Q2: The Middle East conflict adds to domestic pressures in the South East as confidence drops into deep negative territory.

The latest national Business Confidence Monitor (BCM) shows that the Iran War significantly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 13 April to 19 June 2026.

- Business confidence in the South East fell sharply to -21.1 from -7.1 in Q1, and notably below the UK average (-14.6).

- Below par annual domestic sales growth and slowing exports weighed on sentiment but companies anticipate performance for both measures will improve.

- Geopolitical tensions and higher energy costs compounded persistent domestic concerns about labour costs, taxation, regulation and customer demand.

- Salary inflation remains well above the historical norm but was weaker than the rate recorded nationally and businesses expect pay growth to be steady next year.

- Input price inflation rose as companies in the South East reported the lowest profits growth of any region.

- Companies intend to ease capital investment growth slightly while lifting R&D budgets marginally over the next 12 months.

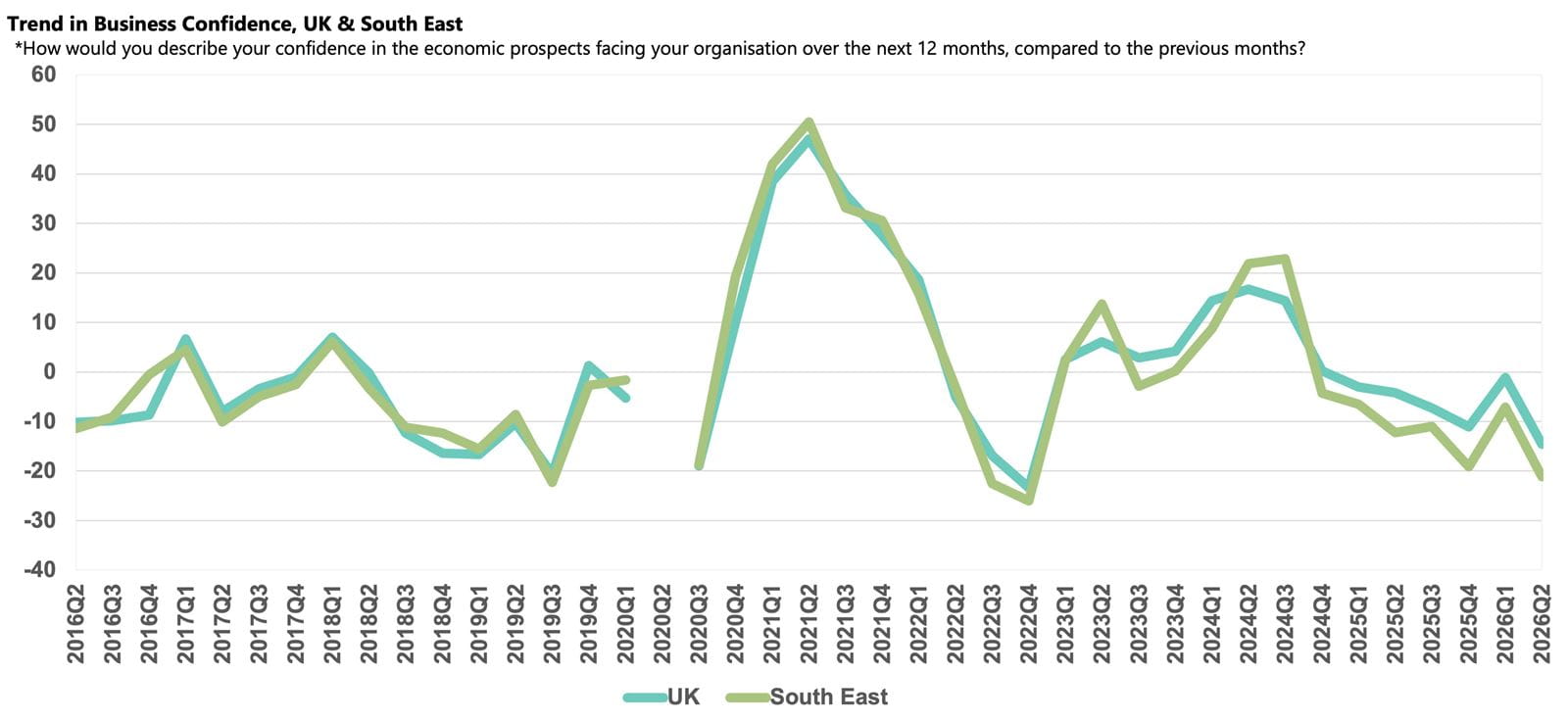

Business confidence in South East

Business sentiment in the South East fell sharply in Q2 2026, with the Business Confidence Index dropping from -7.1 in Q1 2026 to -21.1 and further from the region’s historical average (+4.3). Confidence in the South East remains well below the UK average (-14.6), having lagged behind the UK score since Q3 2024.

