Find out how UKEB’s proposed approach generates stronger evidence on the economic effects of adopting new IFRS Accounting Standards, helping to inform and strengthen future endorsement decisions.

Who is the UKEB?

The UK Endorsement Board (UKEB) is the UK’s national standard-setter for IFRS® Accounting Standards. It has statutory responsibility for influencing the development of IFRS Accounting Standards and assessing them for adoption for use in the UK.

In September 2025, the UKEB published a report setting out an approach to assess potential cost of capital reductions, associated with the adoption of a new or substantially amended IFRS Accounting Standard by UK preparers – an approach intended to show how implementation costs can be recovered in the long run if cost of capital is expected to decrease market-wise.

Why has the UKEB developed an approach to estimate capital market effects?

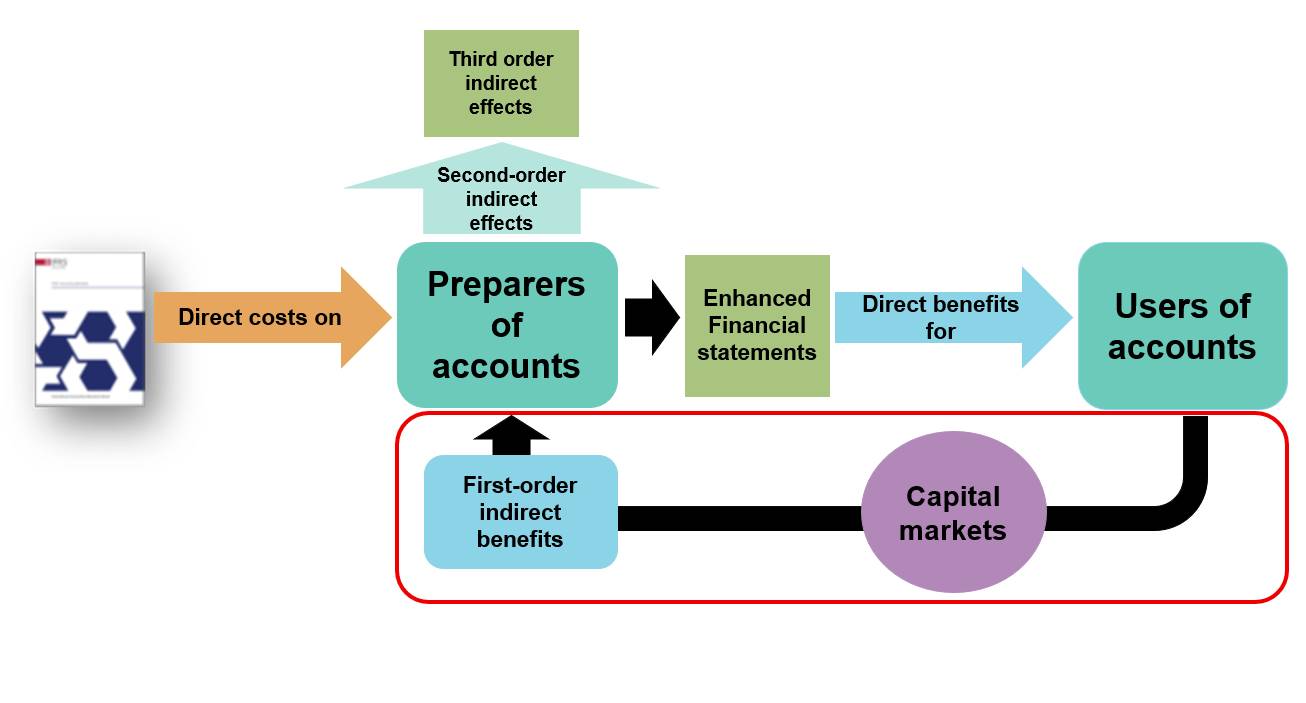

The adoption of new accounting standards can impose a direct cost on preparers, mostly for the direct benefit of users of financial statements.

Economic effects associated with the IFRS Accounting Standards

Source: UKEB

Preparers’ finance departments would usually incur direct monetary and non-monetary costs (ie, reallocation of staff time) to implement a new standard. Such costs could include familiarisation with the new requirements, changes to accounting systems and amendments to internal processes.

However, improved accounting provides a direct benefit to users of financial statements. In the main this arises as enhanced financial reporting enables users to spend their time more efficiently to compare investment opportunities, construct portfolios and allocate capital.

Impact assessments of the adoption of accounting standards have, typically, only focused on the direct costs and benefits outlined above. However, such assessments ignore indirect economic effects brought about by changes to accounting standards.

One such indirect effect can arise when better financial reporting allows investors to improve their capital allocation. This is expected to lead to a market-wide effect – a reduction in the cost of capital for companies using those new accounting standards. This effect is anticipated by economic theory and validated through empirical research (see UKEB report, Appendix B). It is also referred to in the IFRS Foundation’s Conceptual Framework for Financial Reporting and illustrates the rationale for providing standardised financial information.

