Profits growth also dropped below the historical norm.

- Alongside geopolitical risk, energy costs and labour costs are the most prevalent growing challenges and, while less prominent, reports of late payments reached a five-year high.

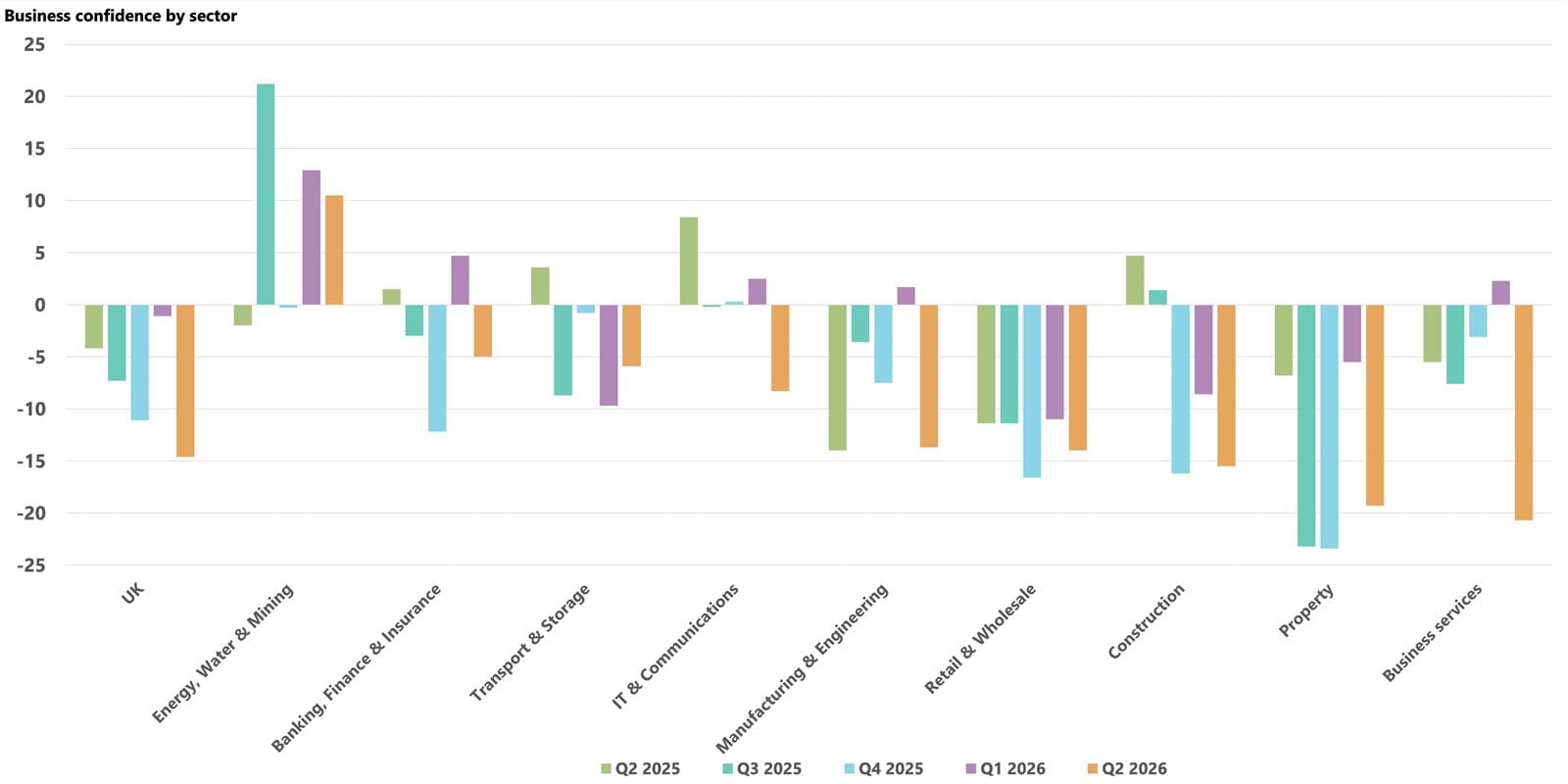

- Confidence deteriorated in most sectors and most have negative scores. Business Services is the least confident, while Energy, Water & Mining is the only sector with a positive score.

Confidence overall

The Middle East conflict drives a sharp decline in UK business confidence.

- Business confidence dropped back into deep negative territory, falling to -14.6 and its lowest level since Q4 2022, amid heightened global uncertainty and rising costs.

- Companies have revised down their expectations for domestic sales for the year ahead, with exports growth also impacted.

- Sentiment is negative in eight of the nine sectors included in the survey, and is lowest in Business Services, Property and Construction but strongest in Energy, Water & Mining.

Business sentiment fell sharply following the outbreak of the Iran War at the end of February and the subsequent impact on energy prices, with the confidence score sinking to -14.6 in Q2 2026, its lowest reading since Q4 2022 and down significantly from last quarter (-1.1). The BCM score has now been in negative territory for six consecutive quarters, the joint-longest period since the global financial crisis, matching the tally recorded for Q2 2018 to Q3 2019.

The decline in confidence was clearly influenced by the increased uncertainty caused by the Middle East conflict, with geopolitical risk the most widely cited growing business challenge during the quarter. For many businesses, the conflict had little immediate impact on domestic sales, in fact they edged up to 3.6% in the year to Q2 2026, the highest annual rate since Q3 2024 and further ahead of the historical norm (3.1%). However, businesses downgraded their expectations for the coming year compared to last quarter, with domestic sales now forecast to grow by 4.7%, down from 5.4% reported in Q1 2026.

Exports growth dipped in Q2 2026, with annual expansion slowing to 3.1% and only just ahead of the historical norm (3.0%). Forecasts for the year ahead were also nudged down to 4.0% from 4.1% last quarter, with businesses anticipating weaker international demand as the Iran War dragged on throughout most of the survey period.

Confidence was negative in eight of the nine sectors covered by the survey in Q2 2026. Business services (-20.7) recorded the lowest score overall. This is the sector’s lowest sentiment score since Q3 2019, with confidence switching from positive last quarter to negative this quarter. Both IT & Communications (-8.3) and Manufacturing & Engineering (-13.7) also reported their confidence falling from positive into negative territory between Q1 2026 and Q2 2026.

