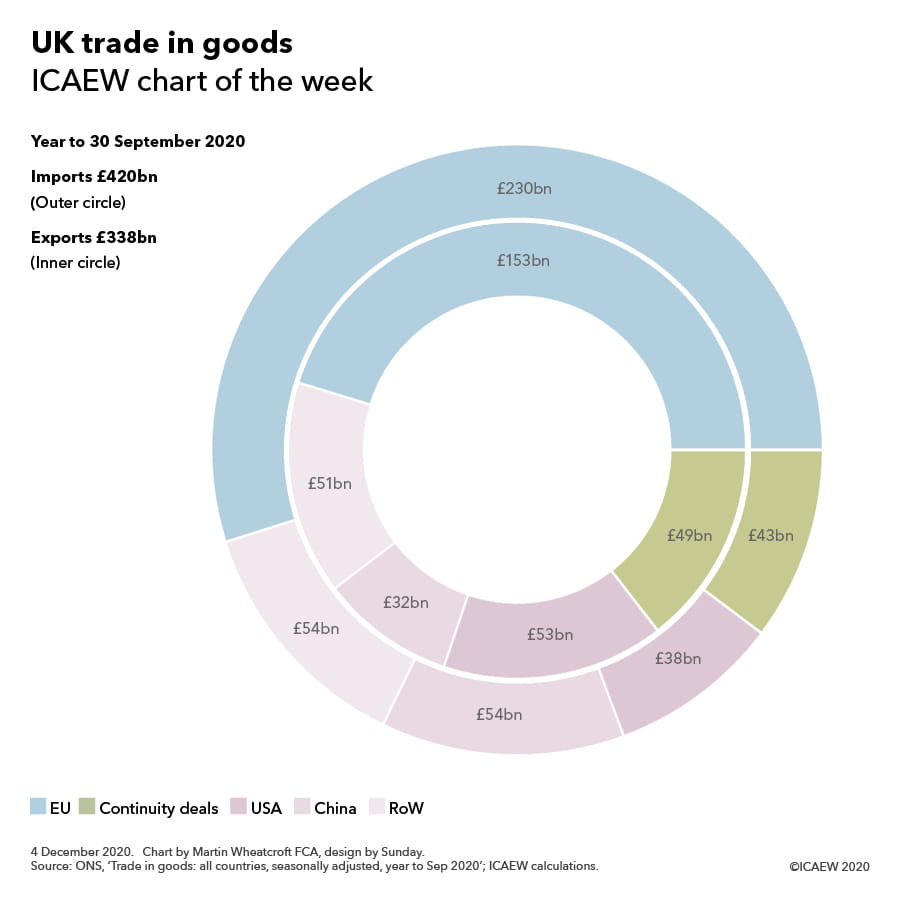

The #icaewchartoftheweek this week is on international trade, illustrating how exports and imports of goods amounted to £338bn and £420bn respectively in the year to 30 September 2020. This excludes £289bn and £181bn of services exports and imports over the same period that are also extremely important, but which are not the principal subjects of the free trade deal currently being negotiated.

The UK’s largest trading partnership for goods is with the members of the EU Customs Union (together with Turkey for non-agricultural products), with the UK exporting £153bn (45% of total goods exports) and importing £230bn (55% of total goods imports).

This is followed by a further £49bn (15%) of exports to and £43bn (10%) of imports from 52 countries that have trade deals with the EU that the UK has been able to agree replacement trade arrangements with. These include Norway, Switzerland, Japan, South Korea, Canada and South Africa, with discussions underway to roll-over trade deals with a further 13 countries not included in these numbers, in particular with Singapore and Vietnam.

The UK’s two largest individual trading partners are the USA and China, where the UK will continue to trade on World Trade Organisation (WTO) terms. The UK exported £53bn (16%) of goods to the USA and imported £38bn (9%) in the year to September, while it exported £32bn (9%) to China and imported £54bn (13%).

The balance of goods trade, comprising exports of £51bn (15%) and imports of £54bn (13%), is with over 130 other countries and territories where the UK does not have a trade deal in place for after 1 January 2021, including India, Russia, Vietnam, Taiwan, the UAE, Saudi Arabia, Qatar, Thailand, Singapore, Australia, Malaysia and Nigeria.

Both exports and imports of goods have reduced in the year to September 2020 compared with a year previously, with exports down 7% and imports down 18%. The principal driver of the fall is the coronavirus pandemic, although reconfiguration of cross-border supply chains ahead of the end of the transition period may also be a factor.

Although global trade is expected to pick up in 2021 once covid-19 vaccines are widely available, there is significant uncertainty as to the effect on trade of the UK’s departure from the Single Market and Customs Union – with or without a deal. Either way, increased trade frictions are likely to have at least some impact, while the imposition of tariffs in the event of no deal could cause significant additional problems for key sectors such as car manufacturing and agriculture.

The size and closeness of the EU economy means that it will continue to be the most important trading partner for the UK whatever is agreed. If only we knew on what terms we are going to be trading in less than a month’s time and what the major changes that are coming in January will mean for the future!