While recent geopolitical tensions and inflationary pressures have driven the latest fall in confidence, South East businesses also face persistent domestic pressures and are more likely to report labour costs, regulation, taxation and weaker customer demand as growing challenges than the national average. The anticipated improvement to underperforming sales growth over the coming year is likely contingent on developments in US–Iran relations, alongside political stability, as the UK awaits the appointment of its fifth Prime Minister in as many years.

Domestic sales and exports growth

Businesses in the South East reported improved annual domestic sales growth at 2.4% in Q2 2026, but the rate continued to lag the historical norm (3.2%) and was weaker than the rate recorded nationally (3.6%). Subdued sales performance in the region likely reflects the slower growth reported by the Construction and Property sectors this quarter. Companies are optimistic of stronger growth of 5.0% over the coming year, which compares favourably to the 4.7% rise forecast nationally.

The increase in global uncertainty and disruption since the outbreak of the war in Iran appears to have dented exports growth in the South East, as expansion eased to 2.3% in Q2 2026, and below the 3.1% rate recorded nationally. Nationally, the Business Services sector reported a slowdown in exports sales growth and, given the importance of this sector in the South East, likely weighed on regional performance. Businesses predict an acceleration to 4.5% over the next 12 months compared with the 4.0% rise forecast nationally. If this rate of expansion is achieved, it will lift exports growth above the region's historical norm (3.2%).

Business challenges

Global uncertainty linked to the Iran War was a key driver of the dip in sentiment in the South East this quarter. Newly added to the survey in Q2 2026, geopolitical risk was the main business concern and cited as a rising challenge by 67% of businesses in the region, slightly above the national average (65%). The rise in oil and gas prices caused by the closure of the Strait of Hormuz was also evident in BCM, with energy costs reported by 53% of businesses in the South East as a growing challenge, up from last quarter and close to the national average (55%).

Rising costs and uncertainty driven by global events only added to existing domestic concerns in the region, most of which were more widely cited in the South East than the national average. Labour costs were reported as a rising challenge by 62% of businesses in the South East. The proportion was up from last quarter and above the national average (58%). While fading from the highs recorded at the end of 2025, the tax burden was cited as a rising challenge by 49% of businesses in the region, compared to 45% in the UK. Concern about regulations also eased but, at 51%, remains above the historical norm (40%) and the UK average (47%). Customer demand (42%) has also faded as an issue in recent quarters but is still more widely reported in the region than historically (39%) and nationally this quarter (40%).

Labour market

Annual employment growth in the South East lifted to 1.5% in Q2 2026, broadly tracking the national rate (1.4%). Businesses plan to cautiously expand growth to 1.6% over the coming 12 months, comparable to the UK-wide projection (1.5%).

Businesses reported that salary inflation remains well above the historical norm (2.2%) but at 2.6%, annual wage growth in the South East was weaker than the rate recorded nationally (3.1%). Companies predict pay growth will be steady at 2.6% next year, close to the 2.7% rise forecast nationally.

Input and selling prices, and profits growth

South East businesses reported that annual input price inflation increased to 4.2% in Q2 2026, slightly above the UK average rise (4.1%). Companies expect input price growth to edge down to 3.9% over the next 12 months, similar to the UK-wide projection (3.8%) but markedly above the region's historical norm (2.7%).

With weak sales growth and ongoing concerns about customer demand, businesses appear cautious about passing on increased input costs to their customers, having maintained their annual selling price rises at 2.3% for each of the last four quarters. Businesses plan to slightly ease the pace at which they raise their prices over the coming year to 2.2%, still notably higher than the historical average (1.4%).

Businesses in the South East recorded the weakest annual profits growth of any UK region in Q2 2026, at 0.3%, notably down from the previous quarter and lagging the 2.8% rate recorded nationally. Nationally, the Construction and Business Services sectors reported disappointing profits growth and likely contributed to the underperformance in the South East. Companies predict a marked acceleration to 4.8% over the next 12 months, comparable to national expectations (4.7%) and above the regional norm (3.2%).

Capital investment and R&D

Annual capital investment growth in the South East was 2.0% in Q2 2026, edging above the regional norm (1.9%) but underperforming the 2.7% rate recorded nationally. Businesses plan to ease capital investment expansion to 1.7% over the next 12 months, similar to the UK-wide projection (1.8%).

Annual R&D budget growth in the South East was also steady at 1.9% in Q2 2026, matching the historical average and broadly in line with the 2.0% rate recorded nationally. Companies intend to lift growth to 2.1% over the coming year, slightly ahead of the UK forecast (1.9%).