Flourishing e-commerce led to a boom in pandemic-era logistics, that’s since been tempered by insular policymaking and shortening supply chains. David Prosser asks if the sector will be going places this year.

Deal-making in the logistics sector should be booming. The World Trade Organization says the value of global trade has risen a pretty incredible 69% over the past five years, from $19trn to $33trn. And e-commerce continues to boom the world over. Geopolitical uncertainty may have been turbocharged over the last 12 months, adversely affecting that global trade, but that’s offset by organisations of all shapes and sizes being compelled to think more deeply than ever before about how to secure supply chains.

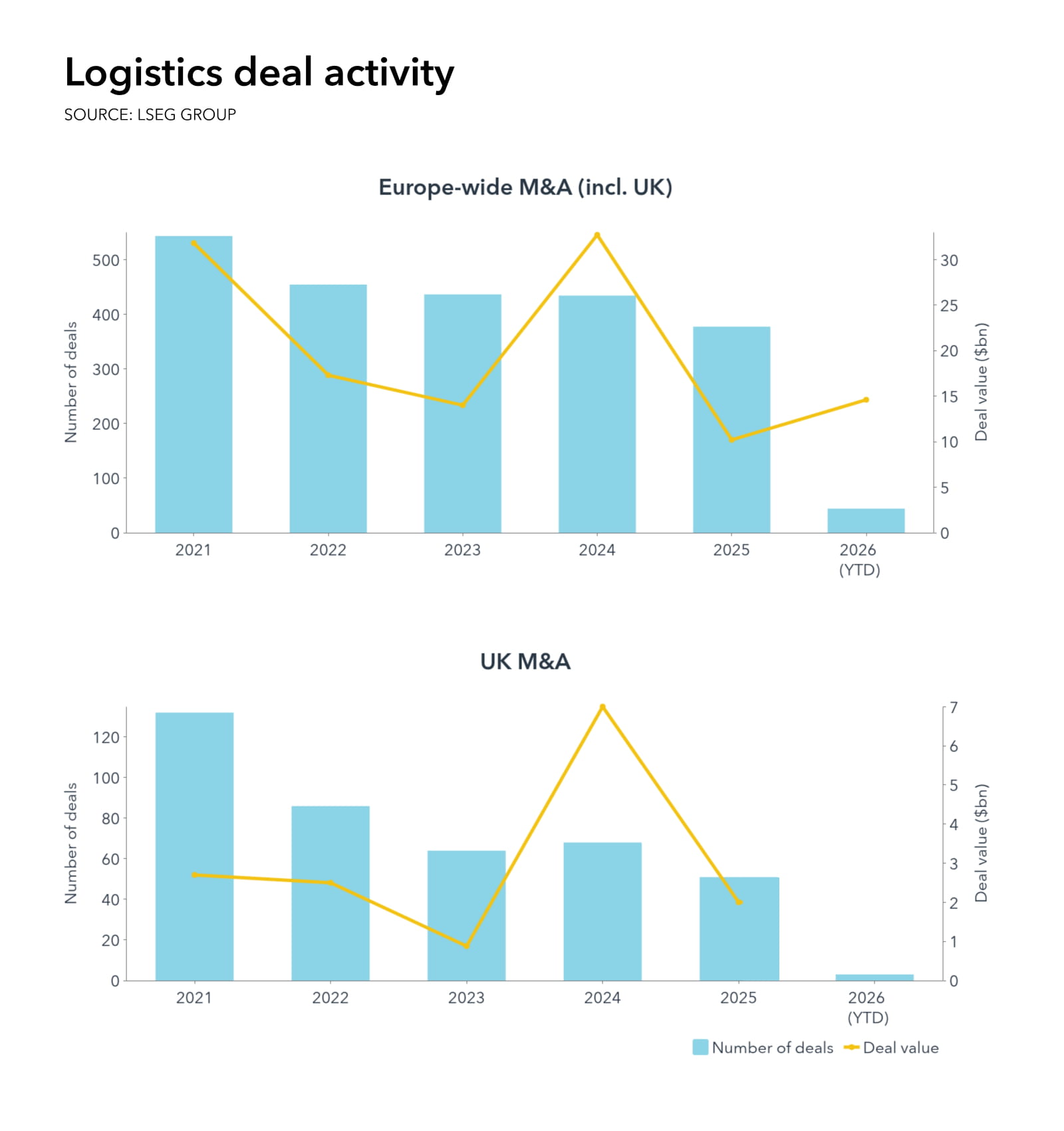

M&A activity in the sector has been inconsistent, however. While 2024 was a strong year, activity hit the brakes in 2025. Data from the London Stock Exchange Group reveals there were 51 M&A transactions in UK logistics and supply chain management last year, versus 68 in 2024, but deal values totalled less than a third of those recorded in 2024.

