-

What is the purpose of a long-form UK statutory auditor's report?

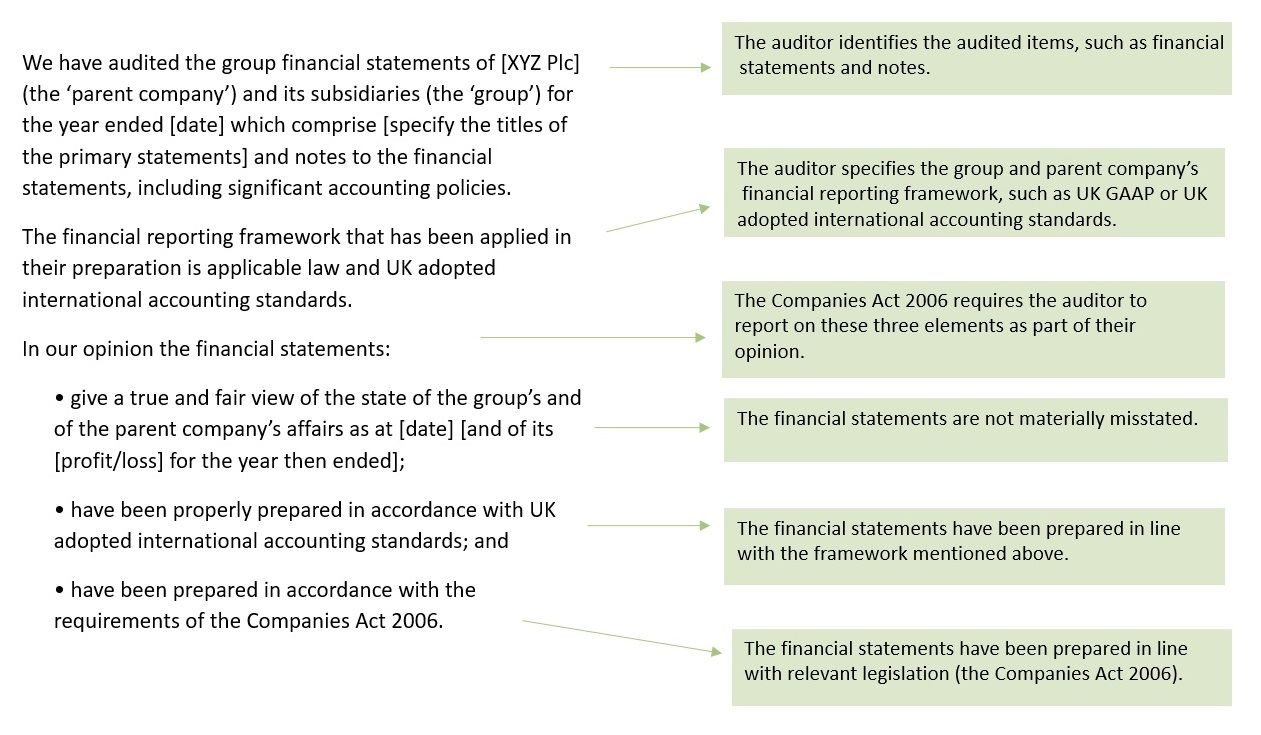

The purpose of a statutory auditor's report is to provide a written opinion on whether an entity’s annual accounts:

- give a true and fair view;

- have been properly prepared in accordance with the relevant financial reporting framework; and

- have been prepared in accordance with requirements of the Companies Act 2006.

-

What does that actually mean?

An auditor's report is seen as a trusted ‘kitemark’ on a company’s financial statements from an independent qualified professional. It enhances the credibility of financial statements by:

- providing assurance to shareholders that an entity’s financial statements are free from material misstatement;

- helping to ensure that an entity's management are held accountable to shareholders;

- allowing auditors to communicate significant issues through paragraphs covering opinion modifications, material uncertainties, and other matter paragraphs.

- providing valuable insights and commentary on significant matters addressed during the audit through KAMs.

Further reading:

-

Who needs an auditor's report?

Section 475 of the Companies Act 2006 dictates that a company’s annual accounts for a financial year must be audited unless the company is exempt from audit.

Private companies that are small, dormant or have a parent guarantee are exempt. A large number of companies fall into this category. A small company is defined as a company that meets any two of the following criteria:

- a turnover of £15m or less;

- £7.5m or less on its balance sheet;

- and 50 employees or less.

Section 476 of the Companies Act provides an option for members of the company to require an audit.

Further reading:

-

Who uses an auditor's report?

Auditors carry out an audit to provide a report for, and only for, the members of the company as a body (Chapter 3, Part 16 of the Companies Act 2006).

However, UK auditor's reports are publicly available within the audited financial statements that are filed on the Companies House database. Many entities also publish the audited financial statements on their website.

Many stakeholders have an interest in how companies are run and may look to auditor's reports for comfort about the reliability of a company’s reporting. This is not just to assess the financial position and performance, but to evaluate corporate governance, company values, economic impact on the local community and strategic plans for the future.

Auditor's reports are also of interest to, among others: potential investors, creditors, employees, consumers, the public, regulators, government and trade unions.

-

What is always included in an auditor's report?

- Opinion

Including the truth and fairness of the financial statements - Basis for opinion

Scope of the audit, what the auditors did - Conclusions relating to going concern

Unless a material uncertainty exists...

(If there is a material uncertainty related to going concern, and appropriate disclosure has been made in the financial statements, a separate section entitled “material uncertainty related to going concern” should be included in the auditor's report. If the relevant additional disclosure requirements have been included in this section, the “conclusions related to going concern” section can be excluded.) - Other information

