Key takeaways

- Gradual improvements to the economy in February have been wiped out by the Iran war.

- Energy costs are now a big concern for businesses alongside employment costs.

- Inflation is also on the rise again, triggered by rising fuel prices.

- The labour market has also become more fragile since the start of the conflict.

Before the Iran conflict, the UK economy performed better than expected

UK GDP grew by 0.5% in February 2025 according to official figures; the strongest expansion since March 2024, up from 0.1% in January. The improvement was largely driven by stronger services sector output, which grew by 0.5%, reflecting a good month for firms within administrative and support service activities, and wholesale and retail trade. Production output also grew by 0.5% in the month. Construction rose by 1.0%.

This likely marks the high point for the UK economy this year. Skyrocketing fuel prices and supply chain chaos sparked by the Iran war seems to have stalled economic activity in March, despite an early Easter boost to sectors such as retail.

Prefer to listen?

This audio file was produced by AI and has been adapted from the original article for audio purposes.

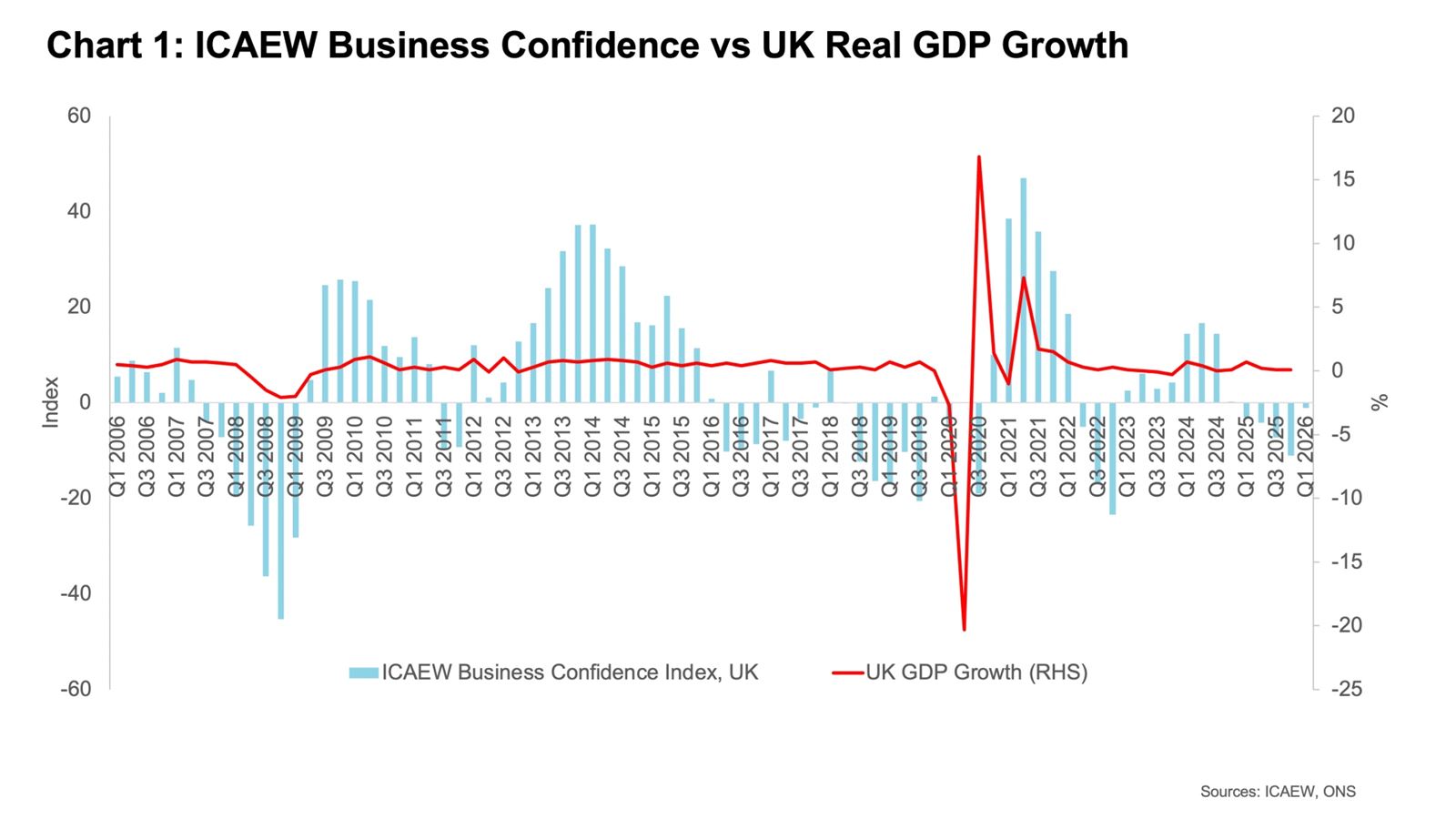

Business confidence recovery thwarted by Iran war

Business confidence in the UK has fallen sharply since the outbreak of the Iran war. Mounting concerns over sales performance, inflation and energy costs have all had an impact. Confidence had been on course to move into positive territory for the first time since Q4 2024. Now, average sentiment tracked by ICAEW’s Business Confidence Monitor (BCM) in Q1 fell from +2.8 on the eve of the conflict to an overall reading of -1.1 by the end of the survey period* (see Chart 1).