For the moment, then, geopolitical turbulence and market volatility seems to be making investors circumspect. BDO’s Logistics Confidence Index, published at the end of last year, recorded its lowest reading in the data’s 14-year history. Trade tariff interventions from the US, in particular, generated anxiety last year.

But Jason Whitworth, M&A partner at BDO, believes there’s a flip side to this. “The unprecedented level of uncertainty has naturally generated real frustration. A series of roadblocks to growth has left many feeling under pressure. But our research repeatedly shows deep-rooted resilience in the sector and an ability to bounce back from adversity, with many operators taking the opportunity to drive change,” he says.

“As we accelerate into 2026, there is a sense of stabilising confidence and of M&A pipelines starting to build,” adds Whitworth. “We are anticipating increased activity driven by technological advancements, e-commerce growth, sustainability initiatives, globalisation and the need for consolidation.”

Delivering change

The logistics sector is under pressure to embrace digitalisation and decarbonisation as demand accelerates. In a highly fragmented sector, M&A could be a shortcut to achieving that transformation.

For strategic investors, an acquisition can mean they avoid the investment required and management resource needed to carry out such a transformation in-house. When Danish logistics firm DSV acquired Germany’s DB Schenker for €14.3bn last April, following a bidding war with rivals including Maersk and MSC, it doubled the size of its business.

Other major deals at the European level last year included Ceva Logistics’ acquisition of the warehousing and transportation arm of Turkish firm Borusan Tedarik for $383m, and France’s Jacky Perrenot’s acquisition of Vos Logistics of the Netherlands. In the UK last year, corporate transactions included the sale of technology business J&J Global Fulfilment to QLS Group, and Stolt-Nielsen’s acquisition of Suttons International.

Deal activity is also being driven by the growing interest of PE investors in the sector. Traditionally less keen on asset-intensive businesses, PE firms have now woken up to the value of the opportunity in logistics, says Daniel Wright, M&A sector lead for transport and logistics at Deloitte. “They see the opportunity, given the massive importance of logistics to the global economy,” he says. “And in the UK, there’s a huge consolidation play.”

Taking a bullet

Panoramic Growth Equity invested in Bullet Express in 2023, working with Maven Capital Partners and Emerald Capital Management to back a management buyout at the firm, led by managing director John McKail. Founded in 1990 by David McCutcheon and Gary Smith, Bullet Express started out with a single vehicle. Today it offers both warehousing and distribution services, including specialist services tailored to individual company needs, international freight forwarding and bonded/secure storage.

“It’s a recurring theme in the logistics sector,” says Panoramic’s Katie Ford. “There are a large number of founder-owned businesses where the founders are now looking for a managed exit, either to a management team or a trade buyer; private equity interest in such opportunities has started to ramp up.”

Panoramic’s investment is intended to support both organic growth and M&A activity, as the company pursues a buy-and-build strategy. “The key is to get the basics right from the start,” adds Ford. “We’ve already done a lot of work with the business on the technology piece, updating its systems and supporting investments in areas such as data.”

Breadth is also important, adds Ford. “One attraction of Bullet is that it has multiple service offerings,” she says. “It offers straightforward distribution, including through partners in the Pall-Ex network, so it has full national coverage, but it can also do specialist contract work – and it offers specialist warehousing as well.”

It’s a recurring theme in the logistics sector

A worldwide web

At a global, big-ticket level, PE investors including BlackRock, Macquarie and Blackstone have all done multibillion-dollar deals in recent months, respectively acquiring 43 ports from CK Hutchison ($22.8bn), Australia’s Qube Logistics ($8.3bn), and Safe Harbor Marinas of the US ($5.7bn).

In the UK mid-market, meanwhile, firms such as Northwood Investors – which has acquired 12 ‘last-mile’ logistics assets across the UK – are increasingly pursuing platform strategies. They focus on the efficiencies and opportunities that come from pulling together multiple small players. In an industry with thousands of owner-operators – often older owners whose children aren’t keen to take on the business – there is plenty of choice.

Succession planning pressures and retirement-driven exits are accelerating activity

M&A opportunities in the sector are increasing and attractive valuations are part of the appeal, says Nicholas Buxton, a director in Investec’s direct lending team. “The drivers of the increase are twofold,” he says. “Succession planning pressures and a wave of retirement-driven business exits are accelerating activity in the sector, as owners seek liquidity and continuity while larger players pursue consolidation and scale. In addition to this, cost pressures from increased staffing, energy and other costs have impacted what can, in some cases, be low-margin businesses, with these issues compounded when a business lacks scale.”

These factors, he adds, have driven down valuations, meaning strong businesses continue to come up for sale at good prices: “These opportunities are particularly interesting to those looking to execute a buy-and-build strategy, or who already have a scaled platform that they can plug into.”