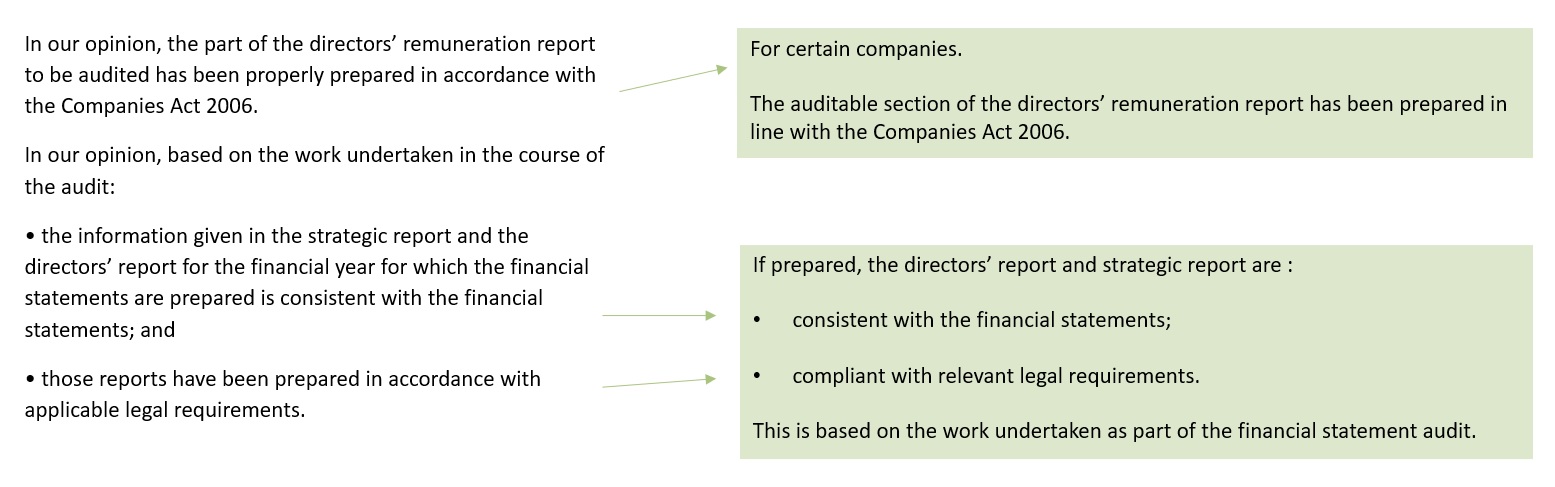

The auditor’s responsibility for information other than the financial statements in the annual report - Opinions on other matters prescribed by the Companies Act 2006

For example, including work performed on the directors’ remuneration report and strategic report - Matters on which the auditor is required to report ‘by exception’

For example, relating to keeping proper accounting records - Responsibilities of directors

For the preparation of financial statements - Auditor’s responsibilities for the audit of the financial statements

Including conducting an audit in accordance with auditing standards - Use of the report

Restricting it to those to whom it is addressed - Signature and date

- Opinion

-

Additional information in certain auditor's reports

Some of the matters in an auditor’s report, including the issues below, are specific to certain types of entities. For example, the approach to the audit below is only required for public interest entities (PIEs) and other entities that are required (and those that choose voluntarily) to report on how they have applied the UK Corporate Governance Code.

A public interest entity is as defined by the FRC’s Glossary of Terms.

- Approach to the audit

- scope of the audit

- key audit matters (KAMs)

- application of materiality

- Opinion on the company’s corporate governance statement

- Other matters which auditors are required to address (such as appointment of auditor and information on non-audit services).

-

What is sometimes included in an auditor's report that warrants special attention?

- Material uncertainty relating to going concern;

- A modified opinion, including ‘qualified opinions’ and basis for modified opinion section;

- An emphasis of matter paragraph and other matter paragraph.

Emphasis of matter paragraphs do not change the audit opinion. They draw the attention of users to a matter presented or disclosed in the financial statements that the auditor thinks is fundamental to their understanding of the financial statements. In practice, they are not common but they are often significant and, for example, may refer to the financing structure of an entity.

Other matter paragraphs refer to a matter that is not required to be presented or disclosed in the financial statements, but that the auditor thinks is relevant to users’ understanding of the audit, the auditor’s responsibilities or the auditor’s report.

Opinion

This section is the most critical element of an auditor's report. It contains the auditor’s opinion on the group and parent company’s financial statements. The auditor will provide either an unmodified (clean) opinion or a modified opinion. The title of this section will usually be changed to highlight this to users.

A modified opinion will be issued where:

- the auditor is unable to obtain sufficient appropriate audit evidence to determine whether the financial statements (or a part of them) give a true and fair view; or

- having collected enough evidence, the auditor has assessed that the financial statements (or a part of them) do not give a true and fair view.

There are three types of modified opinions:

- qualified;

- disclaimer of opinion; and

- an adverse opinion.

The type of modification will also depend on how pervasive the issue is. An explanation of the reasons for the modified opinion will be given in the “Basis for qualified opinion” section of the auditor's report.

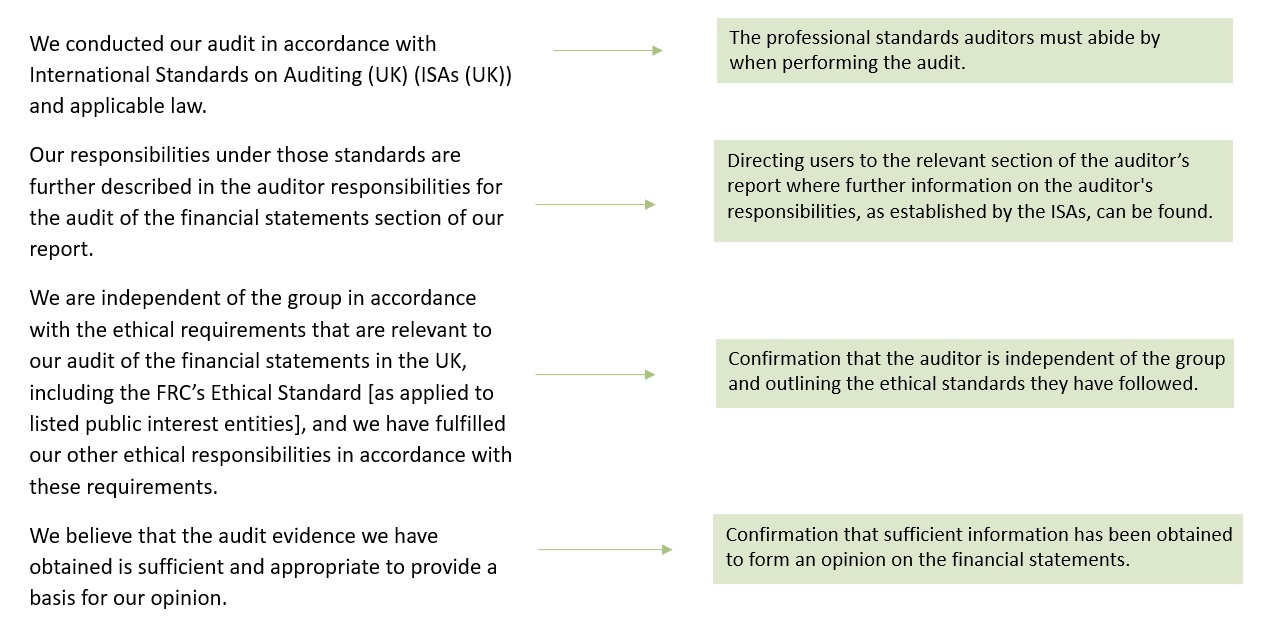

Basis for opinion

The basis for opinion provides background information relevant to the auditor’s opinion.