Though confidence has still improved from -11.1 in Q4 2025, the impact of the Iran war means sentiment has now been in negative territory for five successive quarters – the longest period in more than six years. Negative confidence readings typically coincide with difficult periods for business, such as the inflation shock that followed Russia’s invasion of Ukraine.

Rising energy and labour costs key business concerns

ICAEW’s BCM also found that one in three (35%) firms are concerned about energy costs, partly reflecting the impact of the Middle East conflict. By sector, worries over energy costs were highest among the largest energy consumers: transportation and storage (44%); energy, water and mining (43%); and retail and wholesale (40%).

The survey found that more than half of businesses (56%) were troubled by labour costs in Q1, the biggest growing challenge to business performance. Labour-intensive sectors such as retail and wholesale (69%) and construction (67%) have been particularly hard-hit. This likely reflects both the impact of last year’s national insurance increase, worries surrounding the impact of the Employment Rights Act and April’s notable minimum wage increase.

Businesses exposure to Middle East conflict revealed

In a separate survey of nearly 500 ICAEW members (businesses and individuals), 56% said they were exposed to the current conflict, while over a quarter (29%) think it’s too early to judge.

In response, 56% said they are monitoring the situation, a quarter (25%) are changing their travel policies or staff security guidance, and 13% said they planned to temporarily alter or halt operations in the most directly impacted regions. For UK businesses specifically, those polled said higher energy costs (66%), supply chain disruption (54%) and staff related challenges around security and travel (46%) were the most prominent challenges.

