Q2: Business confidence in the East of England deteriorates as the Iran War weighs on the outlook.

The latest national Business Confidence Monitor (BCM) shows that the Iran War significantly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 13 April to 19 June 2026.

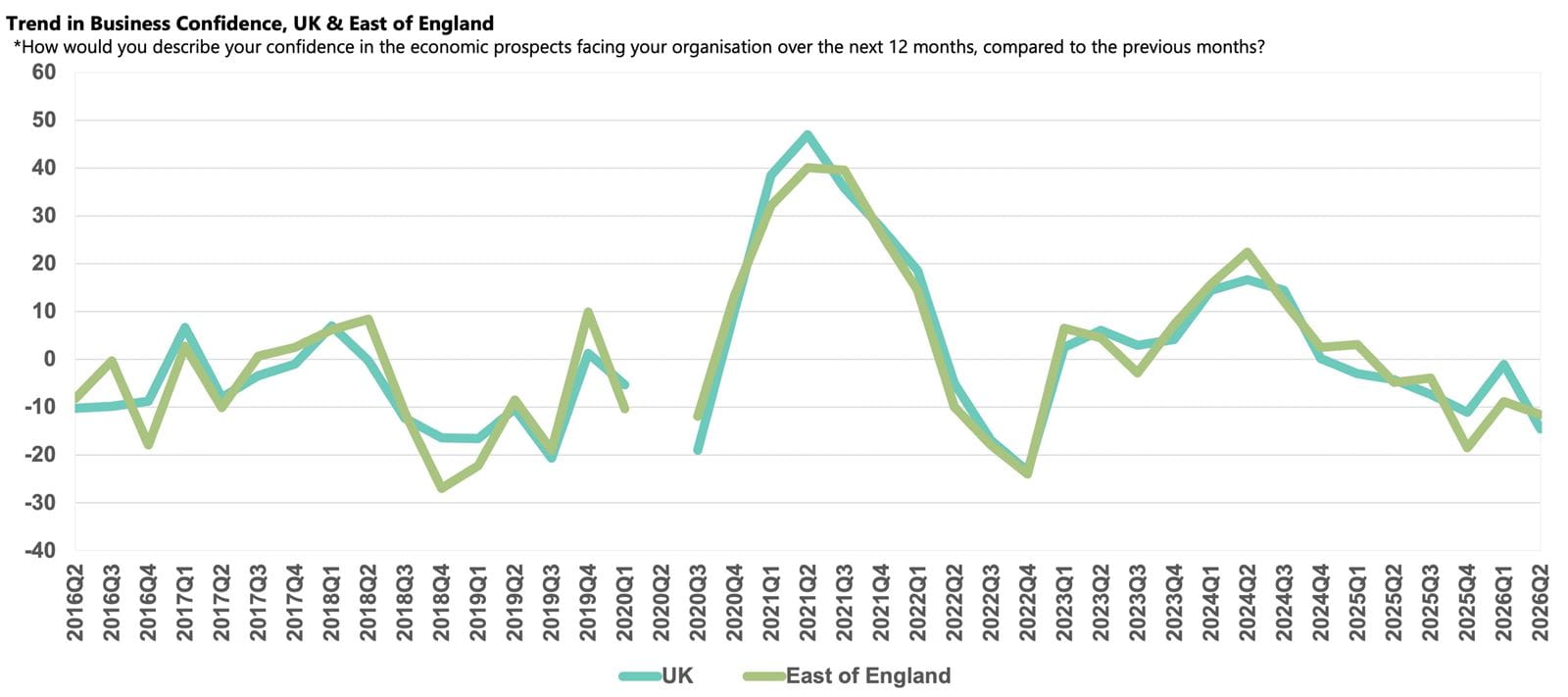

- Business confidence in the East of England fell to -11.6 from -8.8 in Q1, but above the UK average (-14.6).

- Domestic sales and exports continued to grow steadily in the year to Q2 2026 and businesses are optimistic they will gain momentum next year.

- Geopolitical risk was the main rising challenge, followed by labour costs, while transport problems were more widely cited than in any other region.

- Annual salary growth edged up and businesses expect to raise pay above the UK rate in the coming year.

- Businesses pushed up selling price inflation amid rising input cost pressures.

- Companies are becoming increasingly cautious about capital investment and plan to significantly scale back growth.

Business confidence in East of England

Business sentiment in the East of England eased in Q2 2026, with the Business Confidence Index edging down from -8.8 in Q1 2026 to -11.6. The decline in confidence was much less severe in the East of England than in many other regions, and the score was above the UK average (-14.6) but remained below the regional historical average (+3.6).

