In anticipation of the UK Government reconsidering its corporate reporting framework, Claire Bodanis, Founder and Director of Falcon Windsor, has developed her own thoughts on a new model for the AI era – one that rethinks the annual report from first principles and restores the essential distinction between disclosures and commentary.

Anyone who cares about corporate reporting – especially writers – should be very grateful to accountants. Not only because corporate reporting as we know it today started with the 1844 Joint Stock Companies Act, which required a ‘full and fair’ balance sheet to be distributed at annual general meetings, but because writing itself was invented by accountants.

That, at least, is how it would have appeared to the Mesopotamians of the late 4th Millennium BC when they invented a new system of scratching signs into wet clay, the earliest ‘writing’ we know of. They wanted to do a version of what we still want to do now: corporate reporting. When the size of a society has outstripped the size of the human brain, you need writing to record transactions, to record who owes what to whom. For civilisation to exist at all, you need accountants (see Claire Bodanis' book, Trust me, I’m listed - why the annual report matters and how to do it well).

Such musings, together with 25 years of advising companies and writing annual reports – and the insights this has given me into what preparers and users want from reporting – inspired me to develop Falcon Windsor’s new model for corporate reporting for the age of AI. After I was interviewed by the Department for Business and Trade (DBT) in summer 2025 when they revisited the Non-Financial Reporting Review, we presented our model to the DBT in December 2025 to inspire their thinking for what has now become the Modernisation of Corporate Reporting (MCR) programme.

As ICAEW’s Head of Corporate Reporting Strategy, Sally Baker, stated in her recent explainer on the MCR, the government decided that “only reviewing non-financial reporting would fall short of what is needed” and that “a more holistic approach was warranted”. In other words, the whole annual report is up for grabs. Plus, the DBT is “considering how reporting can be modernised in the digital age”. This is a great time to rethink reporting from first principles.

The beautiful structure of financial reporting

People have long complained that corporate reporting is too long, too boring, too complicated and not fit for purpose. And yet if we think of just its accounting aspects, our modern-day version is actually good. What is not to like about a clearly structured, generally consistent set of financial statements plus notes (the accounts or “back-half”), along with management’s commentary on what those accounts mean?

Therefore, I wondered: why do we only see this beautiful distinction between the accounts (or disclosures) and commentary in the pages devoted to financial information? Why not use it for all types of corporate information?

After all, reporting as a whole serves its purpose of building a relationship of trust between a company and its stakeholders through both:

- accurate data and disclosures, in accordance with reporting requirements; and

- truthful commentary – namely, the opinion of management and the board as to the meaning of those disclosures for the company and its prospects.

The idea of this distinction between the two types of information was reinforced by what FTSE companies and investors told us in our research into the responsible use of generative AI in corporate reporting (Your Precocious Intern, published in May 2025 with tech company, Insig AI) – DBT referred to it in the digital aspects of the MCR.

Investors saw many benefits in using generative AI to support producing disclosure-type information, as long as there was human oversight to ensure factual accuracy. But they were concerned about its use in creating commentary – because opinions and decisions must remain the preserve of those responsible for them, instead of being generated by AI.

I concluded that the only way we can use generative AI for the benefit of reporting is to rethink the structure of the annual report from first principles. This means applying that ‘beautiful distinction’ between financial disclosures and commentary to all disclosures and commentary (instead of having them mixed up together in the strategic and governance reports).

What would this look like in practice?

