Key takeaways

- The Memorandum of Understanding (MoU) signed by the US and Iran sets a potential pathway to the end of the conflict.

- Energy costs will lower, but it will take time.

- It may take even longer for supply chains to recover.

- Interest rates are likely to hold.

It will (eventually) lower energy costs

The potential end of the Iran conflict will reduce the risk premium on oil and gas. It will help lower wholesale prices, eventually leading to lower energy bills and fuel costs. This will ease the financial squeeze on households and businesses. However, domestic regulation, including Ofgem’s price cap, means that the pass-through is likely to be slow. Indeed, household energy bills will rise by an average of 13% in July as Ofgem’s price cap resets.

Prefer to listen?

This audio file was produced by AI and has been adapted from the original article for audio purposes.

Trade and supply chains may take a long time to recover

A peace deal would reduce the risk of further disruption to shipping within the Gulf region, including the Strait of Hormuz – an important route for global trade flows. However, major infrastructure damage, safety concerns and economic bottlenecks mean that a return to completely normal pre-war shipping operations in the Strait of Hormuz may not happen until next year. This will help keep that upward pressure on inflation and constrain economic activity.

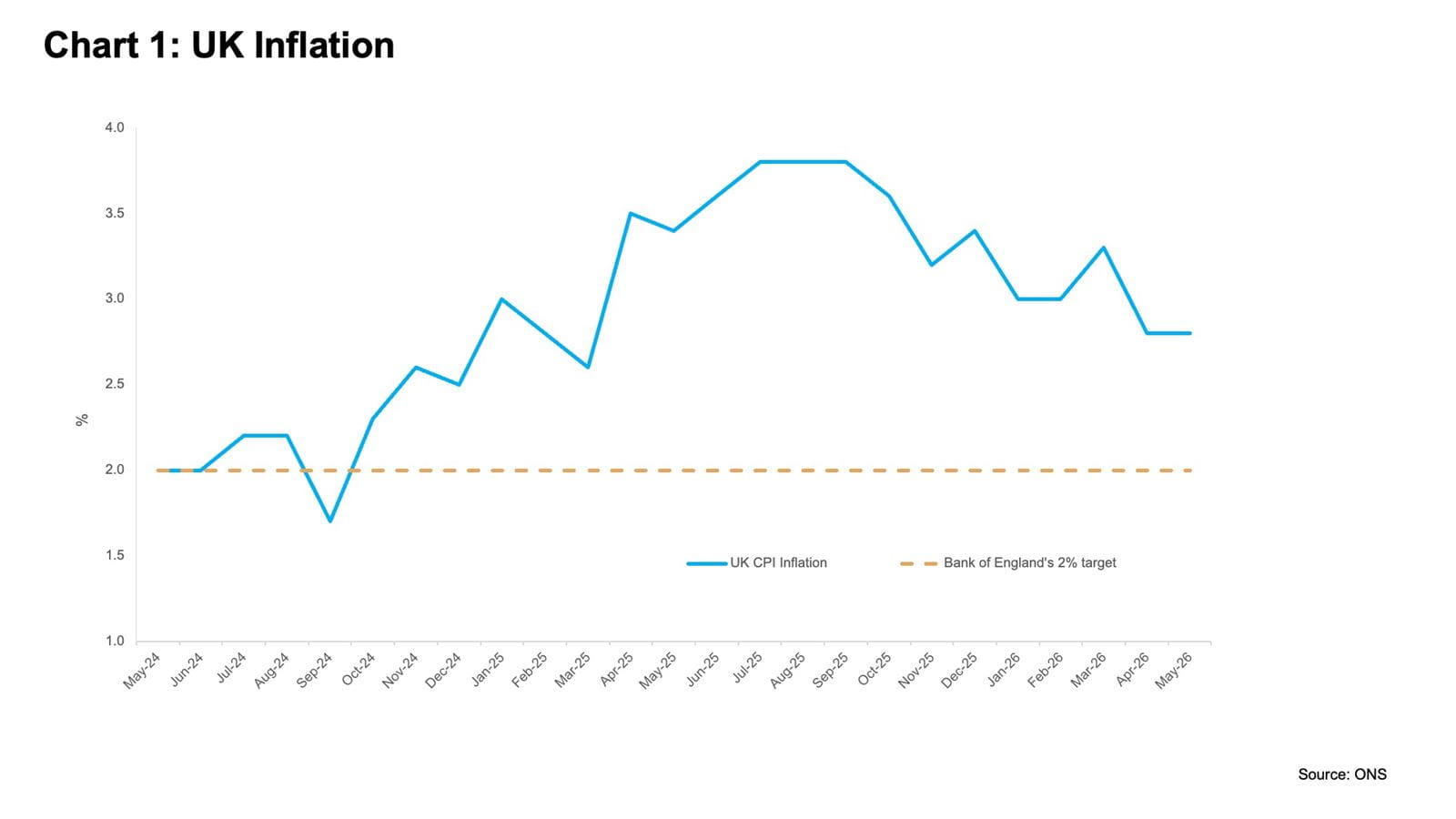

Inflation will likely peak below 4%

Official figures revealed that UK inflation was unchanged at 2.8% in May, still well above the Bank of England’s 2% target (see Chart 1). The largest upward pressure came from motor fuels, which rose by 24.6% in May. The biggest downward pressure came from food inflation, which fell from 3% in April to 2.2% in May, the slowest rate since December 2024.

Although the MoU arrived too late to stop higher energy bills and food costs triggering a summer inflation spike, if oil prices continue to weaken, then a peak well below 4% is becoming increasingly plausible. Energy and other supply chains are likely to take months to normalise, and meaningful easing in inflation will likely be delayed until late 2026.

