Q2: Business confidence in Construction deteriorates amid rising costs and greater uncertainty.

The latest national Business Confidence Monitor (BCM) shows that the Iran War significantly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 13 April to 19 June 2026.

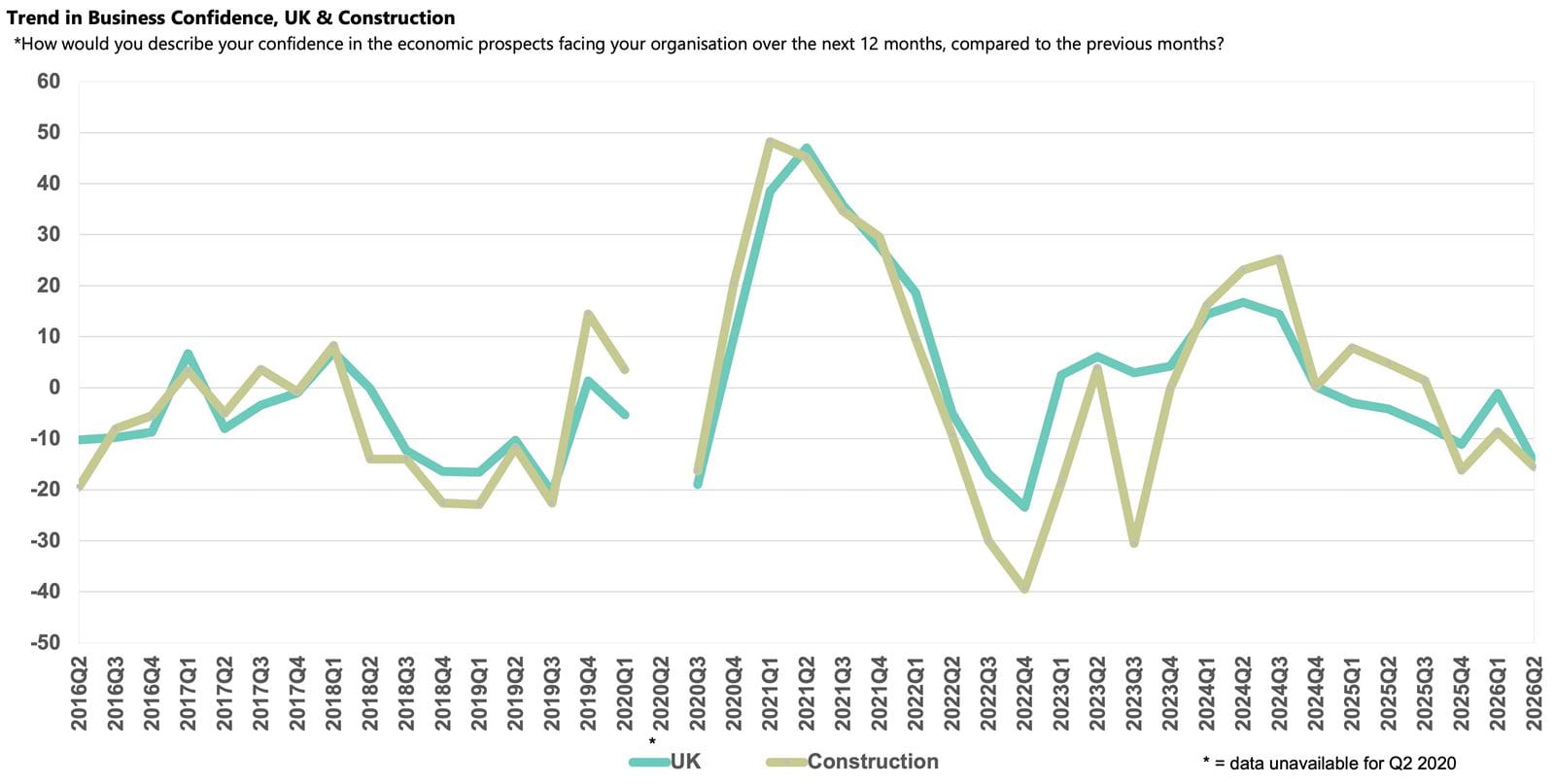

- Business confidence in Construction fell to -15.5 from -8.6 in Q1, dropping just below the UK average (-14.6).

- Domestic sales growth slowed, dipping below the historical norm but is expected to strengthen next year.

- Geopolitical risk and energy costs are the main growing challenges, followed by domestic issues including labour costs, taxation and regulations, and rising concern about late payments.

- Annual input price inflation rose sharply and companies plan to raise the rate of their price increases next year as profits declined in the year to Q2 2026.

- Companies plan to ease capital investment growth and cut R&D budgets over the next 12 months.

Business confidence in the Construction sector

Business sentiment among Construction companies declined in Q2 2026, with the Business Confidence Index falling from -8.6 in Q1 2026 to -15.5 with the score just below the UK average (-14.6). The latest decline marked the 4th consecutive quarter that the confidence index for Construction sat lower than the sector historical average (+3.2).