The model in summary

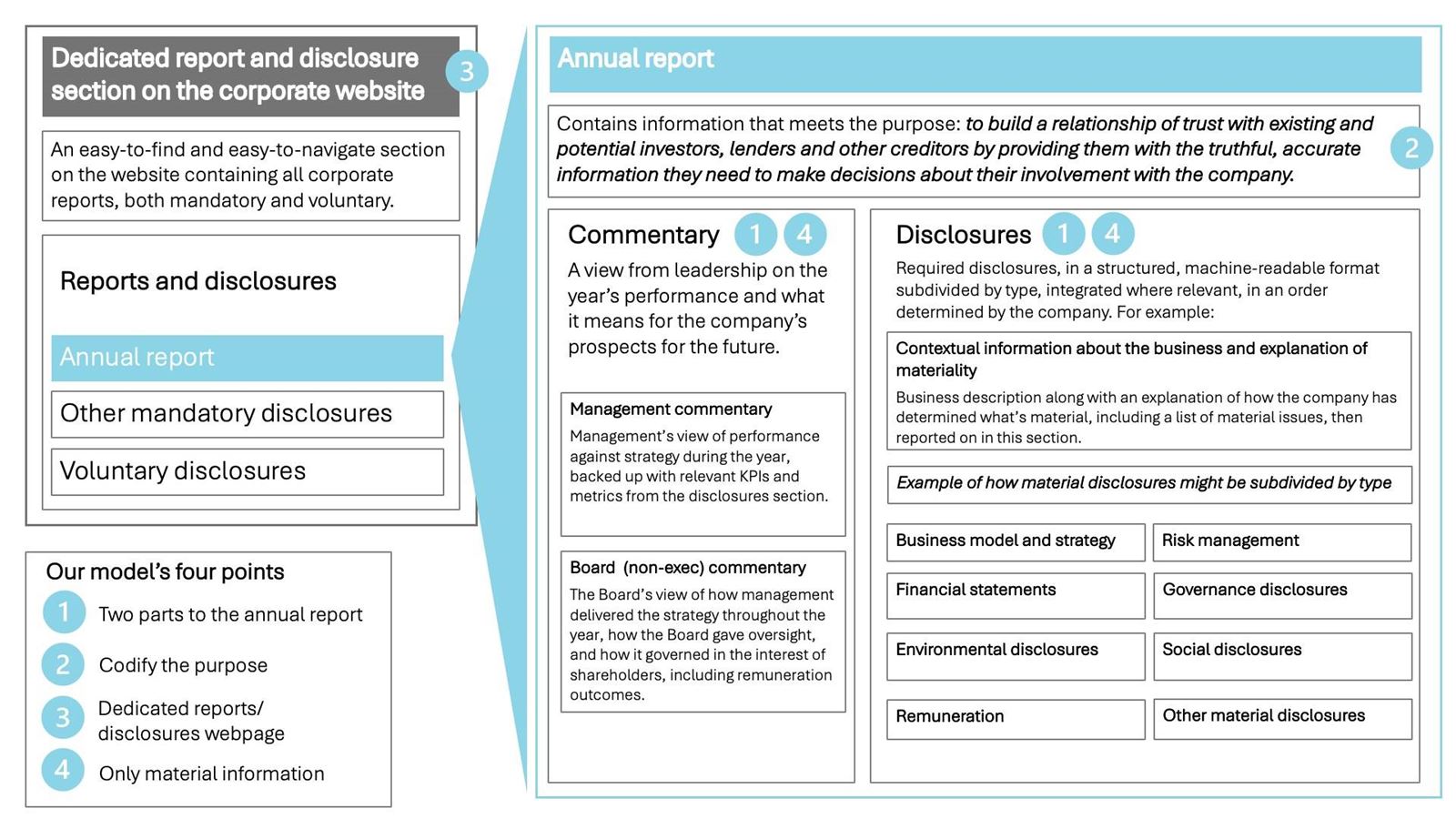

Our model has four key points, summarised in the diagram below.

- Two-part annual report structure

- Codified purpose

- Dedicated reports/disclosure webpage

- Only material information included

The full explanation includes various practical considerations, like double versus single materiality, audit and assurance, stakeholder needs and so on, and can be found on Falcon Windsor’s website. It benefited from the contributions of 50+ FTSE companies, technical and regulatory experts, auditors and investors.

The model's four points

1. A two-part annual report, with guidelines on how to use AI – potentially saving 10% reporting costs per year

As the diagram illustrates, we propose two parts for the annual report.

- A set of disclosures covering everything material (see below for more on materiality). The idea is to provide these disclosures in a single, structured statement, sub-divided by type of disclosure. Once created and properly structured, this section could be rolled over in its entirety and updated each year, just as financial statements are today.

- A commentary section sub-divided between management and the board to reflect the different perspectives of their roles. Each sub-section should be a single, coherent and comprehensive narrative, giving a reasonable explanation of the information in the disclosure statements. This directly addresses the longstanding problem of a lack of connectivity, since this single narrative would require reporters to explain the relationship between all disclosures – not just write commentaries on, say, environmental or financial issues. Also, it is essential that companies are not told what to include. They must think for themselves and give their honest opinion on their own information.

Generative AI could be used to help produce the disclosures – as long as the disclosures are carefully checked and signed off by humans – but should not be used to write the commentary. This may seem an extreme stance, but knowing how people are already using AI, it is highly unlikely that these commentaries would truly be the opinion of those responsible for them if companies are allowed to use AI to write them.

Indeed, to use the AI sales pitch – AI could help with the heavy lifting, ie, writing disclosures, freeing up people’s time to be spent elsewhere ie, on analysis and commentary.

In terms of resources, some corporate feedback suggested that, aside from the obvious benefits of a clearer, shorter, and overall better report, our model could save up to 10% of time and cost spent on reporting after the first year.

2. A codified purpose for corporate reporting overall and, within that, for the annual report for different types of companies

What should companies include? To determine what’s material, you have to know who you’re reporting to and why, otherwise everything’s material and the annual report is no use to anyone. This is where the purpose of reporting comes in, and why it should be codified.

In our model, within the overall purpose of reporting, different types of companies would have specific purposes for their annual reports. For example, in the case of listed companies with external investors: their annual reports focuses on the companies’ owners, so the purpose (aligned with that of IFRS® Accounting Standards) would be:

To build a relationship of trust with existing and potential investors, lenders and other creditors by providing them with the truthful, accurate information they need to make decisions about their involvement with the company.

Note that this purpose covers all information that could influence decision-making — not just financial data but sustainability and other relevant information too. After all, the aim of the new UK Sustainability Reporting Standards is to determine what sustainability information is material to investors.

3. A dedicated top-level section of the corporate website called ‘Reports and disclosures’

As shown on the left side of the diagram, the annual report would live in a dedicated section of the corporate website, along with other required disclosures that are not material and anything else a business chooses to disclose. This section should be called the same by every company, for example, Reports and disclosures, so that it can be easily found, whether that is by a human or AI.

4. Only material information should be included in the annual report

For any new model to work, the annual report must only include information that’s material, as determined by the report’s purpose. Otherwise, companies will have to include information that is not useful to the principal audience, and we’ll be back to where we started.

What’s next?

Accountants, specifically ICAEW, will have considerable influence on the MCR debate. While I believe the DBT has taken on board Falcon Windsor’s principle of codifying the purpose of reporting, I am not sure they have accepted the proposed two-part structure, or the use of the corporate website. If you find merit in our model, please do mention it in your engagement with ICAEW.

Claire Bodanis, Founder and Director, Falcon Windsor. Bodanis is also the author of Trust me I’m listed – why the annual report matters and how to do it well published in 2021.