Underwhelming end to 2025

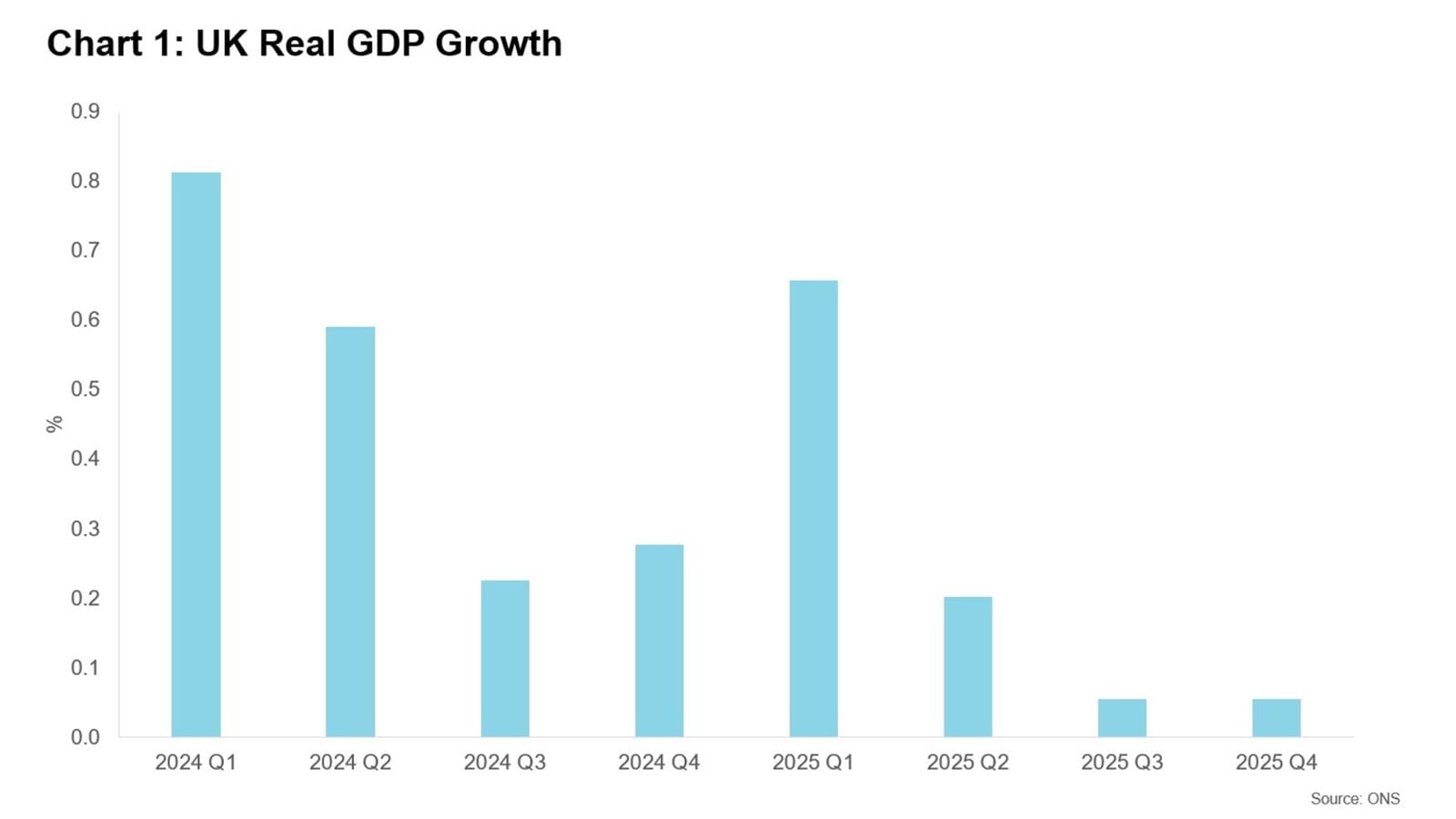

Official figures revealed that the UK economy grew by 0.1% in the final quarter of 2025 (see Chart 1), unchanged from the previous quarter.