Meanwhile, sentiment remains deeply entrenched in Construction (-15.5), Property (-19.3) and Retail & Wholesale (-14.0), with the latter two sectors each recording their seventh successive negative score. Transport & Storage was the only sector to record a rise in confidence, edging up to -5.9 from -9.7 last quarter, while Energy, Water & Mining was the only sector to record a positive score at +10.5.

Business challenges

Geopolitical risk dominates business challenges as concern about labour costs and energy cost issues rise.

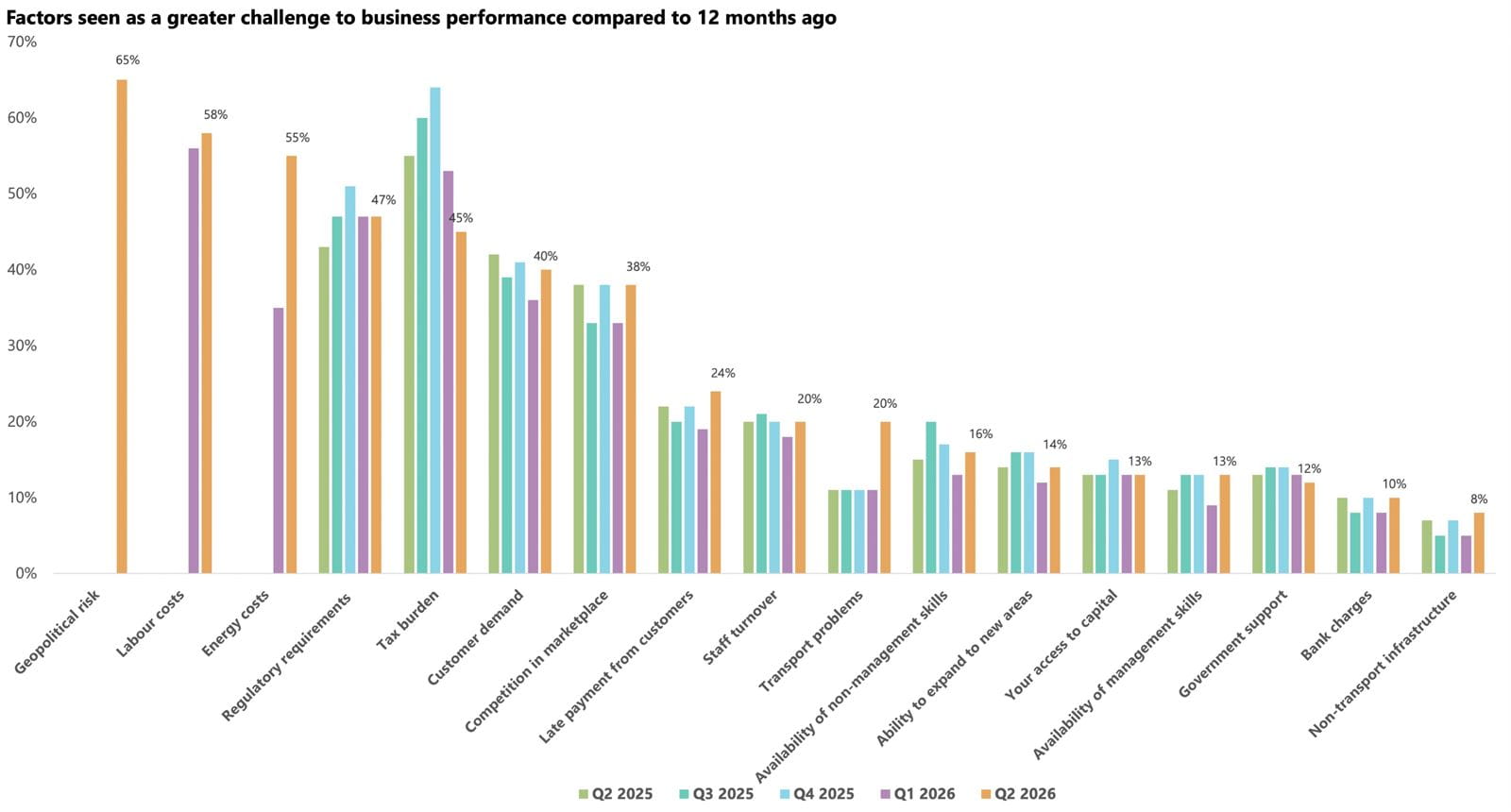

- Geopolitical risk was the most widespread growing challenge for businesses as the Iran War dragged on and, with energy prices rising sharply, energy costs were also reported by over half of companies.

- Labour costs were the second most prevalent growing challenge, edging up from the previous quarter.

- Ailing confidence was also underpinned by rising concerns about customer demand and late payments, while regulatory challenges remain above their historical norm.

Geopolitical risk was the most widely cited growing challenge for businesses in Q2 2026, reported by 65% of companies. This was the first time the challenge was included in the survey, with the high proportion reflecting the rising international uncertainty as the Middle East crisis rumbled on throughout the survey period. The resulting energy-price shock prompted 55% of businesses in the survey to report energy costs as a growing challenge, up from 35% in Q1 2026. A rise in transport problems to 20% in Q2 2026, from 11% across recent quarters, likely represents the impact of the closure of the Strait of Hormuz on distribution and supply chains.

Labour costs (58%) was the second most common growing challenge in Q2 2026, edging up slightly from last quarter. Transport & Storage (80%), Construction, Retail & Wholesale (both 63%) and Business Services (62%), were most likely to report the issue, likely reflecting the rise in the minimum wage in April, alongside previous rises in employers’ National Insurance Contributions. Construction and Business Services companies also reported some of the highest wage rises across all sectors surveyed in Q2 2026.

With companies cutting their sales growth expectations for next year, concern about customer demand (40%) edged back above the historical average (38%), with the challenge most widely reported in Business Services (43%), Transport & Storage (43%), Manufacturing & Engineering and Retail & Wholesale (both 42%).

