Daniele Majorana explains why recent developments, including the agreement of a side-by side (SbS) system in response to United States (US) concerns, suggest that pillar two has the necessary flexibility to achieve its goals.

A century after the League of Nations established the foundations of international tax cooperation — transfer pricing and the permanent establishment — it is widely accepted that the system, which was designed for an era of “bricks and mortar” economies, can no longer cope with multinational groups whose value mainly lies in intangible assets. Pillar two is an ambitious effort to fill that structural gap, not by reforming the old framework, but by setting a minimum effective tax rate beneath it.

Multinational enterprises operate seamlessly across borders, but corporate taxation remains organised along national lines. This structural mismatch has the potential of allowing large corporate groups to shift profits to low-tax jurisdictions, weakening public finances and heightening tax competition between countries.

How pillar two works

Pillar two marks the first serious effort to address this issue at its core. Its aim is not to standardise corporate tax systems or create a global tax authority but to endorse a politically achievable principle: large multinational corporations should pay at least a minimum tax on their profits in each jurisdiction where those profits are earned. This minimum was set at 15% — a baseline below which tax competition cannot go — reflecting the fair value of taxation attainable across many countries.

From the outset, pillar two was crafted as a coordinated framework of domestic regulations rather than a binding international treaty. Countries retain sovereignty over their tax systems but agree on a common structure that prevents undertaxed profits from completely escaping taxation. The mechanism determines the effective tax rate (ETR) for each jurisdiction where a multinational operates. If the rate in a particular country falls below 15 per cent, a top-up tax is applied to ensure the total tax paid meets the minimum.

The preferred approach is to enforce the top-up tax in the jurisdiction where profits are generated, through a qualified domestic minimum top-up tax (QDMTT). This preserves taxing sovereignty by preventing other countries from taxing profits created within that jurisdiction. If this does not occur, the income inclusion rule (IIR) requires the ultimate or intermediate parent entity to pay a top-up tax on its share of low-taxed foreign income, linking pillar two to residence-based taxation. If neither country acts, the undertaxed payments rule (UTPR) serves as the backstop, reallocating any uncollected top-up tax to jurisdictions where the group has employees and tangible assets.

Essentially, pillar two ensures that relying on low taxation in one jurisdiction as a lasting benefit is no longer feasible, since another jurisdiction will ultimately collect the tax revenue.

The OECD/G20 Inclusive Framework (IF), agreed in 2021, was hailed as a significant achievement but rested on fragile political foundations, particularly with respect to the US.

Pillar two in the UK

As part of the pillar two agreement, the government has introduced two new taxes in the UK: the domestic top-up tax; and the multinational top-up tax. For further information, see ICAEW’s TAXguide 06/23.

US concerns

Unlike many other countries, the US already implemented a minimum tax on foreign profits through its global intangible low-taxed income (GILTI) regime. GILTI requires US shareholders of controlled foreign corporations (CFCs) to include in US taxable income a portion of those CFCs’ foreign profits, to the extent such profits exceed a normal return on tangible assets and are taxed at low foreign rates. However, the regime differed fundamentally from pillar two: it was applied on a global, blended basis rather than on a country-by-country basis and allowed generous offsets for tangible assets. Aligning it with pillar two would have required congressional approval and a willingness to accept international limits on US tax sovereignty.

Those constraints came sharply into focus with Donald Trump’s return to the presidency in January 2025. One of the first acts of the new administration was an executive order stating that the OECD global tax deal held no legal force in the US without congressional approval. The administration framed pillar two as an extraterritorial threat to US companies and instructed the Treasury to consider countermeasures against countries that apply pillar two rules to US-parented groups.

The confrontation escalated rapidly. Draft legislation considered retaliatory tax measures against foreign companies from jurisdictions perceived to be discriminating against US multinationals. The UTPR became a specific point of dispute. From the US perspective, it appeared to be a mechanism for other countries to tax US profits without US approval. From other countries’ perspective, it was an essential backstop to ensure the credibility of the minimum tax.

The SbS approach

Many observers feared that pillar two might collapse. However, what happened was not a collapse but an adaptation. Instead of demanding strict symmetry, the OECD IF moved towards a practical compromise: the SbS approach. This system recognises that some countries, most notably the US, will not formally adopt the pillar two rules as they are written. Instead, pillar two operates alongside certain national minimum tax regimes, provided they pursue similar aims and achieve broadly comparable outcomes. In practice, US-parented groups are shielded from some pillar two enforcement rules — especially the IIR and UTPR — once the SbS safe harbour applies.