It is usually standard, but if the auditor’s opinion is modified, details and explanations will be provided here.

Our approach to the audit

This section is only required for certain entities. It is tailored for each audit.

It is a largely free-form section and gives an opportunity for the auditor to describe what they have done. This section includes:

- A summary of the audit's scope, including, where applicable, the audited components within a group.

- Key audit matters (KAMs).

- The application of materiality.

While not specifically required by auditing standards, as part of this section the auditor's report may include:

- the impact of climate-related risk on the audit (not mandatory); and

- the impact of the control environment on the audit approach (not mandatory).

Scope of the audit

This text is not defined and is free-form, but it provides an overview of the scope of the parent company and group audits. It can include:

- how the components were identified and scoped and how this was influenced by the group structure and materiality;

- how the audit procedures were planned, including the nature and amount of work performed on components;

- interaction with and oversight of component auditors; and

- any changes in approach compared to the previous year.

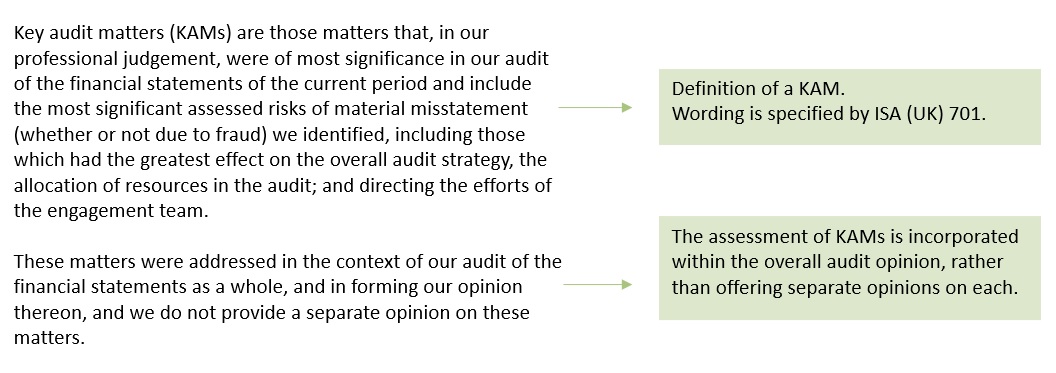

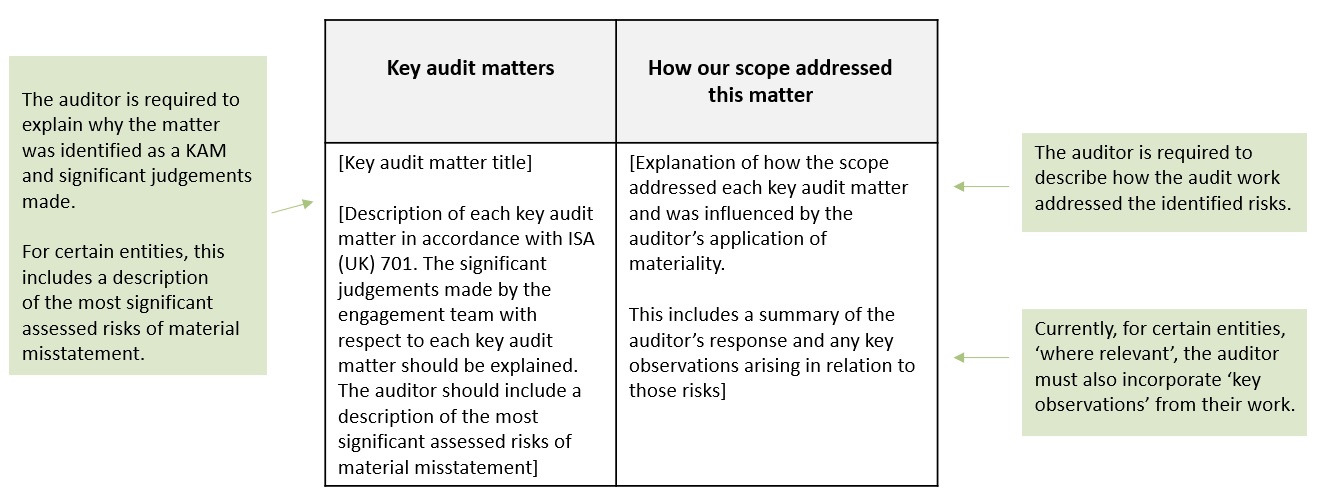

Key audit matters (KAMs)

KAMs are specific to each audit and may help identify areas that require further investigation. They typically relate to:

- areas of significant or higher risk;

- areas requiring substantial auditor and management judgement;

- areas associated with a significant event or transaction,

- areas which required the most auditor effort or had the most effect on the audit.

KAMs are used to highlight significant issues from the audit. They aim to prompt discussions between auditors, audit committees and investors.

The presentation of KAMs varies across firms and their audited entities. Typically, they are displayed in a tabular format with two headings that offer detailed information about the KAM and the related audit work performed.

