The Chancellor had already announced an increase in the health budget from the proceeds of the health and social care levy, but as highlighted by our chart last week, this implied a very tough budget settlement for most other departments, including cuts for some. Instead, Rishi Sunak was able to use some of the upward revisions in the economic forecasts from the Office for Budget Responsibility to add to departmental resource budgets, ensuring that each department receives a real term spending increase in their combined resource and capital budgets even with higher levels of inflation in the coming year.

However, there was a sting in the tail, as supplementary COVID-19 funding ceases at the end of this financial year, leaving departments to absorb further COVID-related expenditure within their budgets from next April onwards. This will include catching up on backlogs built up during the pandemic in addition to any incremental costs that may continue into the Spending Review period.

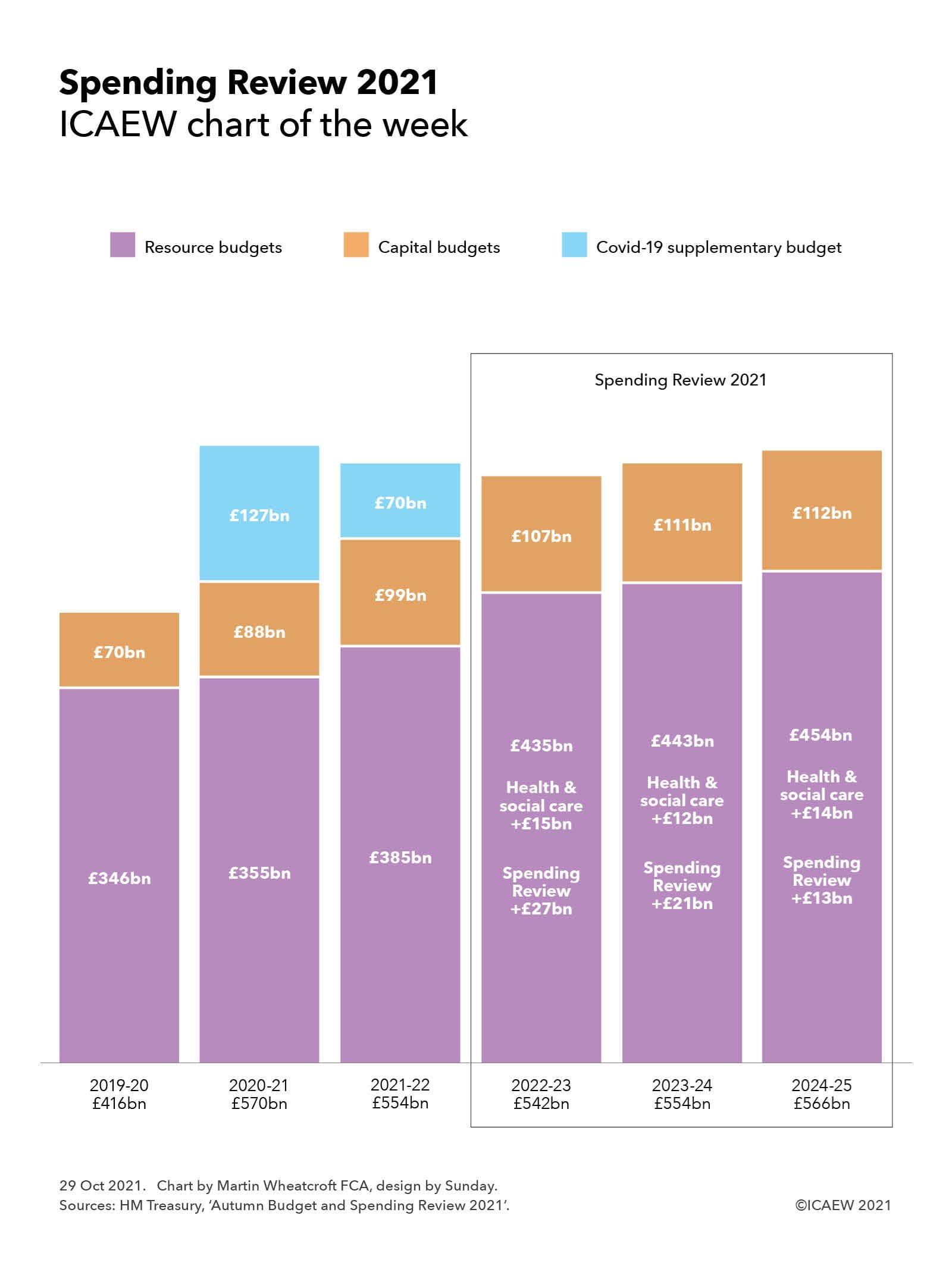

The chart starts by highlighting how departmental resource and capital budgets of £346bn and £70bn in 2019-20, increased to £355bn and £88bn in 2020-21 and to £385bn and £99bn in the current year. This is before £127bn in COVID-19 supplementary budgets last year and £70bn this year.