International shift

Consolidation isn’t only a domestic story, with many large players also looking to expand their geographic footprints and move into new modalities and services lines. When Switzerland’s MSC Group acquired Maritime Transport, the UK’s largest haulier, in late 2024, for example, it didn’t just boost its exposure to the UK – it also increased its road and rail capabilities.

The very largest global logistics operators already offer a one-stop shop, providing cross-border solutions that may span multiple modes of transport and include last-mile delivery. But other players are now using M&A to acquire similar coverage in many markets.

Another trend is for logistics operators to look beyond established verticals for new opportunities in more specialist areas. In the pharmaceuticals sector, for example, carefully controlled environmental conditions are often required for shipping and storage. Hence UPS’s November 2025 acquisition of Canada’s Andlauer Healthcare Group, which runs temperature-controlled facilities across North America, for $1.6bn. And, in Europe, Yusen Logistics’ acquisition of four pharmaceutical logistics operations, spanning 12 countries, from Walden last December.

Combining logistics businesses, then putting new tech capabilities in, offers huge potential upside

Combining entities can improve margins and efficiency, but perhaps the biggest potential gains are to be found by investing in specialist technology, says Deloitte’s Wright: “If you’re putting these businesses together, and then putting some new technology capabilities in there, there is a huge potential upside.”

Harnessing tools such as automation, AI and the Internet of Things, modern logistics operations now have much greater tracking capabilities, supporting superior customer services. Route-optimisation solutions, often cross-border and spanning multiple modes of transport, can deliver substantial savings. The blockchain improves supply chain security, as well as supporting traceability.

Indeed, data from BDO’s Logistics Confidence Index report shows that in some quarters of last year, technology-related logistics deals accounted for more than a third of transactions. Notable examples included Maven Capital Partners’ £3.4m investment in logistics software business Epod Solutions, Palatine Private Equity’s acquisition of retail logistics platform Fulfilmentcrowd, and Whiterock’s Growth Capital Fund’s minority investment in Mantis, an AI-driven fleet safety and risk intelligence company.

Driven by tech

As the logistics sector comes under mounting pressure to reduce its carbon emissions, new decarbonisation technologies will become crucial. Electrification in the UK is currently largely confined to smaller vehicles, typically for last-mile delivery, but developments in battery technology may yet transform longer-haul journeys. Meantime, route and load optimisation software could provide an easier way to reduce carbon footprints.

In the UK, freight accounts for 31% of the transport sector’s carbon emissions, but digital infrastructure projects have delivered promising results in reducing that. One initiative, led by innovation group Digital Catapult, suggested that sharing data across the industry could support more intelligent vehicle slot filling, routing, and tracking – and that greater collaboration could cut emissions by up to 30%.

Katie Ford, senior investment manager at Panoramic Growth Equity, says such initiatives could also make the sector more attractive to PE investors. “Logistics has been seen as a dirty industry, which has often proved challenging for PE,” she says. “But we are now seeing progress – from more accurate emissions tracking to a wide range of improvement initiatives, such as the reuse of water in warehousing.”

In other words, there is the potential here to create a virtuous circle of M&A, with consolidation, capital investment and digitalisation combining to create a new generation of more efficient – and environmentally friendly – logistics businesses. Which would, in turn, catalyse further consolidation.

Deloitte’s Wright says the signs of a potential recovery are there. “From a macro perspective, the current geopolitical situation adds a layer of complexity, but we are cautiously optimistic,” he says.

“We’re already seeing a good level of M&A activity with deals yet to be announced and if investors and strategic buyers can get comfortable about the investment case, around the efficiencies available, and the potential of technology, that will increase the appetite for deals.”

Debt becomes them

Banking group Investec has become an increasingly important provider of debt finance to the UK’s logistics sector, participating in a series of notable deals. Debt is an important part of many M&A transactions in the sector, providing acquirers with agility and firepower to execute their post-deal organic and inorganic growth visions.

Last year, Investec provided debt facilities to support DBAY Advisors’ acquisition of The Alternative Parcels Company (APC), and backed Next Wave Partners’ refinancing of The Delivery Group.

The company is also a longstanding lender to both Palletforce and Walkers Transport, prominent freight businesses based in Staffordshire and West Yorkshire respectively. It has also funded The Coach Travel Group, a Berkshire-headquartered business that operates a number of regional coach operators across the UK – carrying people rather than freight, in other words.

In January, the bank announced its first loan in the storage sub-sector of the logistics industry – an £11.3m facility to support Kennedy Wilson in its acquisition and redevelopment of a site in south London.

“Investec can provide debt facilities to cater for a range of strategies,” says Nicholas Buxton, director in Investec’s direct lending team. “For M&A transactions this typically consists of acquisition finance to get the deal done, follow-on funding to support growth capex and/or acquisitions and working capital facilities. We are also able to provide financing to the sector at a fleet/machinery and property level via our Asset Finance and Real Estate teams.”