Growing reports of late payments as a rising challenge could indicate that some businesses are exposed to greater financial stress. The issue was cited by 24% of companies, up on recent quarters, the highest proportion since Q1 2021 and above sector norms for seven out of the nine surveyed. Construction has the highest rates (37%) followed by IT & Communications (30%) and Transport & Storage (28%). Energy, Water & Mining and Retail & Wholesale are the only sectors below their respective historical average reading in Q2 2026. Concerns about bank charges also edged up, most notably in Construction, with the issue reported by 16% of businesses compared to an economy-wide average of 10%.

Regulatory challenges (47%) remain above their historical norm (41%) but were reported by a larger proportion of businesses in certain sectors, such as Business Services (53%) and IT & Communications (46%). In both sectors, they were the highest rates reported since Q4 2018.

Prices

Annual input price inflation rose with companies expecting to pass some of their higher costs on to customers.

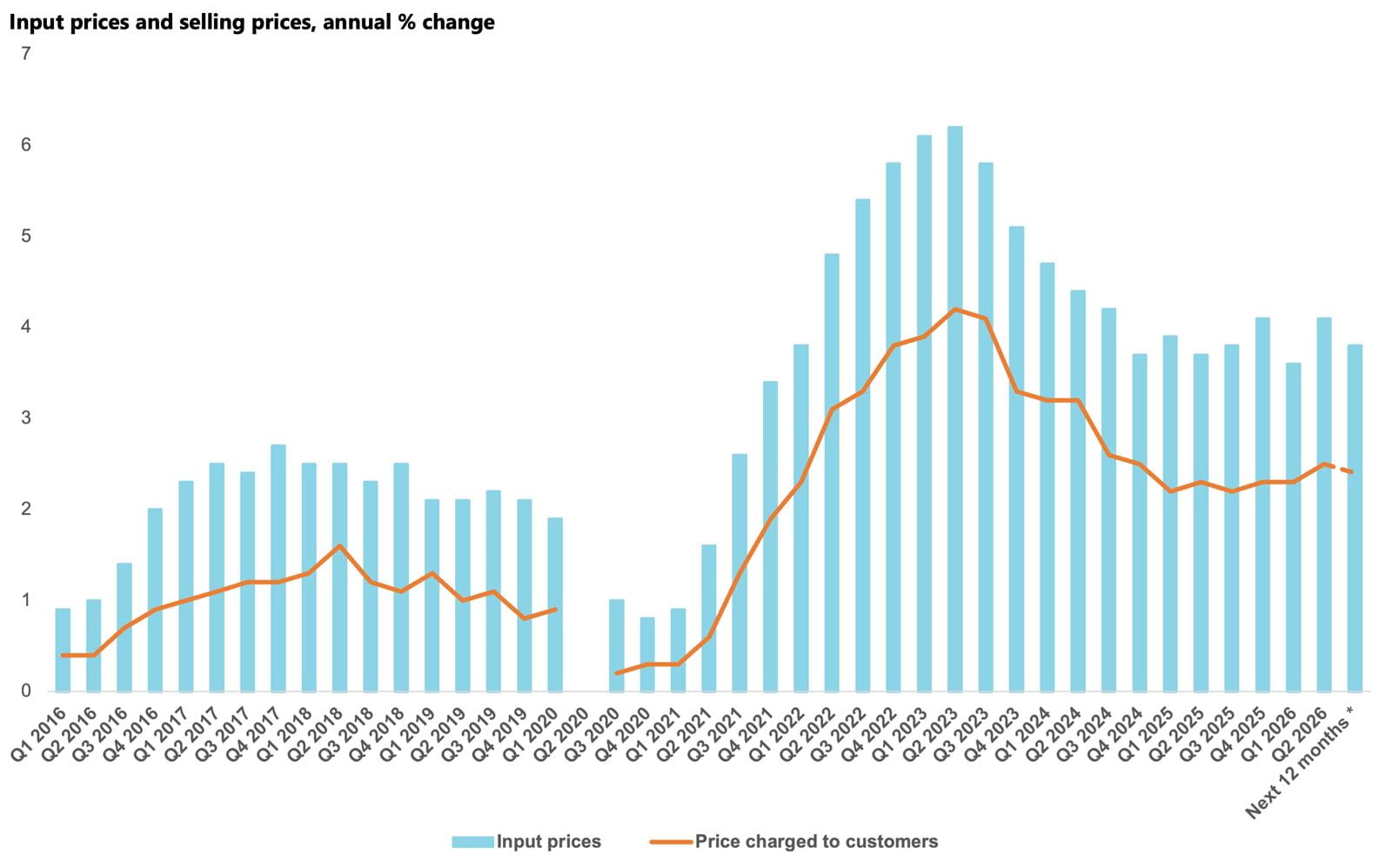

- Annual input price inflation ticked up in Q2 2026, as the outbreak of war in the Middle East caused energy prices to soar and businesses raised their cost inflation projections compared to last quarter.

- Selling price inflation also increased and companies plan to raise their prices at a similar rate over the coming year, stronger than previously projected.

- Most sectors reported higher input price inflation and energy-intensive sectors have the highest selling price forecasts for the coming year.

Businesses reported an increase in annual input price inflation in Q2 2026, rising from 3.6% to 4.1% as the closure of the Strait of Hormuz pushed up oil and gas prices and created significant supply chain bottlenecks. With the increase in energy prices set to filter through to other input costs, companies raised their expectations for year-ahead input price inflation from 3.0% in the previous quarter to 3.8% in Q2 2026, well above the historical norm of 2.7%.

Most sectors reported rising input price inflation in the year to Q2 2026, with the highest rates recorded in Construction and Transport & Storage at 5.1% and 4.9% respectively. Retail & Wholesale was the only exception, with input cost inflation easing to 2.9%, its lowest level since Q2 2021. Even so, it remained marginally above the sector’s historical norm of 2.7%.

While many sectors expect input price inflation to ease over the next 12 months, they also expect it to be stronger than predicted last quarter due to the ongoing conflict in the Middle East. Transport & Storage companies anticipate the largest increase in input costs, reflecting the sector’s exposure to energy prices, with growth of 4.8% projected. At the other end of the scale, Energy, Water & Mining expects the softest increase, with businesses forecasting input cost growth of 2.7% over the next 12 months.