The Spending Review period itself covers the three financial years 2022-23, 2023-24 and 2024-25, with the combination of funding from the health and social care levy and the Spending Review seeing departmental resource budgets increase to £435bn, £443bn and £454bn respectively. This is more than the spending envelope originally set out by the Chancellor last month.

Capital investment budgets remained broadly unchanged at £107bn, £111bn and £112bn respectively, continuing the significant jump from the £70bn invested in 2019-20 in the coming financial year before flattening out in the following two years.

Over the three years, the resource budget settlement implies annualised average real terms growth in the health & social care budget of 4.1% and in the education budget of 2.2%, while the defence budget is broadly frozen in cash terms and cut by 1.4% in real terms. This assumes average inflation over the three years of 2.2%, with higher inflation in the coming financial year offset by much lower rates in the following two years.

Other departments are expected to grow by 3.1% on average over the period, with central funding for local government up 9.4%, transport up 6.8%, work & pensions up 4.6% and justice up 4.1%, each receiving larger relative settlements than other departments. International trade (+0.1%), HM Treasury (+0.9%), levelling up, housing & communities (+1.1%), HMRC (+1.2%), the Cabinet Office (+1.4%), business, energy & industrial strategy (+1.4%), and intelligence (+1.7%) are the departments receiving increases below 2% a year on average.

Spending Review 2021: Departmental resource budgets (RDEL) excluding depreciation

| 2021-22 £bn |

2022-23 £bn |

2023-24 £bn |

2024-25 £bn |

Average real terms growth | |

| Health & social care | 147.1 | 167.9 | 173.4 | 177.4 | +4.1% |

| Education | 70.7 | 77.0 | 79.0 | 80.6 | +2.2% |

| Defence | 31.5 | 32.4 | 32.2 | 32.2 | -1.4% |

| Large departments | 249.3 | 277.3 | 284.6 | 290.2 | +2.9% |

| Other departments | 70.7 | 83.9 | 82.7 | 82.7 | +3.1% |

| Devolved administrations | 56.8 | 63.0 | 64.3 | 65.3 | +2.5% |

| ODA to 0.7% of GDP | - | - | - | 5.2 | |

| Reserves | 8.1 | 11.0 | 10.9 | 10.3 | |

| Total excluding covid-19 | 384.9 | 435.2 | 442.5 | 453.7 | +3.3% |

HM Treasury, ‘Autumn Budget and Spending Review 2021’

The above growth rates exclude capital budgets, expected to increase in real terms by 1.9% a year on average over the three years of the Spending Review. Departments benefiting from higher budgets include small and independent bodies (+16.8%), FCDO (+16.0%), digital, culture, media & sport (+11.8%), and intelligence (+9.1%), albeit mostly from relatively small bases in each case. The 3.8% average real terms increase in health & social care capital investment is much less proportionately, but much larger in cash terms.

Perhaps just as important as the monetary amounts provided to departments as the Chancellor opened his proverbial cheque book, is the certainty that a three-year budgetary settlement provides. This will help departments plan ahead with confidence and hopefully help them obtain better value for the money they spend on our behalf.

Insights special: Repairing public finances

ICAEW Insights takes a closer look at the efforts being made to repair public finances in the wake of the coronavirus pandemic.

More support

ICAEW Community

Public Sector Community

The go-to place for guidance on issues affecting finance professionals working in and with the public sector. With a range of dynamic services, ICAEW provides valuable tools, resources and support tailored to the public sector.

Resources

Public sector

See the latest insights and support on public sector finance, audit, financial management and financial reporting.

Newsletter

Stay up to date

You can receive regular email updates from ICAEW insights, including weekly or monthly enewsletters, subscribe to whichever works for you.

Sign up