Crucially, this does not dismantle the global minimum tax. It preserves the most important element: QDMTTs applied by source countries. Where a country has adopted such a tax, it can still impose a 15% minimum on profits generated within its territory, regardless of the multinational’s nationality. US companies operating in those countries remain subject to the minimum tax at source. What changes is the reliance on cross-border backstop rules to enforce the minimum.

This shift explains much of pillar two’s resilience. Instead of relying on parent jurisdictions to tax foreign profits, the system increasingly relies on source jurisdictions to tax profits locally. Many jurisdictions, including several traditionally low-tax countries, have adopted domestic minimum taxes to safeguard their tax bases. A considerable portion of the minimum tax is now collected locally, reducing the reliance on contested extraterritorial enforcement mechanisms. The revised framework also features simplified calculations and safe harbours for clearly high-tax situations, enabling both businesses and tax authorities to concentrate their efforts where they are most effective.

UK position

In a statement to Parliament, Dan Tomlinson, Exchequer Secretary to HM Treasury (XST), welcomed the reforms to pillar two and confirmed that measures to implement the changes in UK law will be subject to technical consultation and then brought forward in a future Finance Bill. Once enacted, the changes will apply for accounting periods beginning on or after 1 January 2026.

The ETR test and tax incentives

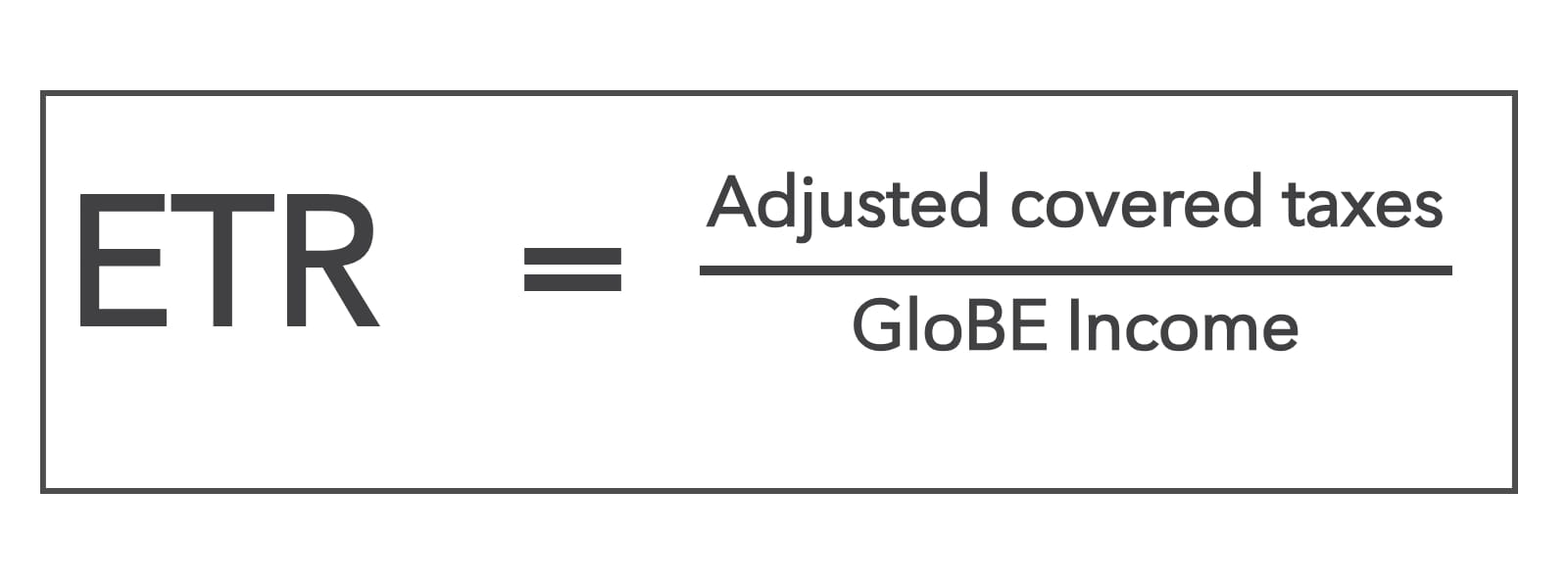

A separate but related issue concerns how pillar two interacts with tax incentives. The framework does not ask whether a tax break is linked to what may be regarded as good policy goals such as innovation or green investment. Instead it reduces everything to a single test: are profits in each country taxed at least 15 per cent? However, what matters is how an incentive affects the ETR, calculated as follows:

- Adjusted covered taxes refers to the taxes the group pays in that country after Global anti-base erosion (GloBE) adjustments.