Businesses also reported an increase in annual selling price inflation in Q2 2026, to 2.5%, widening the gap with the historical norm of 1.4%. Companies intend to maintain a similar pace over the coming year and plan to raise selling prices by 2.4%, up slightly on the projection from last quarter (2.3%). The uptick in businesses reporting concern about customer demand this quarter may limit how much of the rise in input costs they can pass to customers.

At the sector level, the sharpest increases in selling prices were reported in Energy, Water & Mining and Transport & Storage, as companies passed higher energy costs on to customers. The reported rises of 4.2% and 4.1%, respectively, were both at least double their historical norms and marked the largest increases since mid-2023. Looking ahead, these two sectors also anticipate the strongest selling price growth over the coming year, with projected increases of 3.6% and 3.2% respectively.

Employment

Employment growth and recruitment prospects edge up as salary inflation expected to continue to ease.

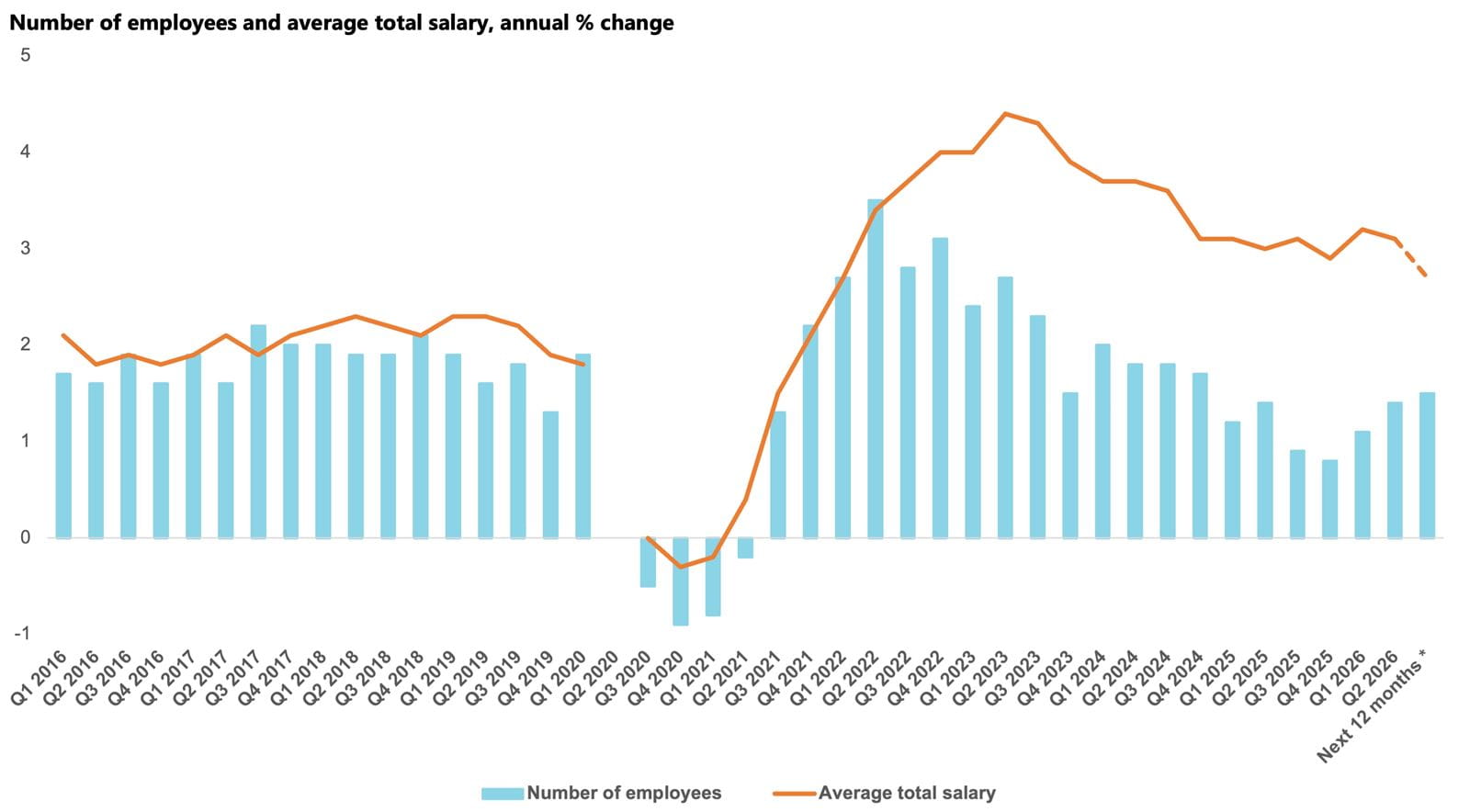

- Employment growth picked up slightly in Q2 2026, rising just above the historical norm with businesses planning to expand recruitment at a slightly faster pace over the coming year.

- Construction companies forecast the strongest employment growth of any sector, while businesses in IT & Communications and Property expect only modest increases.

- Annual salary inflation eased slightly in Q2 2026 but remained above the historical average, with companies expecting further moderation over the coming year.

After a modest uptick in the previous quarter, annual employment growth improved slightly to reach 1.4% in Q2 2026, just above the historical norm of 1.3%. This was the second consecutive uplift in jobs growth, as companies continue to adjust to the higher cost burden from the increase in employers’ National Insurance Contributions (NICs) and April’s rise in the minimum wage, as well as the challenges associated with the Employment Rights Act. Despite heightened global uncertainty, businesses expect to increase headcount by 1.5% over the coming year, marginally above the historical average.

However, there remains wide variation across sectors. Transport & Storage recorded the strongest employment growth of any sector, with headcount rising by 2.9% year on year, nearly triple the sector’s historical norm of 1.0%. At the other end of the scale, Manufacturing & Engineering companies reported employment growth of just 0.1% in the year to Q2 2026. Looking ahead, the largest expansion in employment is expected in the labour-intensive Construction sector, where companies plan to increase their workforce by 2.9% in order to fulfil the marked uplift they expect in domestic sales growth over the coming year. By contrast, greater adoption of AI may be weighing on labour demand in IT & Communications, where companies plan to increase staff numbers by just 0.5% over the next 12 months, less than a third of the sector’s historical norm (1.7%).