The UKEB developed its approach to broaden the scope of its own economic assessments when considering whether to endorse new accounting standards for use in the UK. The aim is to assess whether potential capital market benefits could be large enough to enable preparers to recover their implementation costs through better funding conditions on capital markets.

What is the output of the approach?

This approach quantifies market-wide reductions in the cost of capital that would be equivalent in value to the implementation costs that preparers would incur to apply a new IFRS Accounting Standard. The indirect benefits associated with cost of capital reductions would be delivered by either raising new funds in the equity and debt markets or increases in the value of equity and debt already issued.

The approach also sets out a framework to assess whether the results are plausible, for example by comparing them against results of academic research that has estimated the effects of the adoption of IFRS Accounting Standards.

How the approach works

The approach starts by estimating market-wide preparers’ implementation costs associated with the introduction of a new accounting standard.

Then, it considers an assessment of direct benefits for users. This is in acknowledgement that capital market effects, including reductions in cost of capital, would only materialise if users perceive that the new accounting requirements lead to information that is decision-useful.

The UKEB uses a standardised questionnaire to estimate both the implementation costs and the direct benefits for preparers.

Once implementation costs are estimated and benefits for users are ascertained, the approach aims to answer the following question.

What cost of capital reduction would be needed for preparers to recover implementation costs in the long-term?

To answer this, a simple mathematical model is used to assess how, for both equity and debt public securities markets, cost of capital reductions would affect:

- the stock of existing capital; and

- anticipated future capital flows.

The focus on public markets acknowledges that:

- the legal requirement to use IFRS Accounting Standards applies to the consolidated financial statements of companies with equity or debt instruments listed on public capital markets; and

- private capital providers typically rely less on financial statements because they have access to private information.

The following table provides a visual representation of the effects identified.

Capital market effects considered in the approach

Equity Debt |

Debt |

|

|---|---|---|

Stock: securities already issued |

Increase in market capitalisation. |

Increase in the outstanding value of corporate bonds. |

Flow: securities to be issued in the future |

Decrease in the cost of equity leading to more projects funded through public equity. |

Decrease in the cost of debt leading to more projects funded through publicly traded corporate bonds. |

Caption: Endorsement of IFRS Accounting Standards: an approach to estimating capital market, page 13.

What the approach doesn’t do

The approach aims to provide evidence on capital market effects that may materialise as a result of adopting a standard for use in the UK. It is not used on its own to decide whether a standard is conducive to the UK long-term public good. Instead, the UKEB would consider evidence obtained by applying the approach alongside the broader evidence base collected to support an adoption decision.

Because the effects are assessed at a market-wide level, the approach does not indicate how individual entities are likely to be affected. So, for example, if a given standard is anticipated to deliver a market-wide reduction in the cost of capital, individual entities may experience cost of capital increases or reductions depending on their specific circumstances.

Finally, it is important to note that the approach is applied before a standard is implemented and is not suitable for making predictions of future price trends or cost of capital reductions associated with the implementation of a given standard.

Summary of the output

Utilising up-to-date market data from LSEG Workspace and the London Stock Exchange, the UKEB calculated the cost of capital reductions needed to recover hypothetical amounts of implementation costs (eg, £100m or £200m).

For example, the UKEB estimated that each of the following cost of capital reductions would be enough for preparers to recover a hypothetical amount of £200m of implementation costs in the long run:

- a decrease in the market-wide cost of equity by 0.03 basis points (BPs - a basis point is a hundredth of a percentage point.) would lead to a £200m increase in market capitalisation (see Cost of Capital report, paragraphs 2.30-2.35);

- a decrease in the market-wide cost of equity by 4.4 BPs would lead to a £200m increase in the present value of funds issued on public equity markets (see Cost of Capital report, paragraphs 2.36-2.44);

- a decrease in the market-wide cost of debt by 1.2 BPs would lead to a £200m increase in the outstanding value of bonds (see Cost of Capital report, paragraphs 2.57-2.60); or

- a decrease in the market-wide cost of debt by 1 BP would lead to a £200m increase in the present value of funds issued on public corporate bonds markets (see Cost of Capital report, paragraphs 2.61-2.67).

The effects described in the table earlier may occur concurrently, in which case:

- lower absolute amounts for the individual effects would be observed but still add up to be equivalent to the example of £200m of implementation costs recovered; and

- the relative contribution of each effect would be assessed on a case-by-case basis.

We invite you to read the Endorsement Criteria Assessment of IFRS 18 Presentation and Disclosure in Financial Statements (paragraphs 4.85 - 4.100), where the approach was used for the first time to produce evidence relevant to the board’s decision-making.

Next steps

The UKEB is seeking feedback (see UKEB project page) on the approach to improve it, for example by expanding to other capital market effects.

The UKEB welcomes interactions with stakeholders: preparers, users, auditors and, most importantly, national and international standard-setters who may see the value of implementing a similar methodology as part of their own assessments.