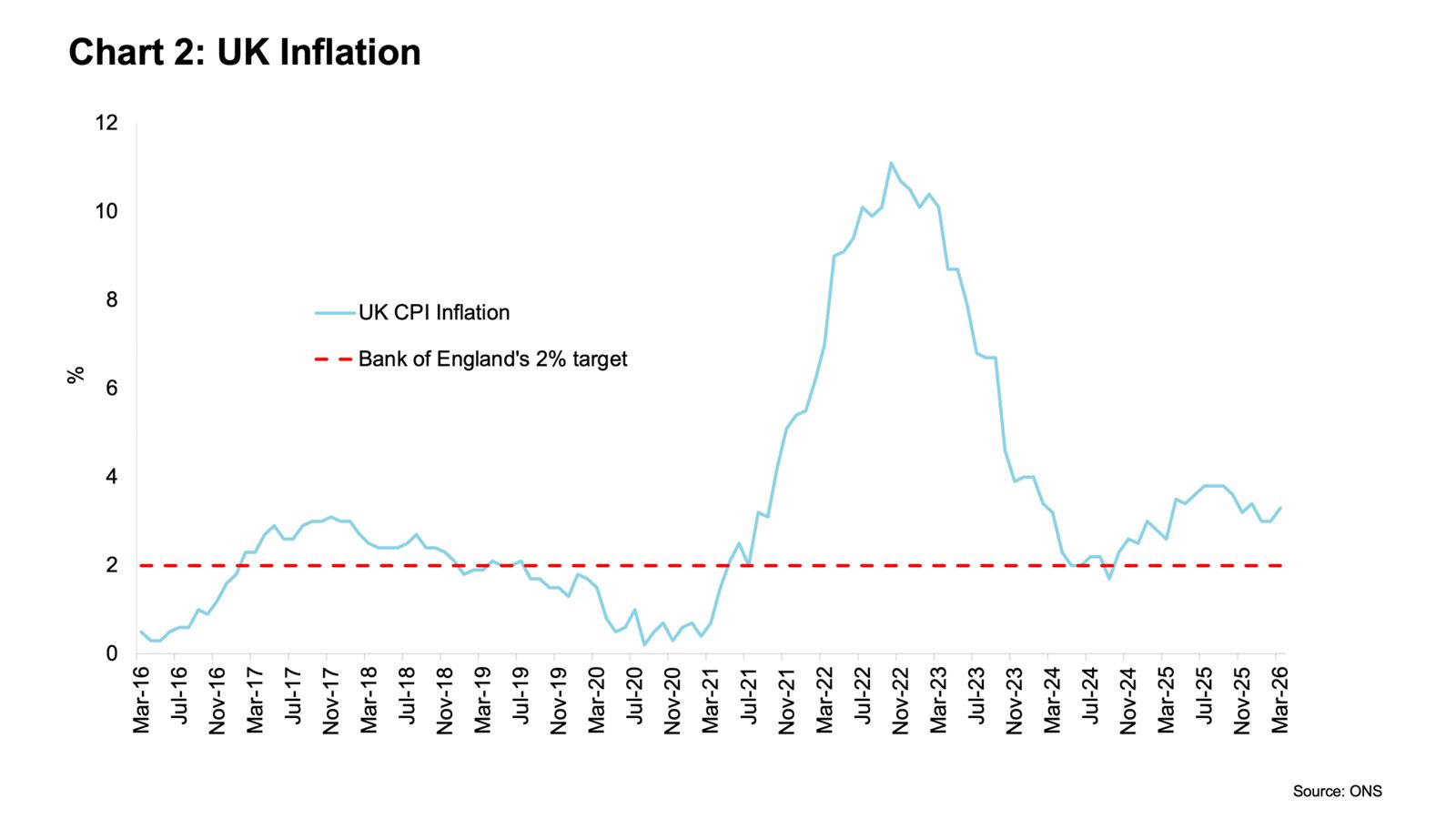

Inflation rises in March

UK CPI inflation increased to 3.3% in March 2026, up from 3.0% in February (see Chart 2). Fuel prices were the primary drivers for this increase, while higher food prices and airfares also added to the upward pressure on the headline rate.

Transport inflation, including motor fuels and airfares, nearly doubled to 4.7% in March, from 2.4% in February; the highest rate since December 2022. Food inflation increased to 3.7%, up from 3.3% in February.

March’s CPI increase is the start of a period of accelerating inflation. Energy costs and food prices are likely to lift the headline rate above 4% by the autumn.