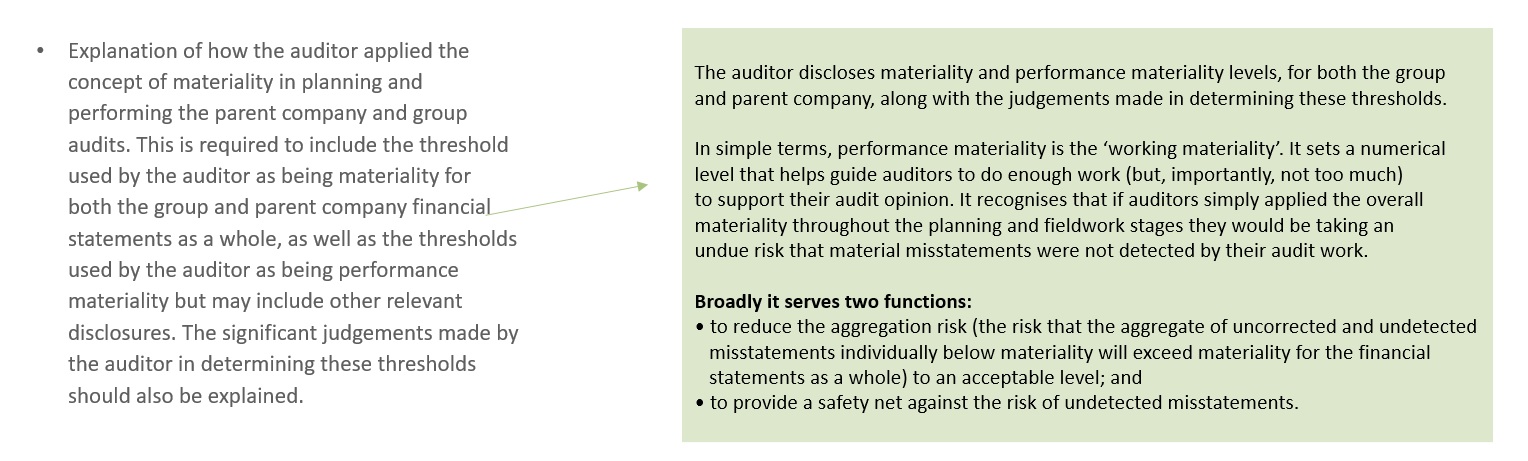

Our application of materiality

The application of materiality is specific to each audit.

Although presentation styles may vary among audit firms, it is common to utilise graphics or tables to visually represent this information.

Non-mandatory additions

The impact of climate-related risk on the audit

Climate-related disclosures are not mandatory but are an increasingly common voluntary disclosure by auditors. The extent of the impact of climate-related risk will vary between companies.

The auditor needs to consider whether the financial statements reflect all material risks, including climate-related risks, which may involve the use of experts.

Auditing standards require that auditors determine whether there are any material inconsistencies between all disclosures in the annual report, and:

- the audited financial statements;

- or the auditor’s understanding (as gained during the course of the financial statement audit),

which may indicate a material misstatement in the financial statements.

This includes climate-related disclosures.

The impact of the control environment on the audit approach

This is not mandatory but there are examples of auditors including more information on controls in their auditor's reports, including the extent to which the auditor was able to rely on controls as part of the testing approach and the extent to which they undertook substantive testing.

For financial years beginning on or after 1 January 2026, provision 29 of the UK Corporate Governance Code requires boards to declare information relating to the effectiveness of their internal controls.

As part of their work on ‘Other Information’ under ISA (UK) 720, auditors will consider the statements the board has made in relation to this provision and whether this is consistent with the knowledge obtained during the audit.

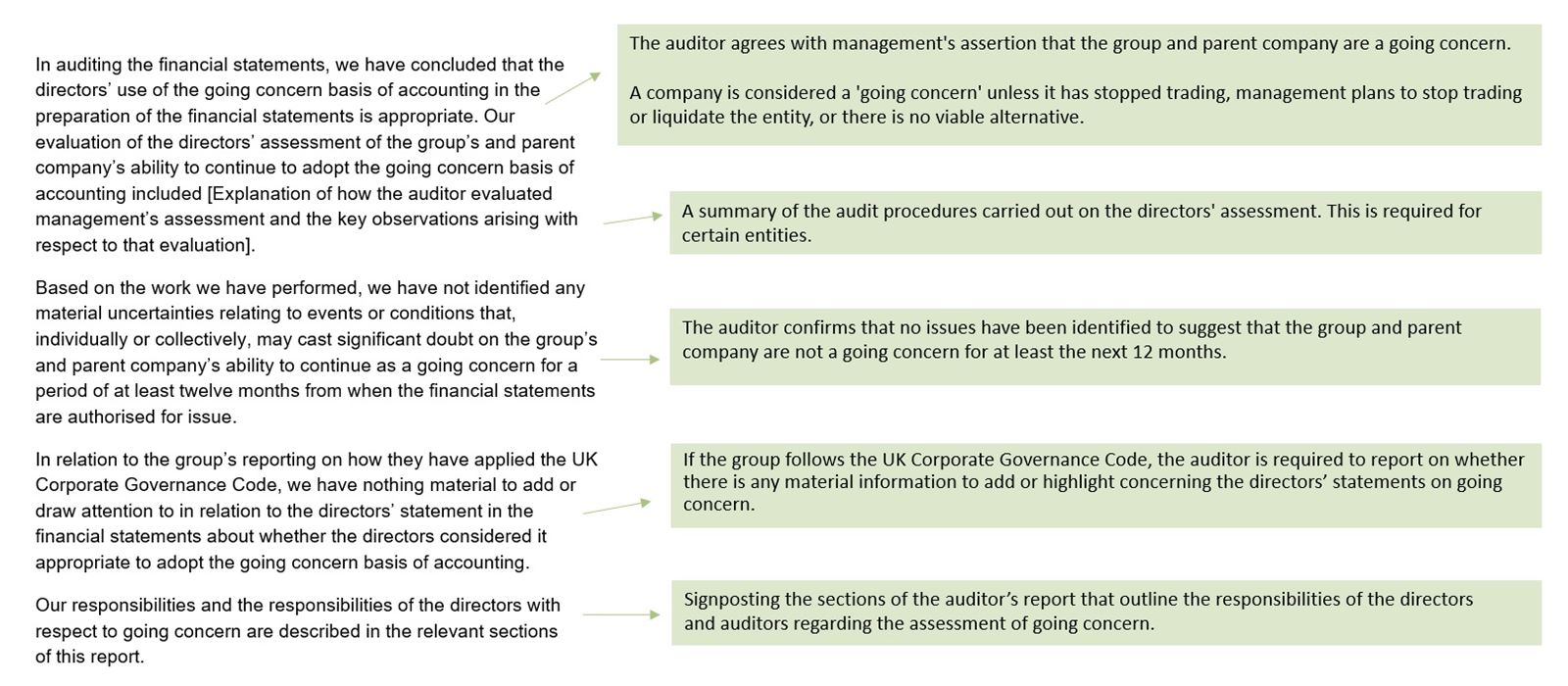

Conclusions relating to going concern

The auditor’s evaluation of the group’s and parent company’s ability to continue as a going concern. The wording is standard, except for the audit procedures, which are unique to each audit. The first consideration for users should be whether there is a material uncertainty relating to going concern.

A material uncertainty about going concern exists when the potential impact and likelihood of events require disclosure to fairly present the financial statements or prevent them from being misleading. If a material uncertainty relating to going concern exists, this section is not included. If the uncertainty has been disclosed appropriately, a ‘material uncertainty relating to going concern’ section is included instead. If the uncertainty has not been disclosed, a qualified or adverse opinion is issued.