After rising by 3.2% in the previous quarter, annual salary inflation nudged down to 3.1% in Q2 2026. While companies expect salary growth will moderate over the coming year, the projected increase of 2.7% is still well above the historical norm of 2.2%. Most sectors expect salary growth either to remain at current rates or to ease over the next 12 months. The two exceptions are Retail & Wholesale and Energy, Water & Mining, both of which tend to employ larger shares of lower-paid workers and both expect modest accelerations in pay growth, to 3.1% and 2.5% respectively.

Profits and Investment

Profits growth drops below the historical norm following the outbreak of war in the Middle East.

- Businesses reported a marked slowdown in annual profits growth in Q2 2026, dropping below the historical norm, as the Middle East conflict hit costs and companies have downgraded their expectations for the year ahead.

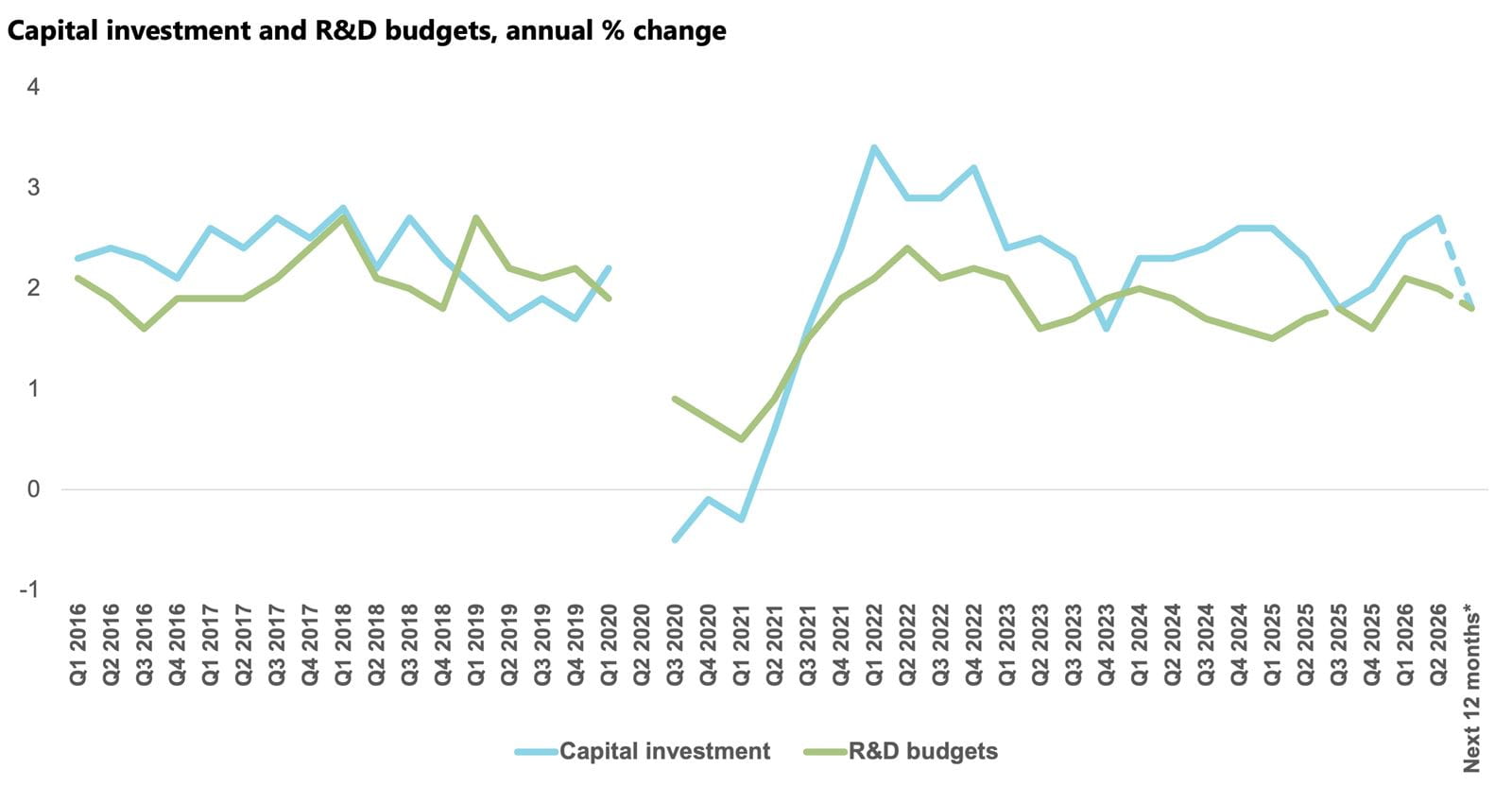

- Capital investment growth continued to improve, though businesses plan to slow both capital investment and R&D budget growth over the coming year.

- Transport & Storage companies reported the sharpest rise in capital investment growth, but companies in the sector expect a marked slowdown in growth over the next 12 months.

After improving in the last two quarters, businesses reported that annual profits growth dropped to 2.8% in Q2 2026, below the historical average (3.1%). The closure of the Strait of Hormuz weakened demand from external markets and caused energy prices to soar, eroding profit margins. While a marked uplift in growth is still anticipated for the coming year, companies have cut their projections from 5.2% in the previous quarter to 4.7% in Q2 2026.

The improvement in profits growth in recent quarters and the Bank of England decision to gradually reduce Bank Rate from 4.75% to 3.75% during 2025 appears to have supported a more favourable investment environment in the year to Q2 2026. Companies reported that capital investment growth rose to 2.7%, the highest rate since Q4 2022. However, increased global uncertainty is weighing on future investment decisions, with businesses planning to moderate growth in the year ahead to 1.8% which, if realised, is lower than the historical norm of 2.1%.

Businesses also plan to curb the growth in their R&D budgets over the coming year. Annual budget growth decreased slightly from the previous quarter in Q2 2026, dropping to 2.0% and companies expect growth to slow to 1.8% over the next 12 months, lower than the historical norm (1.9%).