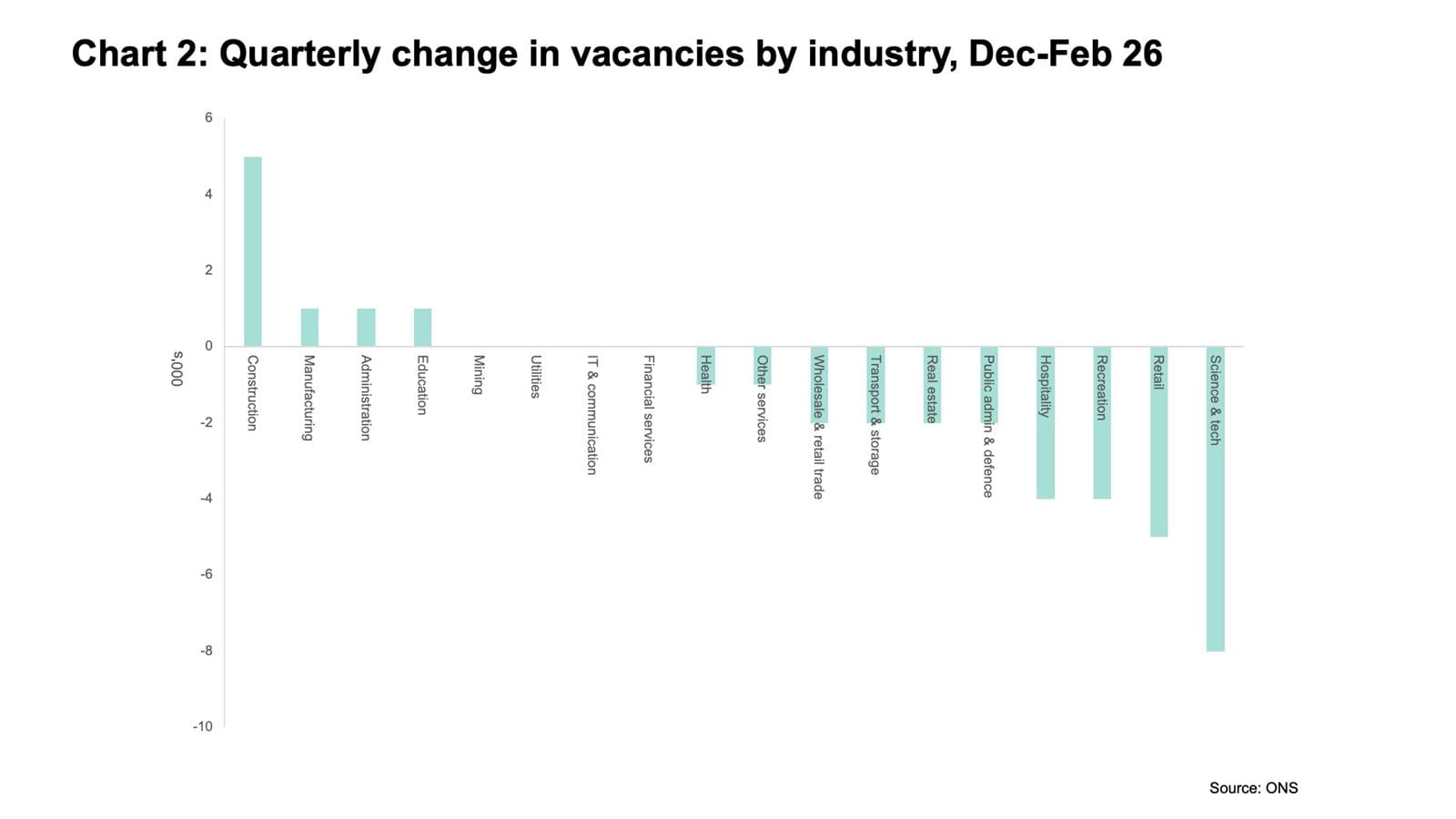

Job vacancies are falling

The UK’s unemployment rate dropped slightly from 5.0% to 4.9% in the three months to April 2026. The number of job vacancies fell by 19,000 in the three months to May 2026, the lowest level since February to April 2021. Vacancy estimates decreased in 10 of the 18 industry sectors (see Chart 2).

Professional, scientific and technical activities saw the largest decreases (down 8,000). These falling job vacancies suggest that the growing financial squeeze on firms and the use of greater automation is reshaping the jobs market.

Damage to the UK’s labour market is already done, with hiring intentions – already weakened by soaring staffing costs – likely to fade further as higher energy bills bite, lifting unemployment higher from here, particularly among younger workers.

Interest rates on hold for now

The Bank of England kept interest rates on hold at 3.75% for the fourth successive time. The Monetary Policy Committee (MPC) members voted 7-2 in favour of this outcome, with the two dissenters voting for a 25 basis points rise. The next UK interest rate decision will be announced at midday on Thursday 30th July.

The MPC is currently maintaining a cautious approach to setting policy as it waits for the dust to settle around US-Iran. While the US-Iran MoU has raised hopes that inflation could ease without further tightening, any return to hostilities could quickly tilt the balance back towards rate hikes. Currently, rate-setters are most likely to opt for a prolonged pause on interest rates. While the next move is now more likely to be an interest rate cut than a hike, it is unlikely to come before next year given the heightened global turbulence.