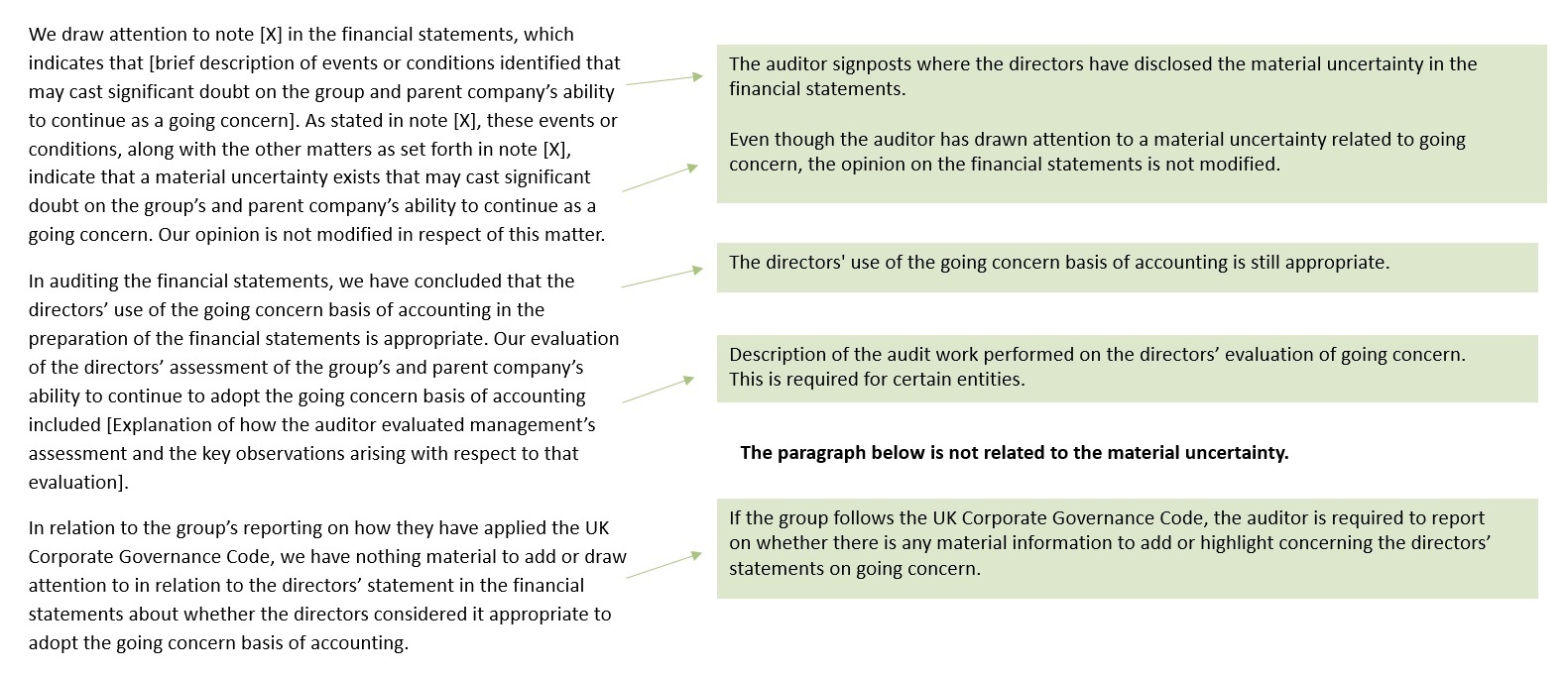

Material uncertainty relating to going concern

This section is required where the directors have determined that a material uncertainty about going concern exists

and the directors have provided clear and transparent disclosures in the financial statements about the uncertainty.

A material uncertainty about going concern exists when the potential impact and likelihood of events require

disclosure to fairly present the financial statements or prevent them from being misleading.