At the sector level, capital investment growth was strongest in Transport & Storage, with a survey record high of 6.8% reported in Q2 2026. There are several factors that likely contributed to this uplift, including government investment in local transport across England, as well as the shift towards more eco-friendly practices including electric vehicles and route-optimisation software to meet green targets. However, this rapid rate of investment is not expected to be sustained, with companies planning to slow capital investment growth significantly over the next 12 months to just 1.8%, which is below the sector’s historical norm (2.1%). Increased regulation aimed at protecting UK waterways and the continued transition to Net Zero means that Energy, Water & Mining companies predict the strongest investment growth over the coming year, despite plans to slow growth from 5.2% over the past 12 months to 4.5% over the coming year.

Confidence by sector

Sentiment dropped in most sectors, with Business Services and Property the most pessimistic.

- Sentiment was negative in almost all sectors in Q2 2026, with Energy, Water & Mining the only sector to record a positive confidence score.

- Confidence slumped in IT, Manufacturing and Business Services and remained deeply negative in Construction, Property and Retail & Wholesale.

- Geopolitical risk was the main challenge identified by most sectors, but energy costs and labour costs were also significant, particularly for Construction and Transport & Storage.

Business confidence scores have weakened considerably across the majority of sectors and most are in negative territory. The one exception is Energy, Water & Mining, where the index remains in positive territory, but below the previous quarter, as companies reported a sharp uptick in exports growth. Confidence also edged up in Transport & Storage but remains negative. Business services is now the most pessimistic sector with companies recording a slump in profits growth and a weaker outlook for domestic and exports sales, followed by Property, Construction and Retail & Wholesale, sectors that have suffered both prolonged periods of deeply negative sentiment, linked to depressed consumer confidence, and ongoing cost pressures.

Broadly, the deterioration in confidence in Q2 2026 is strongly linked to heightened uncertainty due to the Iran War, with geopolitical risk cited as the main growing challenge in most sectors, with concern highest in Manufacturing & Engineering. Companies in the sector are worried about both the impact on the supply of materials and the demand for their goods overseas. Indeed, Manufacturing was among a small number of sectors that reduced its projections for exports growth for the year ahead compared to last quarter. After edging back into the positive last quarter, confidence in the sector dropped back into negative territory in Q2 2026.

Renewed inflationary pressure following the closure of the Strait of Hormuz is also weighing on sector confidence, and most reported an uptick in annual input cost inflation in Q2 2026 compared with the previous quarter. While most sectors anticipate that inflation will ease over the coming year, almost all have raised their forecasts for year-ahead inflation compared to Q1 2026. Nevertheless, plans to raise selling prices vary by sector. Energy intensive sectors intend to raise their prices faster than average, with Transport & Storage and Energy, Water & Mining planning the sharpest rise in selling prices at 3.2% and 3.6% respectively. Businesses in the Banking, Finance & Insurance sector anticipate the softest rise, with a projected increase of just 1.0% over the next 12 months.

Alongside concerns about geopolitical risk and rising input costs, the issue of labour costs is more prominent among sectors with lower confidence scores. This issue was more widely cited in Business Services, Construction and Retail & Wholesale than average, and was highest in Transport & Storage. The survey also indicates that some sectors may be under increasing financial stress, with late payments concerns highest in Construction, IT & Communications, Transport & Storage and Business Services. Bank charges also edged up as a challenge, particularly in Construction and Property, with these sectors also indicating increased issues accessing capital.

Confidence by region and nation

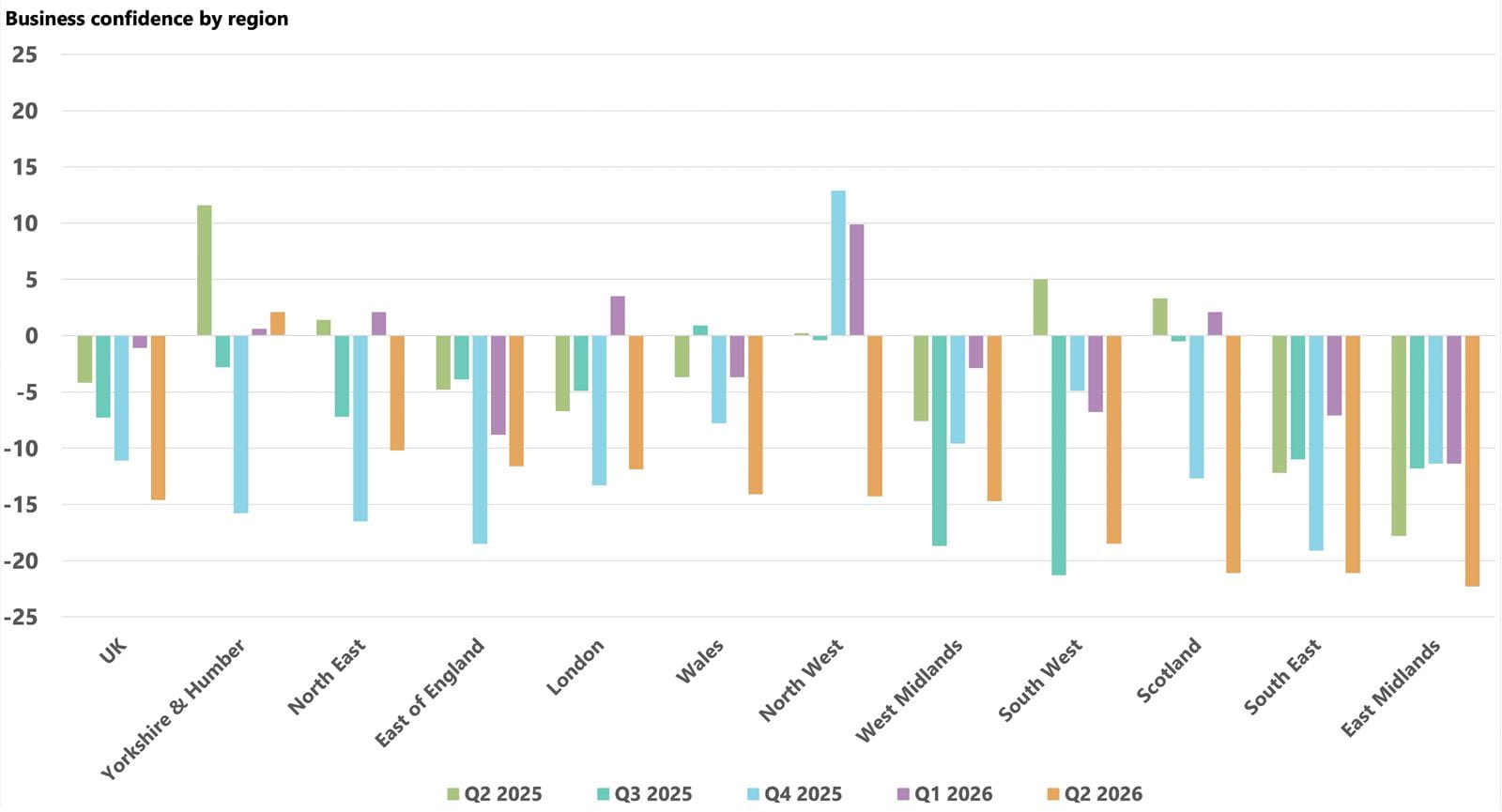

Confidence is negative across all of the UK except Yorkshire & Humber.