The main driver of Q4 growth came from a 1.2% rise in industrial production, driven by Jaguar Land Rover’s return to production following its cyber-attack. The services sector, however, recorded no growth and construction output fell by 2.1%, its weakest since Q3 2021.

Just taking data from December 2025, UK GDP grew by 0.1%, down from growth of 0.2% in November. Looking at the entire year, the UK economy grew by 1.3% in 2025, up from growth of 1.1% in 2024.

UK GDP per head (which divides UK GDP by the total UK population) – a key indicator of living standards as it adjusts for changes in population size – dropped by 0.1% in Q4 2025, the second successive quarterly decline. However, GDP per head increased by 1.0% annually in 2025, following zero growth in 2024.

Business investment fell in Q4

Detailed official GDP data showed that firms had a particularly bleak final quarter. Business investment dropped by 2.7%, as uncertainty caused by the Budget and higher costs caused many projects to be mothballed.

Household spending increased by 0.2% in Q4, down from 0.4% growth in the previous quarter. Government spending was an important driver of GDP growth, increasing by 0.4% in Q4. This mainly reflects increases in expenditure on health, public administration and defence, and social care.

Inflation dropped sharply in January

UK CPI inflation stood at 3% in January 2026, the lowest rate since March 2025, down from 3.4% in December. This was largely driven by a decrease in petrol prices, lower food prices and cheaper airfares also added to the downward pressure on the headline rate.

January’s decline is the start of a period of rapidly falling inflation. Lower food prices and falling energy bills are pulling the headline rate back to around 2% in the spring – helped by the cut to green levies announced in November’s Budget and April’s reduction in Ofgem’s energy price cap.