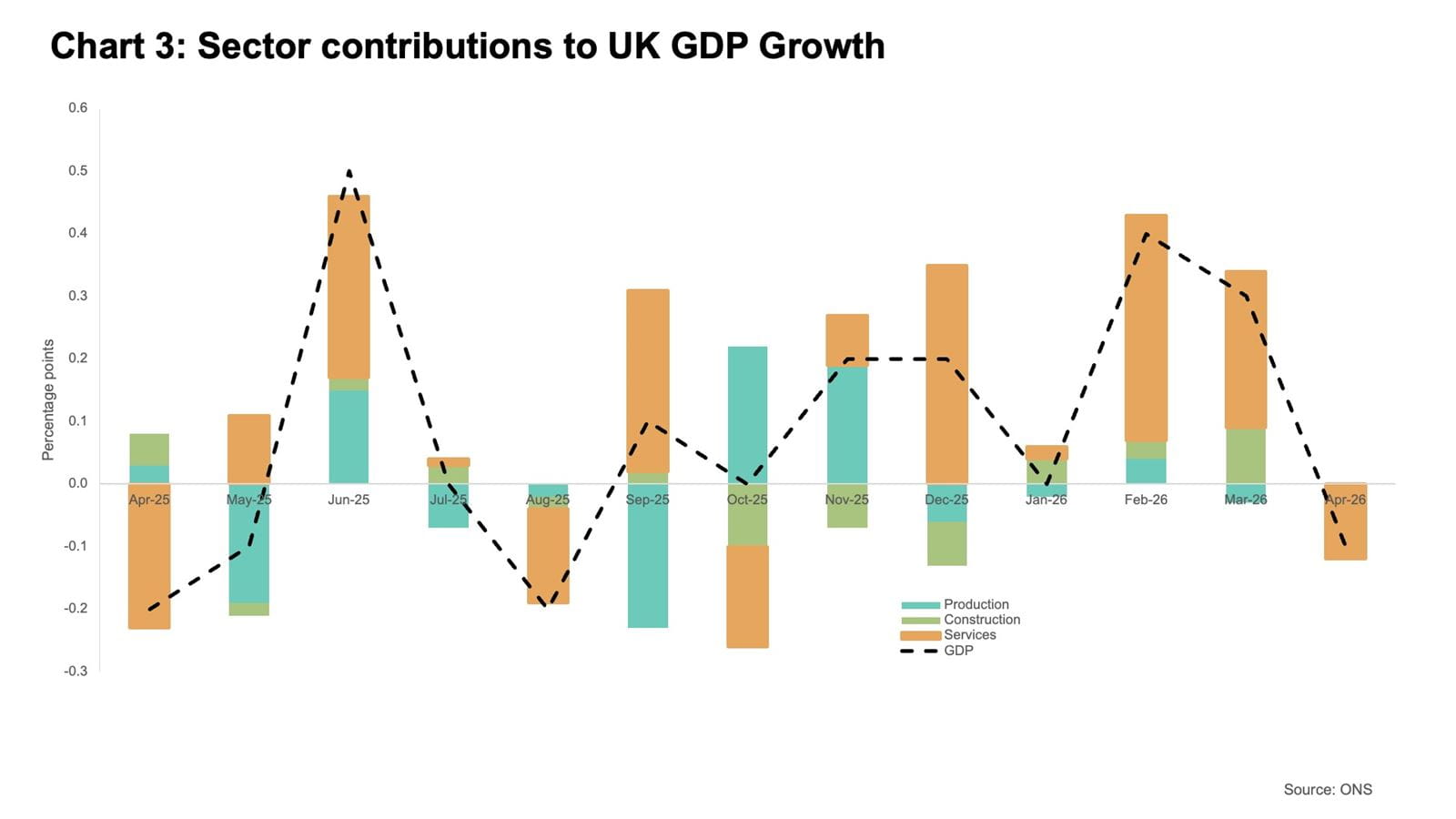

Overall impact on the UK's economic growth

Official figures revealed that UK GDP contracted by 0.1% in April 2026, the first monthly fall since August 2025 (see Chart 3). This fall was driven by a 0.2% fall in services, with arts and entertainment, sports activities and amusement and recreation activities particularly hard hit, thanks to the cancellation of multiple sporting events in the Middle East. This was partially offset by a 0.1% rise in construction, while industrial production showed no growth.

The US-Iran MoU is only likely to have a modestly positive impact on UK economic growth as it removes a major global energy and inflation risk. While this is crucial for avoiding recession, it won’t magically reverse the domestic slowdown already in motion. GDP growth is still likely to be notably lower this year due to the conflict. In other words, the peace deal helps stabilise the outlook by taking a headwind away, not adding a tailwind.

What to watch out for next month

- ICAEW's Business Confidence Monitor (BCM), one of the largest and most comprehensive quarterly surveys of UK business activity, will be covering the second quarter of 2026, launching on 2 July.

- The May 2025 UK GDP data, to be released on 16 July, could show that the UK economy returned to growth following April’s decline.

- The next set of inflation data, to be released on 22 July, should confirm that inflation resumed its upward trajectory in May, having held steady in April.

Further support

Resources

Economy

Expert analysis on the latest national and international economic issues and trends, and interviews with prominent voices across the finance industry alongside data on the state of economy.

Visit the hubResearch

UK Business Confidence

ICAEW's Business Confidence Monitor is one of the largest and most comprehensive quarterly surveys of business conditions and the health of the UK economy.

Read the latest findingsICAEW support

Training and events

Browse upcoming and on-demand ICAEW events and webinars looking at the global economy and trade.

Events and webinars A-Z of CPD Courses