- Confidence deteriorated in most UK regions, with only Yorkshire & Humber recording a positive score in Q2 2026.

- The South East and East Midlands were the most pessimistic regions, but the largest decline in confidence score was in the North West.

Sentiment declined in almost all UK regions in Q2 2026 as the conflict in the Middle East continued through the survey period. Confidence in nearly all regions now sits in negative territory, with only Yorkshire & Humber reporting an uplift in confidence to +2.1 compared to +0.6 in the previous quarter, though confidence in the region remains well below its historical norm of +4.6.

Companies in the East Midlands continue to be the most pessimistic in the UK, with confidence dropping from -11.4 in the previous quarter to -22.3. The region’s greater dependence on production and logistics left companies more exposed to the volatile global trading environment and weighed on optimism in the region.

Further analysis of confidence for each region and nation is available in their respective reports on ICAEW Business Confidence Monitor.

Confidence by business size

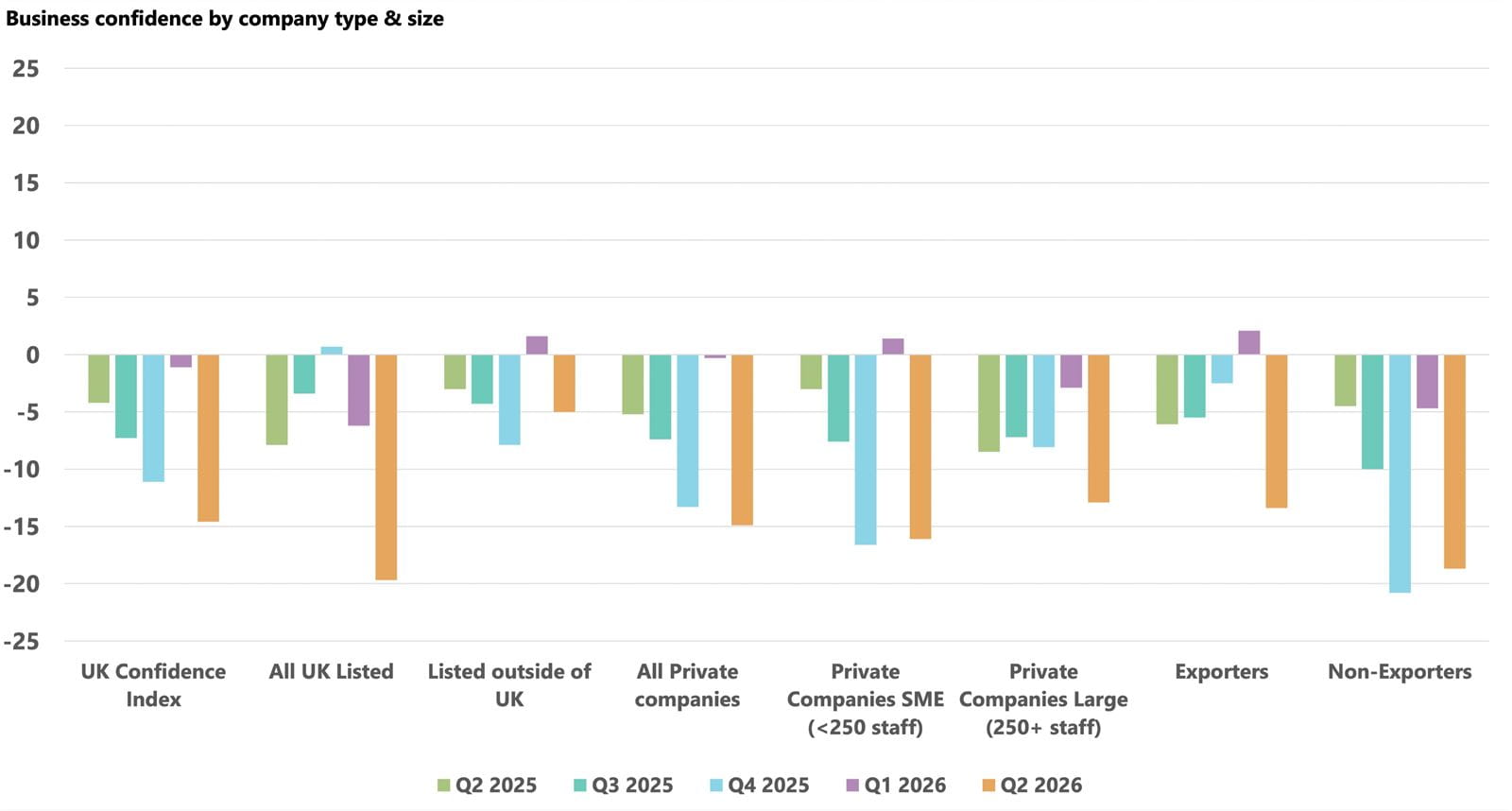

Sentiment was negative across all company types and sizes in Q2 2026, with UK Listed businesses the most pessimistic about the year ahead.

- Sentiment declined across all company types and sizes, with UK Listed companies the most pessimistic.

- Rise in concern about late payments was particularly marked for Private SMEs.

Business sentiment deteriorated across all company types and sizes in Q2 2026. The survey results suggest that the largest decline in sentiment was among Private SMEs, with their Business Confidence Index dropping from +2.1 in Q1 2026 to -16.1 as soaring energy costs impacted small businesses most. The proportion of Private SMEs reporting concern about late payments rose to 27% in Q2 2026, up from 20% in Q1 2026 and above the historic norm (23%). Concern about late payments also rose for large Private companies but to a lesser degree.