Young people bear brunt of weak labour market

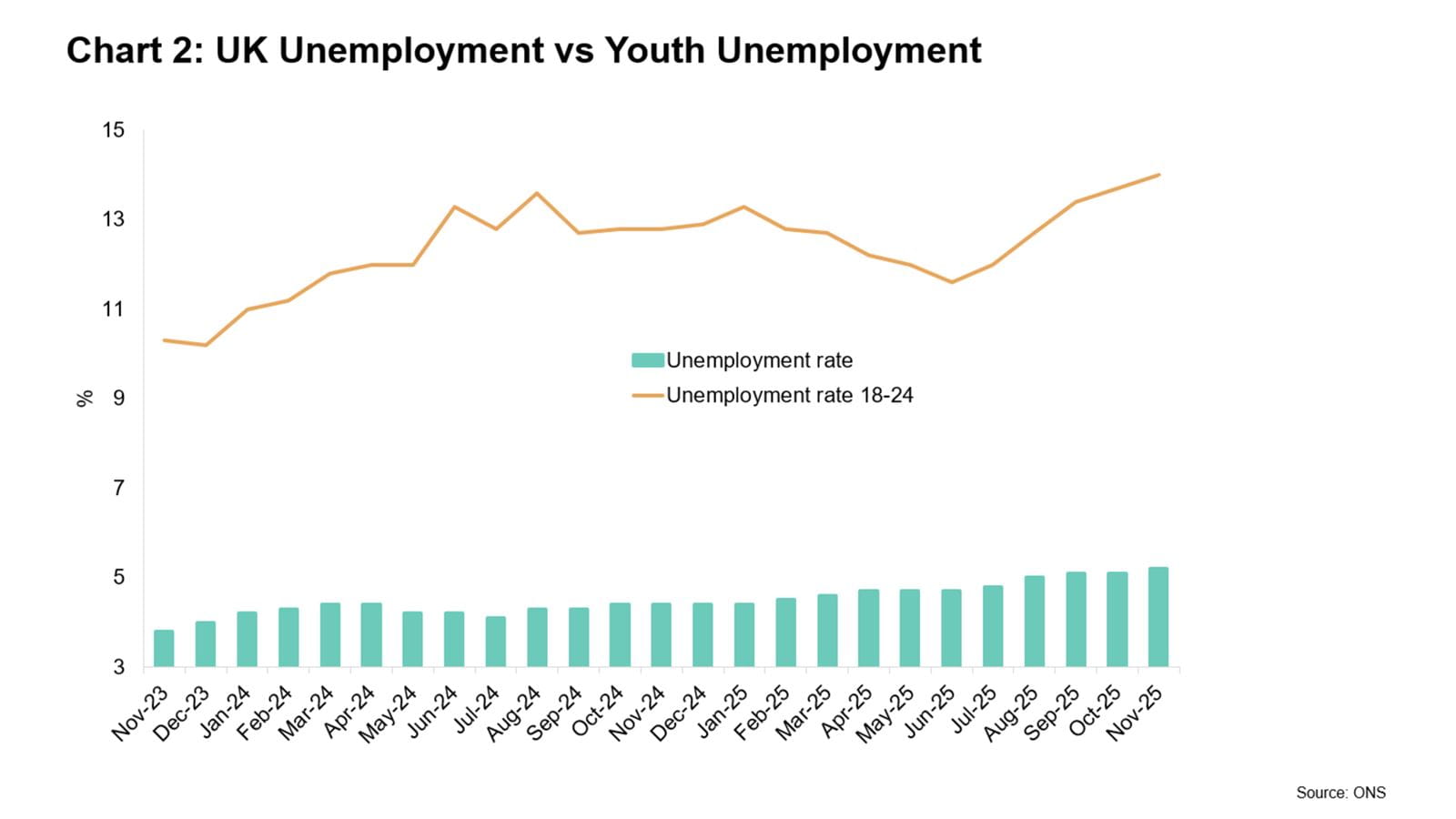

The UK’s unemployment rate rose from 5.1% to 5.2% in the three months to December 2025; the highest rate since the first quarter of 2021.

Young people in particular are struggling to enter the labour market. The unemployment rate among 18–24-year-olds has risen to 14% over the same period, the highest rate since the three months to September 2020 and almost three times the national rate (see Chart 2).

The continued rise in unemployment means competition for vacancies is intensifying with 2.6 unemployed people per vacancy in Q4, up from 1.9 a year earlier. The UK’s labour market will probably face more pain in the year ahead, with elevated staffing costs and worries over the impact of the Employment Rights Act likely to lift unemployment higher.