While confidence in the region was likely buoyed by above-average annual domestic sales growth, the Iran War and the closure of the Strait of Hormuz fostered widespread uncertainty and significantly undermined confidence among companies in the East of England. The rise in oil and gas prices caused a spike in input prices for businesses and disrupted their supply chain activity. Geopolitical uncertainty and the rise in energy costs added to existing concerns about the cost of doing business, particularly labour costs and the tax burden.

Domestic sales and exports growth

Annual domestic sales growth was steady in the East of England at 3.7% in Q2 2026, it broadly tracked the national average (3.6%) and outperformed the region's historical norm (3.1%). The locally important Business Services sector likely supported annual sales growth this quarter, offsetting some of the weakness reported by Manufacturing & Engineering businesses. Companies are reasonably optimistic about the year ahead, projecting growth of 4.4%, though this is weaker than the 4.7% rise forecast nationally.

Annual exports growth in the region was also steady at 3.3% in Q2 2026, broadly in line with the 3.1% rate recorded nationally. Strengthening exports contributions from the IT & Communications sector in the year to Q2 2026 probably offset some of the underperformance reported by the Manufacturing & Engineering sector. Businesses predict a pick-up over the next 12 months to 4.4%, compared with the 4.0% rise forecast nationally, and expect growth to remain above the historical norm (3.0%).

Business challenges

Global uncertainty linked to the Middle East conflict was a key driver of the dip in sentiment in the quarter. Newly added to the survey in Q2 2026, geopolitical risk was the main business concern and cited as a rising challenge by 64% of businesses in the region, comparable to the national average (65%). The rise in oil and gas prices and transport disruption caused by the closure of the Strait of Hormuz was also evident in BCM, with energy costs cited by 51% of businesses in the East of England as a growing challenge, up from last quarter, while transport problems were reported by 26% of businesses, the highest proportion across the UK, likely reflecting the impact on activity at Felixstowe and Harwich ports.

Rising costs and uncertainty driven by global events only added to existing domestic concerns in the region. Labour costs were cited as a rising challenge by 56% of businesses in the East of England. The proportion was down from last quarter but broadly comparable to the national average (58%). While fading from the highs recorded at the end of 2025, the tax burden was cited as a rising challenge by 43% of businesses in the region, still over twice the historical norm (19%), and concern about regulations (41%) remains above the historical norm (39%).

Labour market

Annual employment growth in the East of England was 1.6% in Q2 2026, exceeding the 1.4% rate recorded nationally and the regional norm (1.3%). Businesses plan to slow the rate of hiring slightly over the next 12 months, projecting jobs growth of 1.4%, compared with the 1.5% rise forecast nationally.

Annual wage growth in the East of England edged up to 3.2% in Q2 2026, slightly above the national rate (3.1%). Companies expect pay growth to slow to 2.9% over the next 12 months, compared with the 2.7% rise forecast nationally, but they anticipate salary growth will remain significantly above the region's historical norm (2.3%).

Input and selling prices, and profits growth

Annual input price inflation lifted to 3.9% in the East of England in Q2 2026, slightly under the UK average (4.1%). While businesses in the region expect cost inflation to ease over the coming year to 3.6%, the projection is above the historical norm (2.8%).

There was evidence from BCM that businesses in the East of England have passed some of the rise in their input costs on to customers, raising their selling prices by 2.7% in the year to Q2 2026. This was a sharp uplift from the previous quarter and significantly ahead of the region's historical norm (1.4%). Expecting cost pressures to soften, businesses plan to slightly ease the pace at which they raise their prices over the coming year to 2.4%.

Annual profits growth in the East of England stood at 2.3% in Q2 2026, lagging the 2.8% rate recorded nationally and down on the regional historical average (3.0%). Underpinned by optimism about stronger sales growth for the coming year, companies predict profits growth will rise to 4.8% next year, comparable to the 4.7% rise forecast nationally.

Capital investment and R&D

Businesses in the East of England appear to be increasingly cautious about investment, reporting softer annual capital investment growth in Q2 2026, at 1.6%, below both the 2.7% rate recorded nationally and the regional norm (2.0%). Businesses plan to scale back growth to just 0.2% next year, significantly lower than the 1.8% rise expected across the UK.

Companies reported stronger annual R&D budget growth in Q2 2026, at 2.5%, above the 2.0% rate recorded nationally. However, they intend to moderate budget growth over the next 12 months to 2.0%, marginally below the historical average (2.1%), but above the UK projection (1.8%).