- GloBE income reflects the group’s accounting profits in that country, based on financial accounting net income or loss (FANIL) rather than domestic tax regulations. The calculation is performed separately for each jurisdiction and compared with the 15% threshold. If the result exceeds the threshold, no action is taken. If it falls below the threshold, a top-up tax is applied in the following order: QDMTT, then IIR, and then UTPR.

Every incentive is assessed based on its mechanical effect on this portion. Non-refundable tax credits — conditional discounts that lower the corporate tax bill only when a company has taxable profits — reduce taxes while leaving profits unchanged, resulting in a lower ETR that may drop significantly below 15%. Pillar two aims to address this exact scenario. In contrast, refundable tax credits - paid in cash or as sellable assets and not contingent on future profits - are treated quite differently, with the pillar two rules reclassifying them as income rather than a tax reduction. The tax rate might decrease slightly, but it is not compromised. This enables governments to support investment, research, or environmental objectives in a transparent, budgeted manner that aligns with the global minimum tax. The same principle applies to deferred taxes: incentives relying on future profits are approached cautiously, and if those profits do not materialise, the earlier tax benefit is revoked.

Pillar two does not ban tax incentives. Instead, it shifts the burden of cost. If incentives reduce the ETR below 15%, the benefit is offset by additional tax, often collected by the same country through a QDMTT. Governments can still offer incentives, but they must do so transparently. This approach ensures that pillar two aligns not with corporate tax rates but with the consequences of tax reductions, prioritising transparency over secrecy and cash support over hidden tax breaks. The SbS package further adjusts this by allowing, within limits, the inclusion of certain substance-based incentives in the ETR calculation, thereby reducing resistance from countries that rely on non-refundable credits, particularly the US.

What this means for pillar two

Pillar two has survived not because it was applied uniformly, but because it proved flexible enough to accommodate political realities without abandoning its core objective. The global minimum tax in place today is less elegant than the original plan but is also more resilient. The US challenge paradoxically strengthened certain aspects of the system by compelling the IF to clarify its priorities, emphasising the importance of domestic minimum taxes as the primary enforcement tool, and exposing the limits of coercion in international tax cooperation.

However, vulnerabilities remain. The SbS arrangement is explicitly asymmetric: US-parented groups enjoy exemptions not automatically available to others, raising concerns about competitive neutrality. There is also a risk that other countries, principally India and Greater China, which have adopted a wait-and-see strategy, may seek similar carve-outs by designing bespoke minimum tax regimes and demanding recognition. If that process accelerates, the system could fragment into parallel variants, undermining consistency and increasing disputes.

Furthermore, because the compromise gives greater weight to large economies with advanced tax systems, it reduces the incentive for smaller or lower‑income countries to participate fully. Whether pillar two ultimately helps to narrow or instead widen global inequalities in taxing rights remains uncertain.

Alternative approaches

This institutional tension has broader dimensions. As pressures within the OECD process became more visible, parallel discussions intensified at the United Nations (UN) on alternative approaches.

Developing countries often prefer Articles 12A and 12B of the UN Model Convention over pillar two because they address a more immediate problem: how to tax income generated locally and collect revenue directly. Article 12A covers fees for technical services paid to foreign companies without a local permanent establishment; Article 12B does the same for automated digital services. Both rely on simple withholding taxes collected at the time payments are made, providing immediate and predictable revenue that is easier to administer.

These source-based rules strengthen the taxing capacity of developing countries rather than preserving a system that mainly benefits headquarters’ jurisdictions. The growing momentum behind the UN framework reinforced the determination of many OECD members to keep pillar two alive, even in compromised form, to preserve influence over the direction of global tax governance.

Strength in flexibility

Pillar two’s survival through the Trump administration’s challenge illustrates how international tax law evolves in practice. Legal design, political power, and economic interests interact continuously. The global minimum tax did not emerge as a fixed blueprint; it became a living system capable of adjustment under pressure. The SbS approach marks a shift from idealised uniformity toward managed diversity, accepting that not all jurisdictions will move at the same pace or in the same direction.

Daniele Majorana, international tax analyst