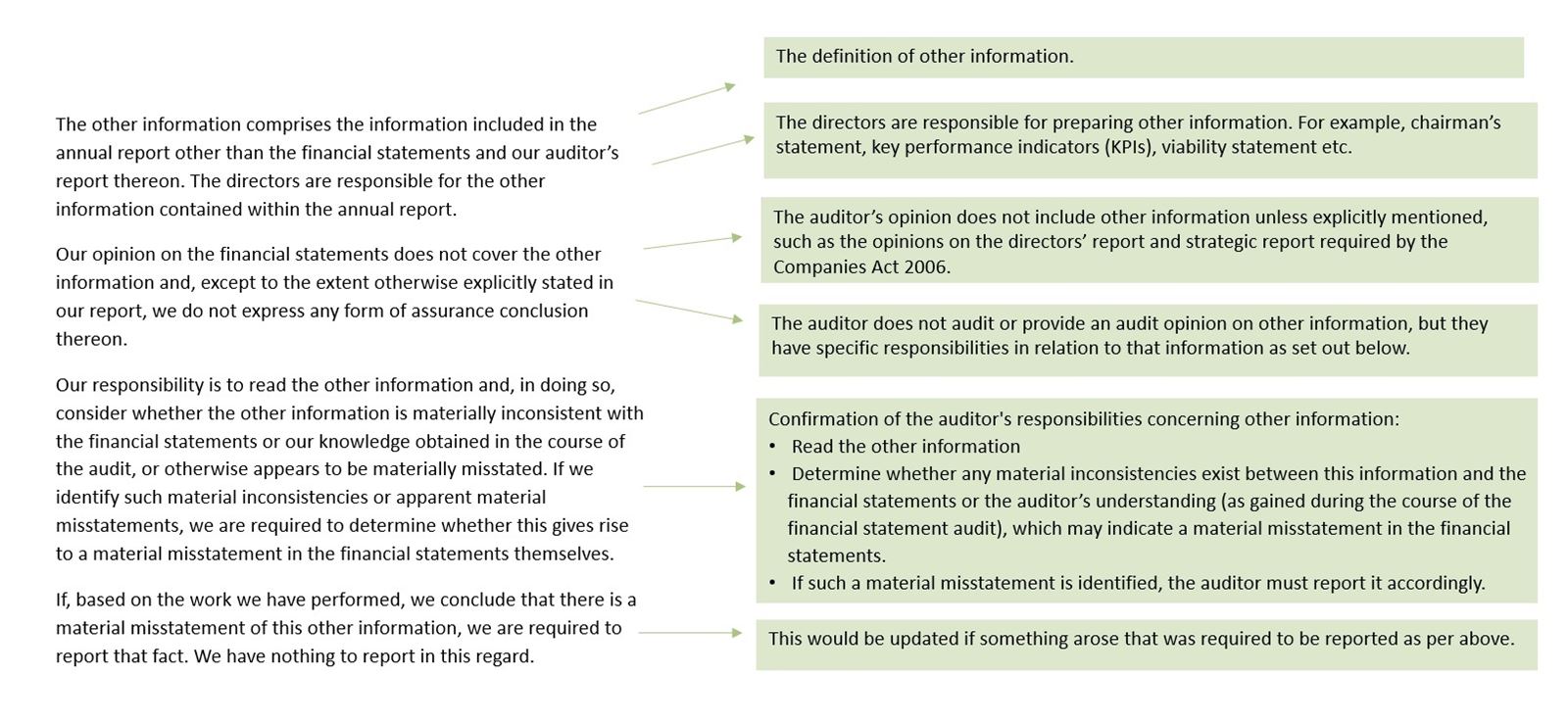

Other information

This is standard wording (apart from the last sentence) that is required to be included by auditing standards, outlining the auditor's responsibilities regarding 'other information’ in the financial statements, such as the directors' report or strategic report.

Opinions on other matters prescribed by the Companies Act 2006

The Companies Act 2006 mandates that auditors must report on specific additional matters within the auditor's report.

This is standard wording, unless there is something to report per below.

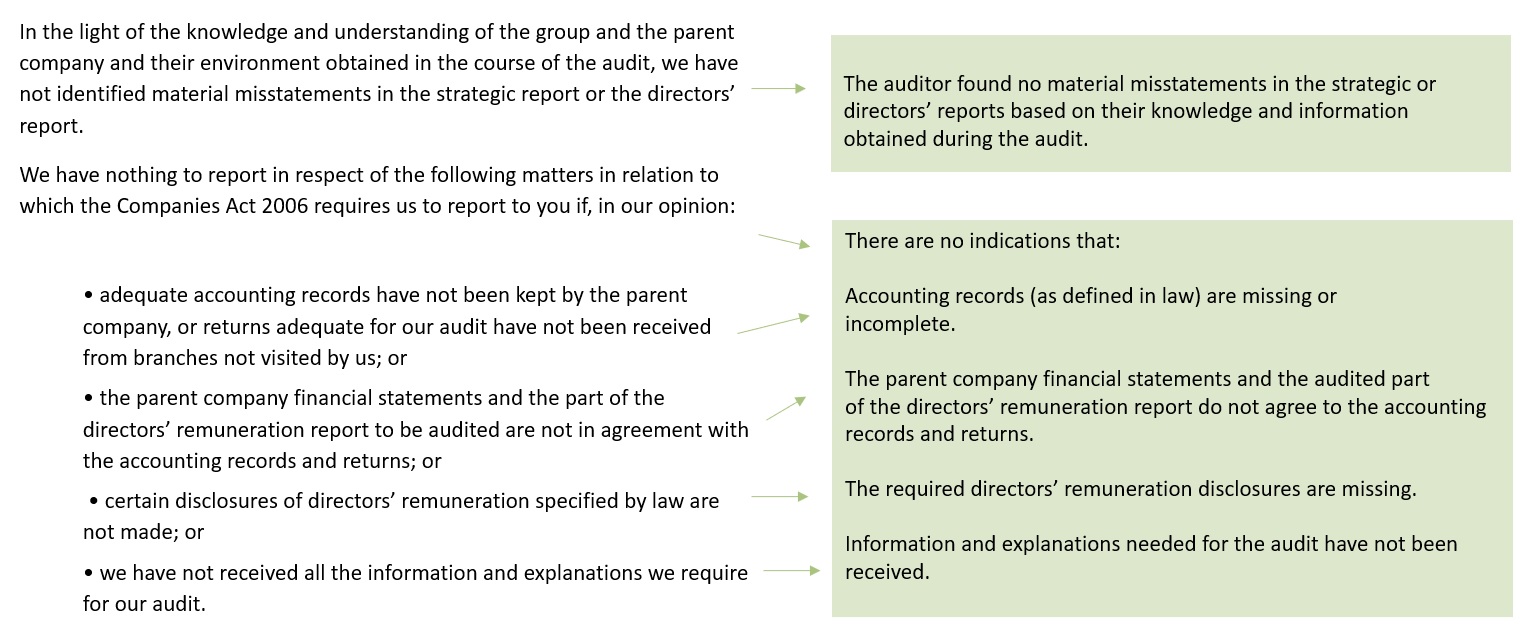

Matters on which we are required to report by exception

The auditor must report on specific matters by exception, where required by law or regulation.

For companies, this includes requirements outlined in the Companies Act 2006. This is standard wording.