Amid heightened global and UK political uncertainty, confidence dipped further in the Construction sector in Q2 2026 as domestic sales growth continued to slow and input cost inflation leapt to the highest rate reported since the end of 2023. Businesses recorded a marginal fall in profits and almost 2 in 5 companies cited late payments as a growing challenge, while a quarter were concerned about access to capital. ONS data reported that construction output rose by 0.1% in April 2026 compared to the previous month, however growth was driven purely by repair and maintenance work with new work contracting over the period. The Bank of England Agents’ summary of business conditions for June 2026 noted that companies report that construction activity continues to fall modestly and while infrastructure contacts remain busy across large projects, contacts across other parts of the industry remain downbeat, particularly those involved in residential developments.

Domestic sales growth and customer demand

Businesses in the Construction sector reported that annual domestic sales continued to slow, easing to 2.5% in the year to Q2 2026, dropping below the sector norm (2.7%). Despite growing headwinds, companies remain optimistic that sales will improve over the coming year, projecting growth of 6.3%, compared with the 4.7% rise forecast nationally.

Customer demand was cited as a rising challenge by 39% of businesses in the Construction sector, down from 51% in Q1 2026. This proportion fell short of the sector's historical norm (42%) but was broadly in line with the national average (40%).

Input and selling prices, and profits growth

Annual input price inflation in the Construction sector spiked in Q2 2026, rising to 5.1% from 3.7% in the previous quarter and above the UK average (4.1%). Companies predict some moderation over the next 12 months to 4.6%, but this expectation is higher than the 3.8% rise forecast nationally, and above the sector's historical norm (3.2%).

Construction businesses passed on some of the rise in input costs to their customers, reporting stronger annual selling price growth in Q2 2026, at 2.1%, up from 1.8% in the previous quarter. But with sales remaining weak, companies appear to be absorbing more of the cost rises than in other sectors and are raising their prices more slowly than the UK average (2.5%). However, companies expect to raise their prices at a faster pace in the coming year, projecting 2.6%, compared with the 2.4% rise forecast nationally.

A combination of rising costs and slowing sales is eroding profit margins in the sector. Construction businesses recorded a fall in annual profits in Q2 2026, reporting a decline of 0.1%, lagging the 2.8% rate recorded nationally and the only sector to report a fall. Companies forecast a notable acceleration to 5.1% over the next 12 months, compared with the 4.7% rise forecast nationally, which if achieved will lift growth above the sector's historical norm (2.3%).

Employment and labour market challenges

Despite low levels of confidence, Construction businesses reported above-average jobs growth in the sector at 2.7% in Q2 2026, above the 1.4% rate recorded nationally. Companies plan a modest pick-up over the next 12 months, to 2.9%, above rise forecast nationally (1.5%), anticipating growth to continue above the sector's historical norm (1.2%). However, concern about the availability of non-management skills was reported by 32% of businesses in the sector — more widely cited than in any other UK sector and above the sector's historical norm (26%).

Salary inflation rose further above the sector’s historical average in Q2 2026. Businesses reported that annual pay increased for the fifth consecutive quarter, reaching 3.8% in Q2 2026, outpacing the UK average (3.1%). Companies predict wage growth will moderate over the next 12 months to 2.6%, compared with the 2.7% rise projected UK-wide, but anticipate it will remain above the historical norm (2.2%).

Business challenges

The Iran War and the prolonged closure of the Strait of Hormuz brought geopolitical risk and energy costs to the forefront of concerns for Construction businesses in Q2 2026. Nationally, global risk – a new challenge added this quarter – was cited by 65% of UK businesses, while energy costs were reported by 55%. Both issues were more prevalent in the sector and were each cited as a rising challenge by 73% of businesses. The more widespread concern among Construction businesses reflects their relatively high exposure to rising fuel and materials prices, and also the potential for higher interest rates and weaker demand if the conflict persists.

Amid rising wage bills, uplifts to the National Living Wage uplift and higher employer National Insurance Contributions, labour costs were cited as a rising challenge by 63% of Construction businesses, above the national average (58%). The tax burden remains a notable concern for the sector, reported as a rising challenge by 45% of businesses in the Construction sector, down from 66% in Q1 2026. This proportion was above the sector's historical norm (20%) but matched the national average. Regulatory challenges (41%), particularly related to planning delays, remain elevated and above the historical norm (37%).

There are also signs that businesses in the sector could be facing increased financial stress, as reports of late payments as a growing challenge rose further from the last quarter to reach 37%, the highest of any sector and above the historical norm (26%). At the same time a larger proportion of companies noted access to capital as a growing challenge, at 25%, the highest incidence across all sectors and above the sector norm (17%).

Investment growth

Investment was more encouraging with companies in the sector indicated annual capital investment growth at 3.6% in Q2 2026, above the 2.7% rate recorded nationally. Businesses plan to slow expansion to 3.0% over the next 12 months, but this anticipated increase is still notably above the 1.8% rise forecast nationally, and the sector's historical norm (1.6%).

Businesses also reported an uptick in annual R&D budget growth to 1.9% in Q2 2026, from 0.5% in the previous quarter, broadly in line with the UK average 2.0% and above the sector norm (1.1%). However, companies intend to scale back expenditure, planning to reduce R&D budgets by 0.2% next year, compared with expansion of 1.8% expected nationally.