Our 400th chart of the week is on the average price of petrol and diesel in the UK according to analysis from the RAC Foundation.

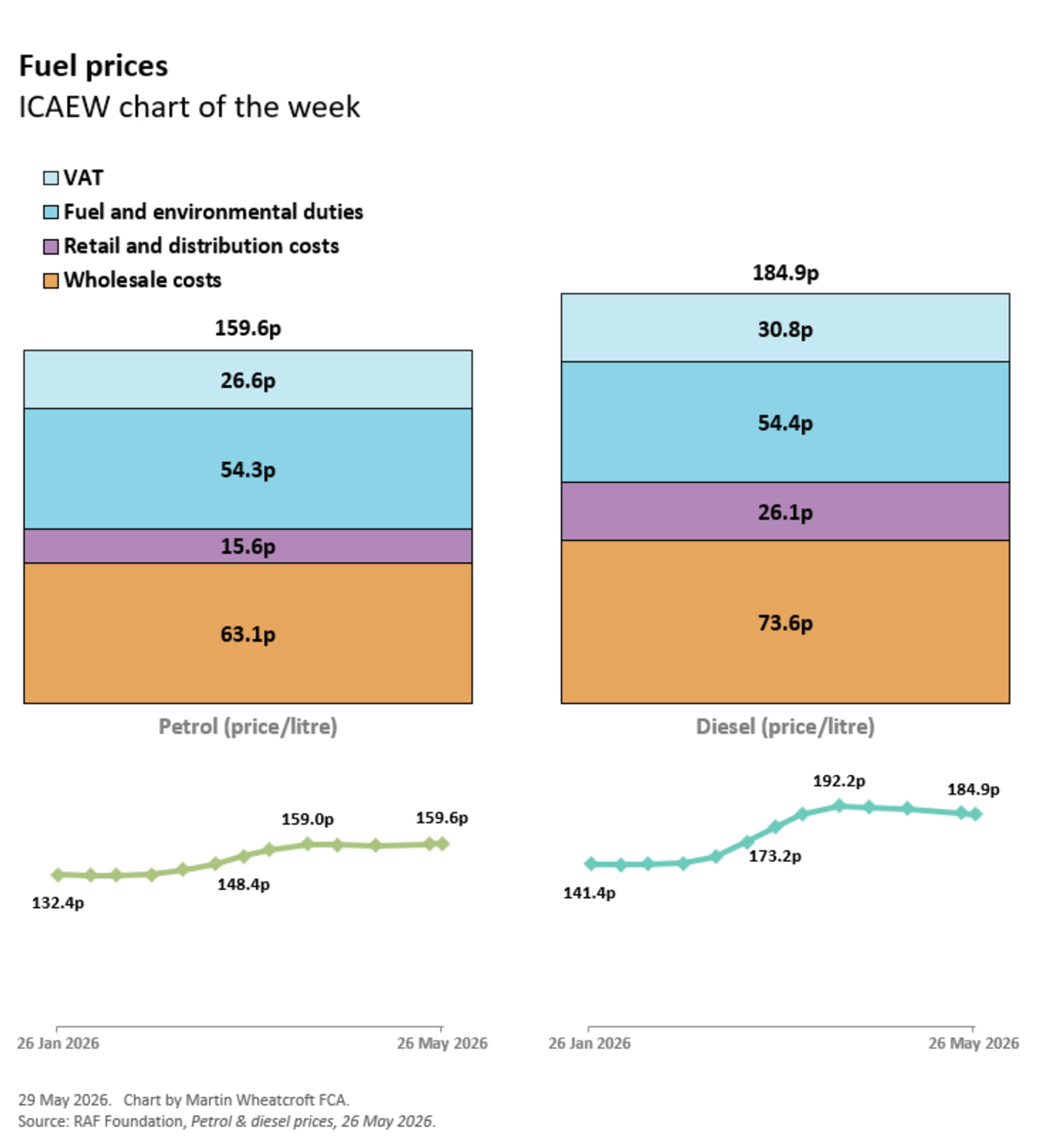

As our chart illustrates, the average price for petrol in the UK on 26 May 2026 was 159.6p per litre comprising wholesale costs of 63.1p (39%), retail and distribution costs of 15.6p (10%), fuel and environmental duties of 54.3p (34%), and VAT of 26.6p (17%).

The average price for diesel on the same date was 184.9p, comprising wholesale costs of 73.6p (40%), retail and distribution costs of 26.1p (14%), fuel and environmental duties of 54.4p (29%), and VAT at 20% of 30.8p (17%).

The wholesale cost of petrol of 63.1p per litre consists of 56.4p for petroleum and 6.7p for the cost of ethanol production and refining, while the diesel price of 73.6p per litre comprises 60.4p for diesel and 13.2p for biodiesel.

Retail and distribution costs of 15.6p for petrol and 26.1p for diesel comprise retail margin (forecourt costs and profit) of 13.9 and 24.0p respectively together with delivery and distribution costs of 1.7p and 2.1p.

Fuel and environment duties of 54.3p and 54.4p comprise fuel duty of 53.0p per litre (net of a temporary 5.0p fuel duty cut) for both petrol and diesel plus 1.3p and 1.4p respectively in greenhouse gas and development fuel obligations.

A sharp shock

Our chart also shows how the petrol and diesel prices have changed over the last four months, rising sharply in March and April following the US and Israel attack on Iran and the effective closure of the Strait of Hormuz but stabilising in May as markets have calmed.

The price of petrol was 132.4p per litre on 26 January 2026, rising to 148.4p on 25 March, increasing to 159.0p on 14 April before dipping slightly and then rising to 159.6p on 26 May 2026.

The price of diesel rose from 141.4p on 26 January to 173.2p on 25 March and 192.2p on 14 April before falling to 184.9p on 26 May 2026.

High and volatile

The general consensus is that fuel prices are likely to remain high and volatile even if there is a peace agreement between Iran and the US and Israel. Wholesale prices are currently being supported by the release of strategic reserves by several nations and a sharp reduction in imports by China, but these are not expected to continue indefinitely.

Even if shipments resume, there will be a time lag before they reach Europe (historically three to five weeks on average) when the constraint will become refinery capacity. Meanwhile, Gulf nations will be looking to recoup the costs of repairing oil and other infrastructure damaged during the conflict in addition to plugging the holes in their domestic budgets caused by the Iranian embargo on their oil exports.

This is the 400th ICAEW chart of the week and it is a shame that it features yet more economic bad news for the UK, in line with many of our charts over the last few years. Let’s hope that things turn around so that our 500th chart in 2028 can reflect a more positive position.

Latest charts

Further resources

ICAEW Community

Public Sector Community

The go-to place for guidance on issues affecting finance professionals working in and with the public sector. With a range of dynamic services, ICAEW provides valuable tools, resources and support tailored to the public sector.

Resources

Economy explainers

ICAEW experts offer simple guides to help understand the technical, economic jargon that is discussed when talking about public finances and the economy.

Find out moreICAEW support

Training and events

Browse upcoming and on-demand ICAEW events and webinars offering support on technical areas, such as assurance, reporting and tax, as well as personal development.

Events and webinars A-Z of courses