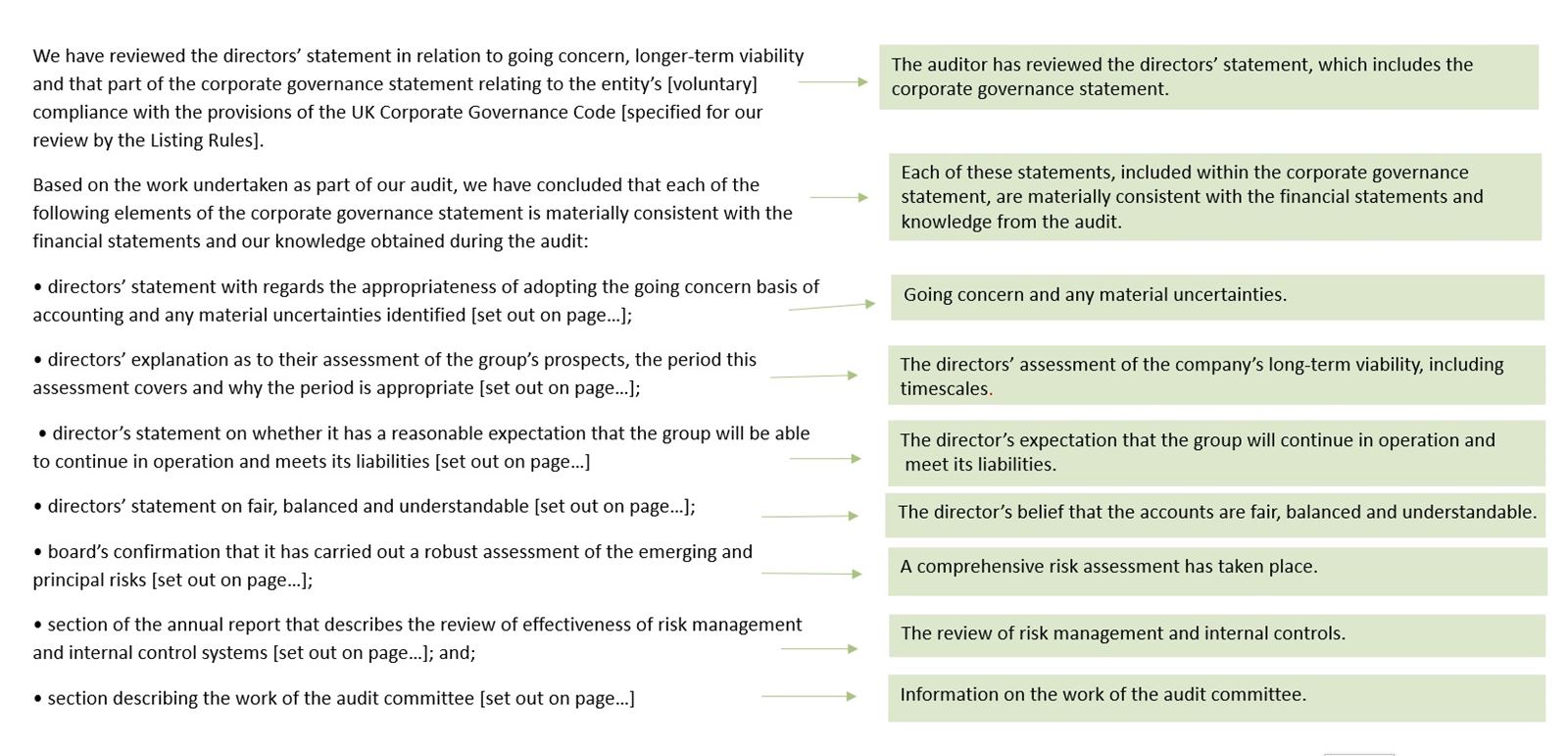

Corporate governance statement

This is required for certain entities. This is standard wording.

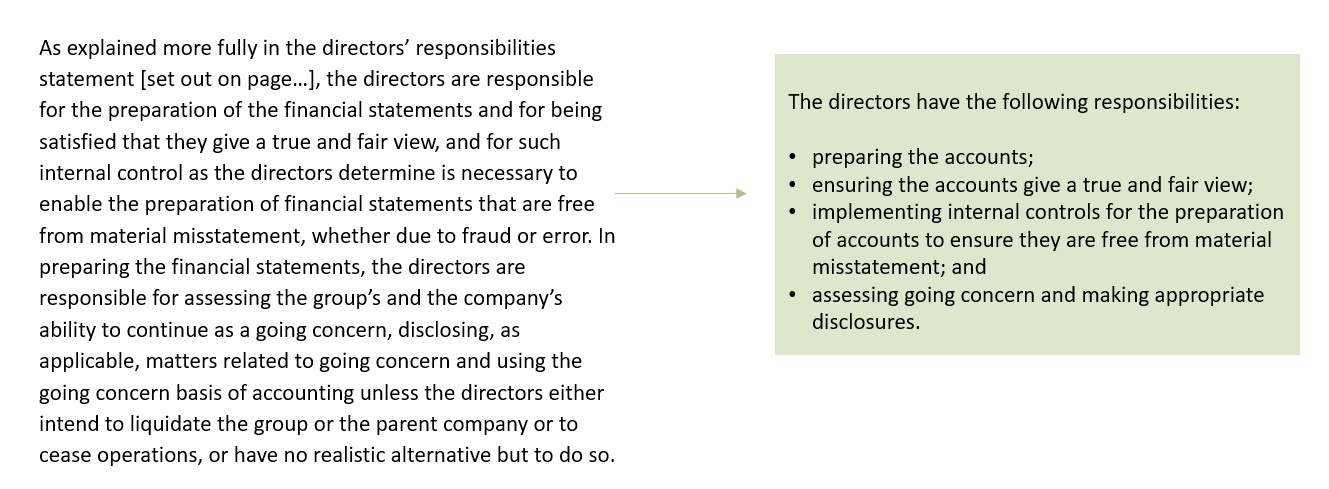

Responsibilities of directors

This section indicates where in the annual report you can find detailed information on directors' responsibilities.

It is typically standard wording.