Record UK trade in 2025

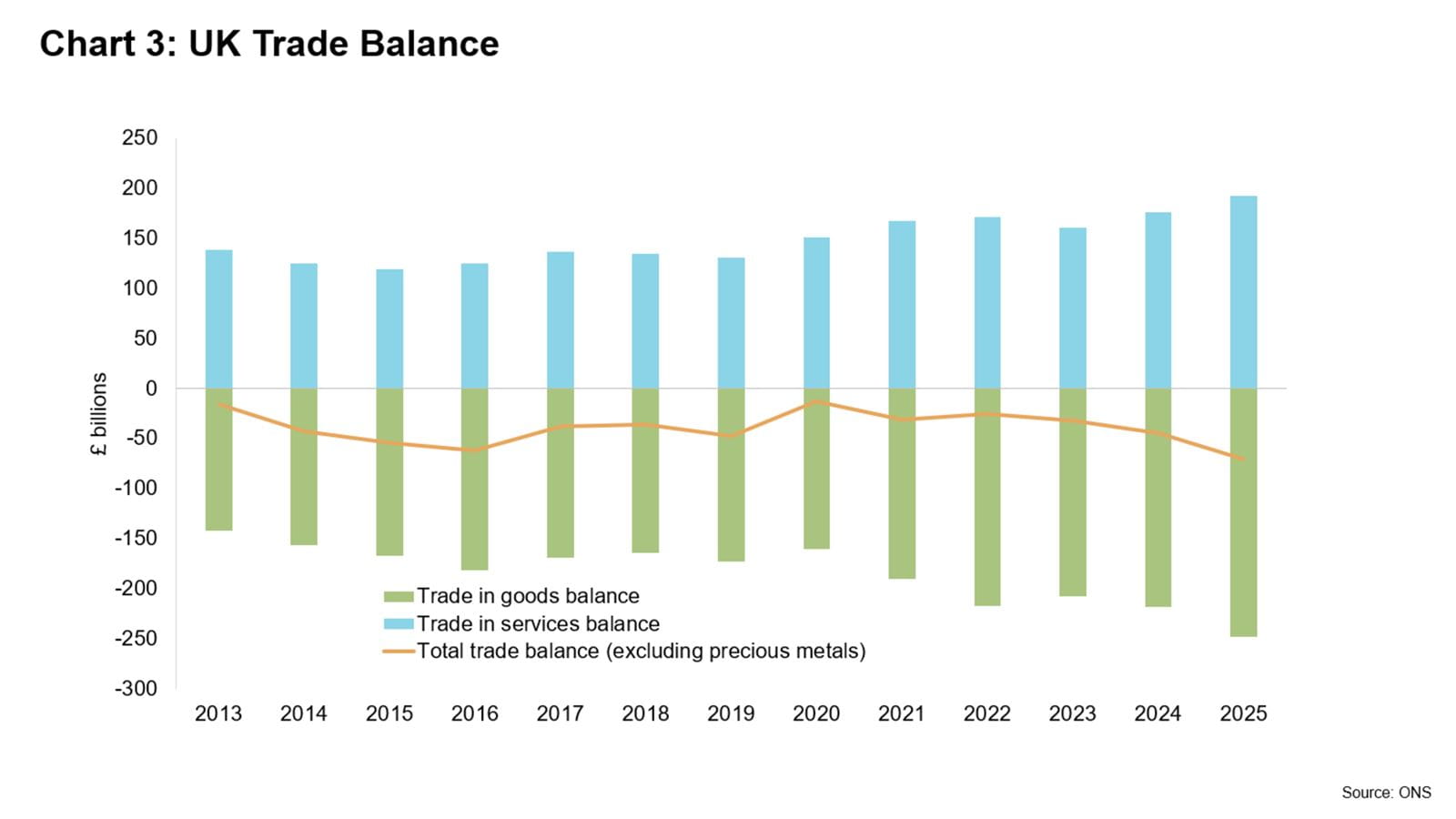

UK’s trade deficit in goods and services narrowed by £3.3bn to £3.8bn in Q4 2025, compared with the previous quarter. For 2025, the UK recorded a trade deficit for goods of £248.3bn, the largest since records began in 1997 (see Chart 3).

The strength of sterling and lower production costs in other countries helped drive more goods to be imported into the UK. In contrast, the UK had a £191.8bn trade surplus in services, also the largest on record, partly reflecting international trade in services rising over goods – a particular benefit to the UK, the second largest exporter of services.

Spring interest rate cut looking likely

At their latest meeting, the Bank of England kept interest rates at 3.75%, with the Monetary Policy Committee member voting five to four in favour of holding rates.

The vote split confirms that the rate-setters remain deeply divided, if inflation falls as expected, there should be a decisively dovish shift within the committee in the coming months, meaning more rate cuts are likely in the spring.

However, a lingering question among policymakers will be whether to pull the trigger in March or April as some may want slightly more evidence of easing inflation before reducing rates.

Implications for accountants, business owners and the economy

The underwhelming end to 2025 caps off another disheartening year for the UK economy with growth tailing off unnervingly quickly after the strong start to last year, as rising taxes, heightened uncertainty and poor productivity increasingly squeezed activity.

However, the UK economy should see slightly stronger growth in the current quarter with reduced uncertainty now the Budget is in the rear-view mirror, and lower inflation likely to boost consumer spending and business activity, despite higher unemployment.

UK economy – what to watch for in February:

- The January 2025 GDP data to be released on 13 March, is likely to show that the UK economy grew modestly at the start of this year.

- On 19 March, the Bank of England’s Monetary Policy Committee could well cut interest rates from their current rate of 3.75%.

- The inflation figures for February, out on 25 March, should see the headline rate slow slightly from the 3.0% recorded in January.

2026 six months in

Further support

Resources

Economy

Expert analysis on the latest national and international economic issues and trends, and interviews with prominent voices across the finance industry alongside data on the state of economy.

Visit the hubResources and support

How to grow

Support from ICAEW on starting, growing and renewing businesses in the UK, and supporting the government's mission of kickstarting sustainable economic growth.

More support Policy recommendationsICAEW support

Training and events

Browse upcoming and on-demand ICAEW events and webinars looking at the global economy and trade.

Events and webinars A-Z of CPD Courses