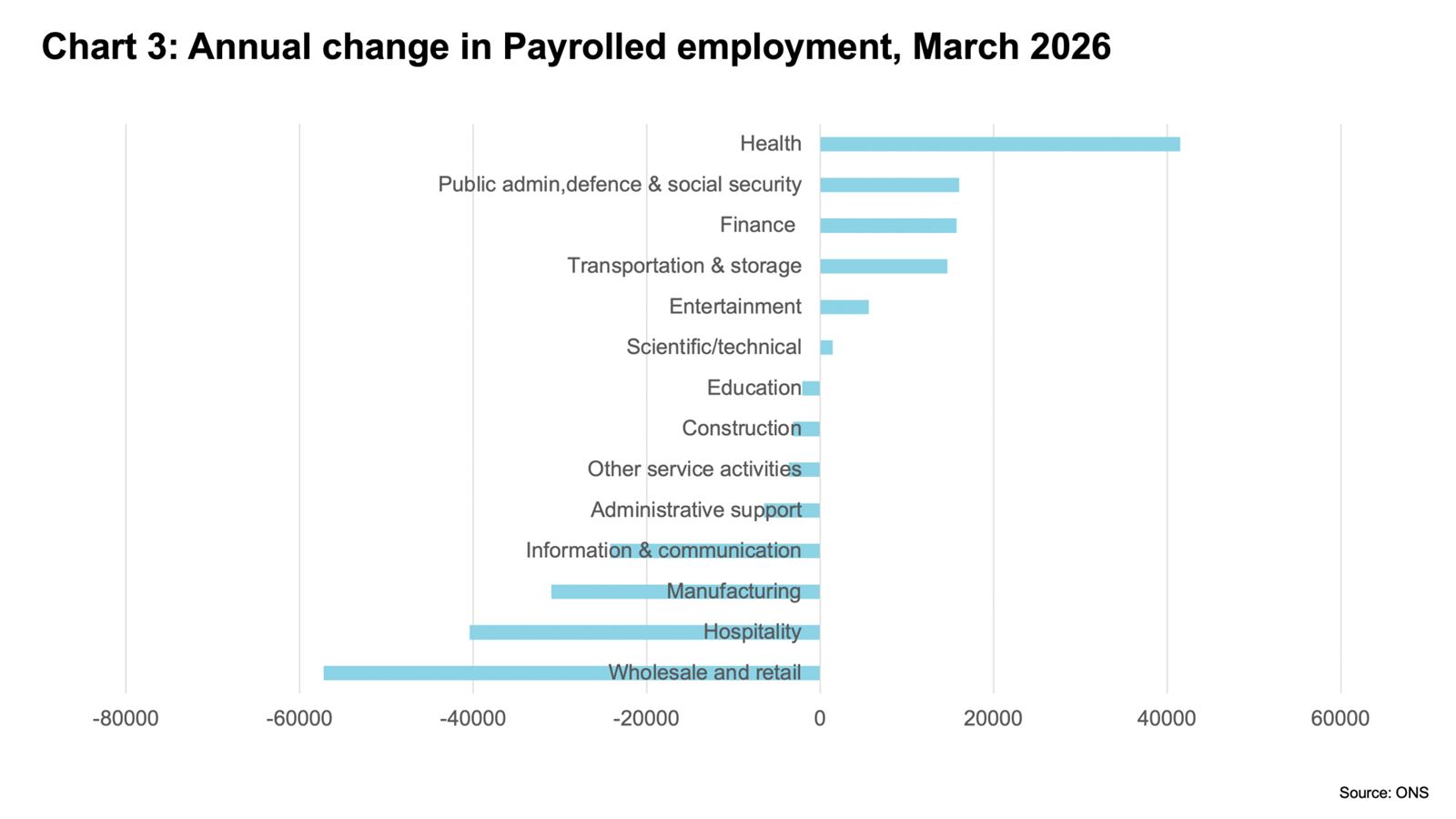

The UK labour market is more fragile following Iran conflict

The number of payrolled employees for March 2026 dropped by 11,000 on the month, and by 65,000 over the past year.

The health and social work sector saw the biggest increase in the number of payrolled employees between March 2025 and March 2026 (see Chart 3) – a rise of 41,000 employees. The largest fall was within the wholesale and retail sector (a fall of 57,000 employees). The number of job vacancies, a good indicator of labour demand, fell by 29,000 in the three months to March 2026 to 711,000, the lowest level of vacancies since 2021.

The Iran conflict will soon pull the UK’s labour market into more troubled waters as costs for businesses rise and consumer demand weakens. The heightened uncertainty is likely to push unemployment uncomfortably close to 6%, especially given elevated employment costs.

Implications for accountants, business owners and the economy

Taken together, these figures suggest that the UK’s economic mood is turning increasingly sour as the impacts of the Iran war set in. Even if a peace deal is reached soon, a severe spell of stagflation looks locked in. Surging energy costs are expected to trigger sizable falls in investment and consumer spending, leaving growth weaker than many expect.

What to look out for

- On 30th April, the Bank of England’s Monetary Policy Committee is expected to keep interest rates at their current rate of 3.75%.

- The March 2026 GDP data to be released on 14th May, is likely to show that the UK GDP growth slowed from 0.5% in February.

- The inflation figures for April out on 20th May may see the headline rate slow slightly from the 3.3% recorded in March.

Further support

Resources

Economy

Expert analysis on the latest national and international economic issues and trends, and interviews with prominent voices across the finance industry alongside data on the state of economy.

Visit the hubResearch

UK Business Confidence

ICAEW's Business Confidence Monitor is one of the largest and most comprehensive quarterly surveys of business conditions and the health of the UK economy.

Read the latest findingsICAEW support

Training and events

Browse upcoming and on-demand ICAEW events and webinars looking at the global economy and trade.

Events and webinars A-Z of CPD Courses