Economic and political environment during the survey period

Economic growth falters amid heightened global risk and UK political instability.

- After a strong start in Q1 2026, UK economic growth declined in April as the impacts of the Iran War and the energy-price shock started to weigh on performance.

- Despite the rise in oil and gas prices, CPI inflation eased and interest rates were held at 3.75% for the seventh consecutive month.

- The US-Iran deal agreed at the end of the survey period should ease geopolitical risks but greater political instability with the prospect of a new Prime Minister could fuel uncertainty.

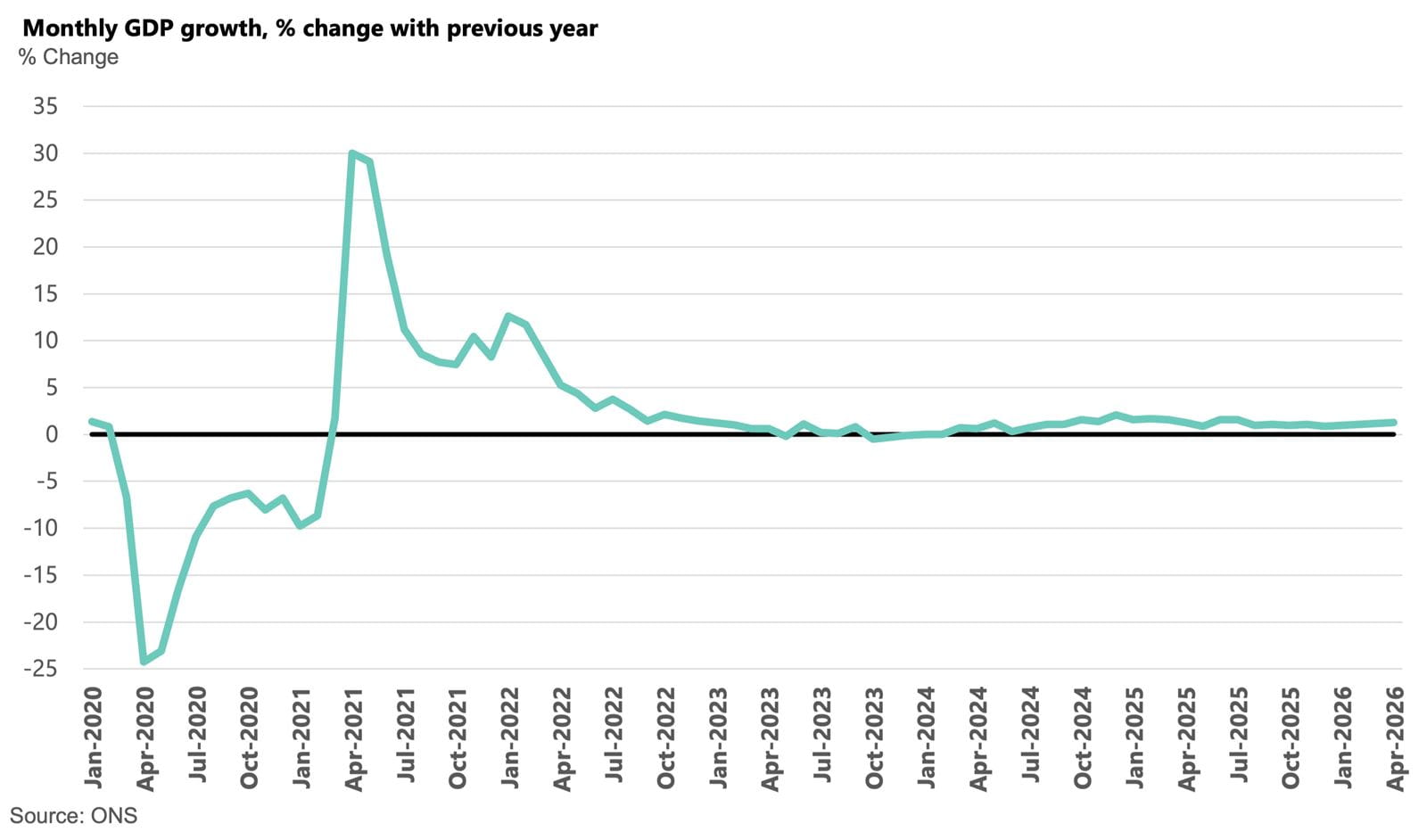

The UK economy got off to a strong start in the first quarter of 2026, with GDP expanding by 0.6% compared to the previous quarter, but the outbreak of the Iran War was evident in the latest monthly GDP estimates, which showed that the economy shrank by 0.1% in April compared to March. The most immediate impact of events in the Middle East was the rise in oil and gas prices. However, despite this, annual CPI inflation decreased from 3.3% in March 2026 to 2.8% in April and May.

The Bank of England’s Monetary Policy Committee has clearly signalled that it is going to take a slow and steady approach to setting Bank Rate and at their meeting in June, voted to maintain the rate at 3.75% for the seventh month in a row. However, the impact of the war on energy prices will begin to feed through into household bills from July when the OFGEM Energy Price Cap increases by 13%, with CPI inflation likely to rise in the near term as rising energy costs filter through.

There were otherwise mixed signals about the underlying state of the UK economy during the quarter. With consumer confidence remaining depressed, retail sales have fluctuated in recent months, with a 1.0% decline recorded in April following growth of 0.6% in March. Retail sales volumes bounced back in May, growing by 1.2% m/m. Labour market data points towards continued cooling, with pay growth slowing to 2.9% in April from 3.1% in March, while employment in May 2026 was 119,000 lower than the previous 12 months.

The tail-end of the survey period coincided with news that Iran and the US had agreed a deal which included the immediate re-opening of the Strait of Hormuz, with oil and gas prices falling accordingly. Domestically however, political instability rose in the build-up and aftermath of the local elections in early May, with both the Labour and Conservative parties suffering significant losses to Reform and ultimately culminating in the resignation of Sir Kier Starmer as leader of the Labour Party. Consequently, the UK will soon have its fifth Prime Minister in as many years, with Andy Burnham likely to take the role this summer.