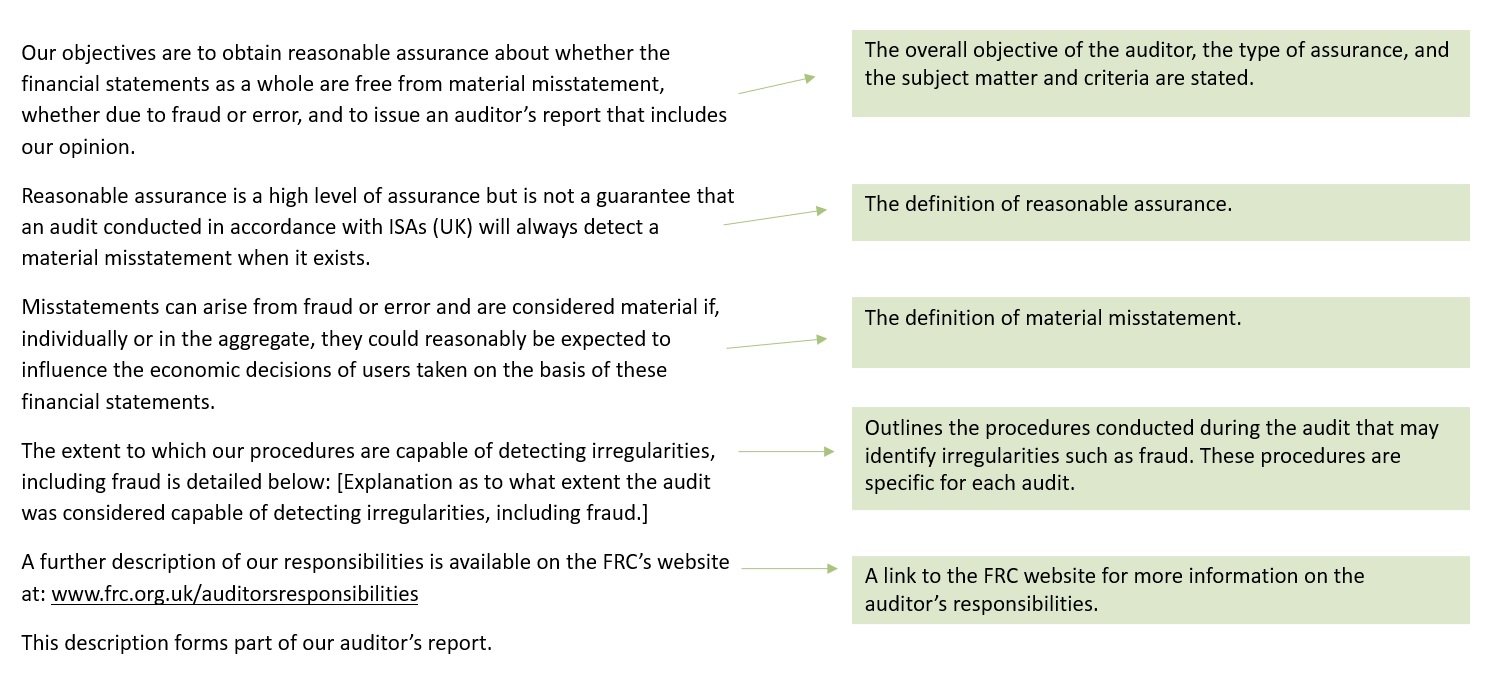

Auditor’s responsibilities for the audit of the financial statements

This section outlines the auditor's responsibilities for conducting the audit. This wording is standard.

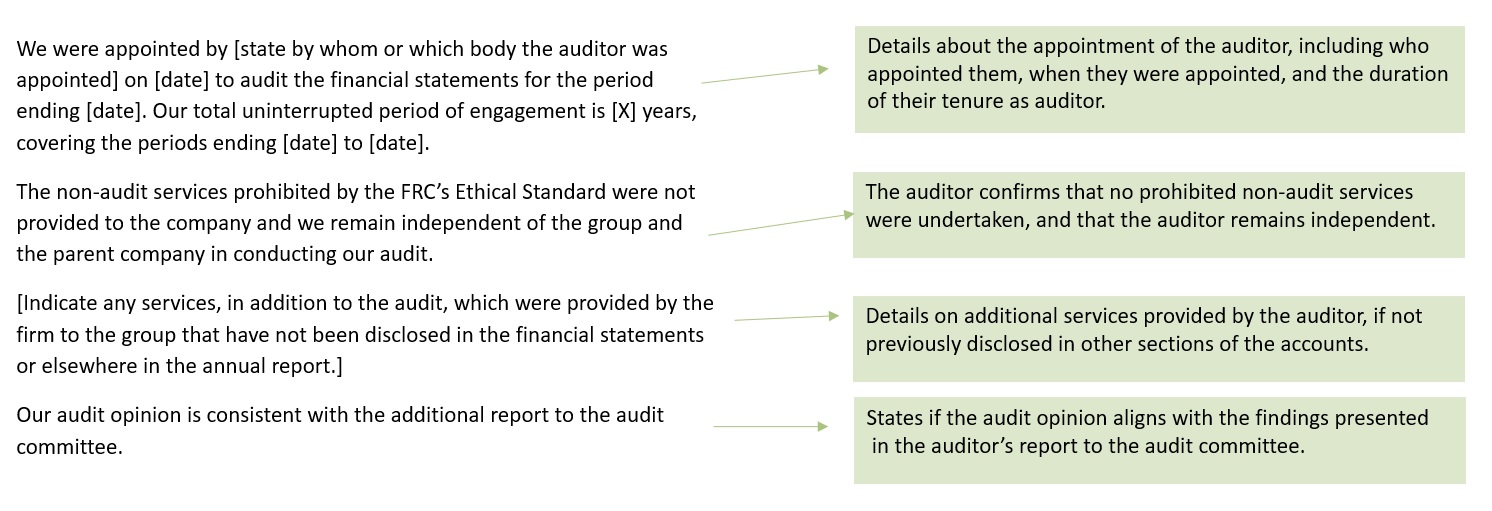

Other matters which we are required to address

This is required for certain entities.

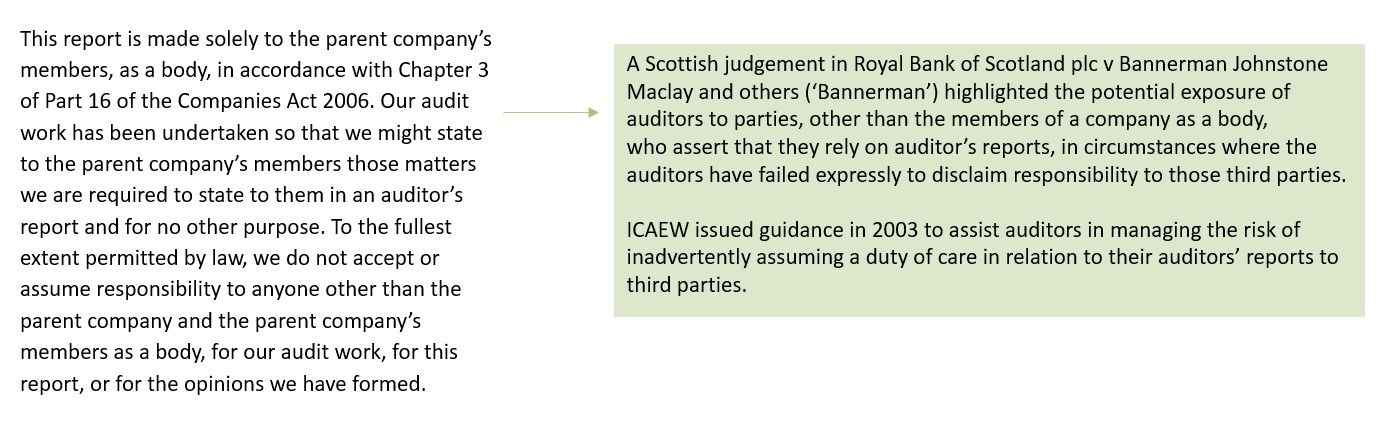

Use of our report

This paragraph, also known as the ‘Bannerman’ paragraph, was added as a result of various legal cases and legal advice obtained by

ICAEW over the auditor’s duty of care to third parties. It clarifies to whom the auditor has a duty of care and it disclaims liability to others.

Signature and date

UK auditors' reports must state the name of the auditor and be signed.

Where the auditor is a firm rather than an individual, the auditor's report must be signed by the senior statutory auditor on behalf of the firm.

The auditor's report must not be dated earlier than when the auditor has obtained sufficient appropriate audit evidence to form their opinion.

You may also be interested in

Audit in depth

In-depth guidance on completing all stages of an audit as well as how to make the decision as to whether or not an audit is required.

Find out more

Audit reports

Understand how to prepare an audit report for an array of different circumstances, sectors and legislation.

View