Q2: Despite sentiment cooling slightly, the Energy, Water & Mining sector is still the most confident sector in the UK.

The latest national Business Confidence Monitor (BCM) shows that the Iran War significantly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker than expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 13 April to 19 June 2026.

- Business confidence in Energy, Water & Mining dipped to +10.5 from +12.9 in Q1, but was the only UK sector in positive territory and above the UK average (-14.6).

- Weak annual domestic sales growth is expected to recover over the coming year, while strong exports growth is predicted to slow.

- Geopolitical risk was the most widely cited rising challenge, followed by energy costs, with government support also prominent, but other common concerns were under reported.

- Annual pay growth eased but businesses intend to maintain above-average salary rises next year.

- Input price and selling price inflation spiked, and companies expect to continue to raise their prices at a sharper pace than all other sectors in the coming year.

- Businesses intend to reduce capital investment growth over the next 12 months, but their planned growth remains significantly above the projected national average.

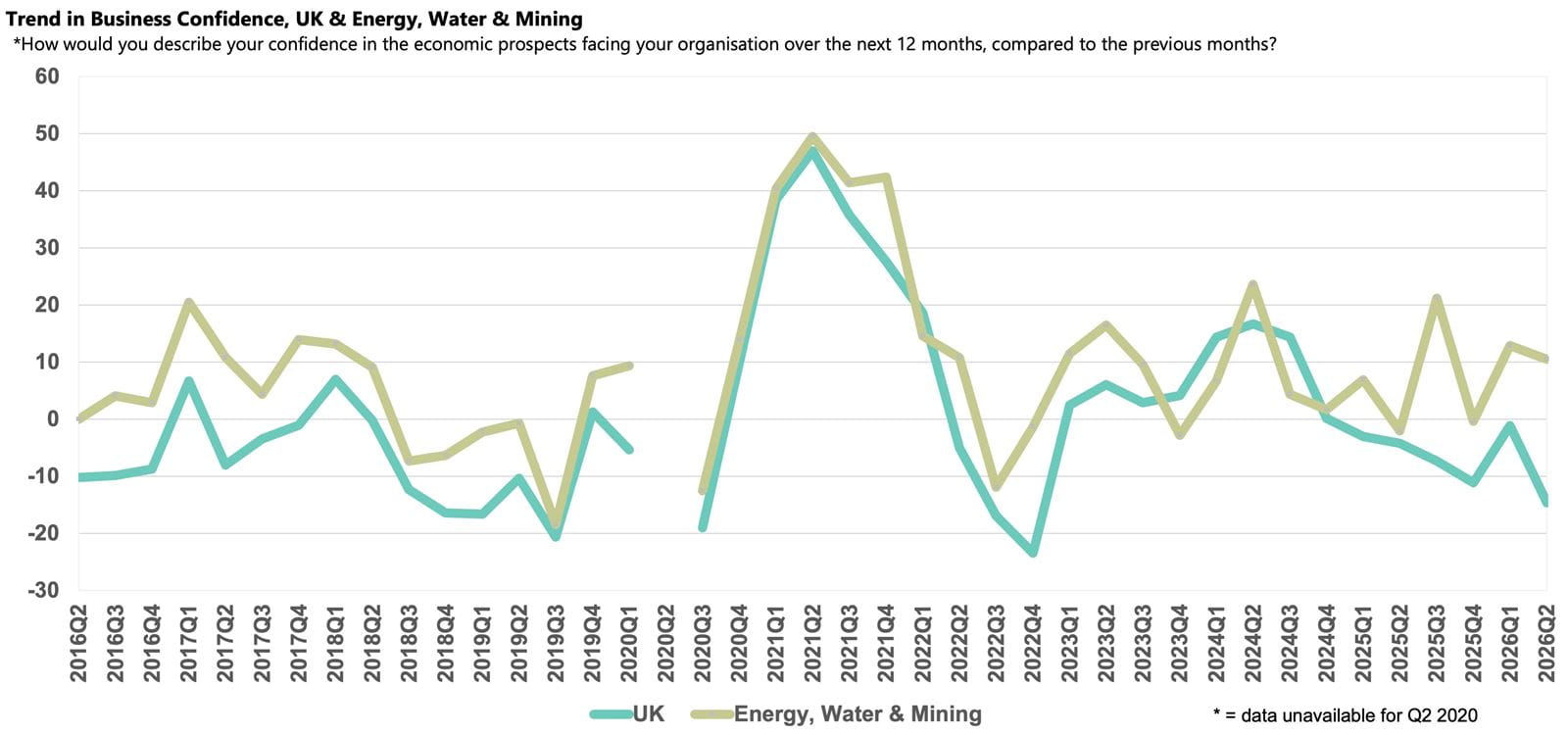

Business confidence in the Energy, Water & Mining sector

While business sentiment in Energy, Water & Mining declined slightly in Q2 2026, it was the most confident sector in the UK and the only one to record a positive score in the quarter. The Business Confidence Index for the sector dropped from +12.9 in Q1 2026 to +10.5 but remained above the sector's historical average (+7.8) and outperformed the UK average (-14.6), which sank further into negative territory.

The fall in confidence in the Energy, Water & Mining sector is undoubtedly linked to the disruption and energy price swings caused by the Iran war and the temporary closure of the Strait of Hormuz. However, the sector was somewhat less exposed than others, partly because exports grew sharply, and also because businesses have greater certainty over their selling prices, particularly after the government announced a 13% rise in the Ofgem energy price cap from July. Likely linked to increased international uncertainty and a rise in political instability domestically, a large proportion of businesses cited government support as a growing challenge. However, reflective of the greater optimism in the sector, concerns about some of the most common growing challenges among UK companies were less widespread in the sector than average.

Domestic and export sales growth

Businesses in the Energy, Water & Mining sector recorded muted annual domestic sales growth of 1.7% in Q2 2026, less than half the 3.6% increase observed across the UK. Companies in the sector expect growth to improve to 4.6% over the next 12 months, comparable to the 4.7% rise forecast nationally and markedly above the sector's historical norm (2.7%).

Exports growth was more encouraging in the year to Q2 2026, expanding by 6.7%, notably above the UK average (3.1%). With heightened uncertainty in the global trading environment, businesses expect export sales to moderate to 4.3% over the coming year, slightly above the UK projection of 4.0% and notably ahead of the sector's historical norm (2.9%).

Labour market

Annual employment growth in the Energy, Water & Mining sector slowed to 1.3% in Q2 2026, matching the sector’s historical norm and broadly in line with the UK average (1.4%). Businesses plan to increase their headcount at a faster pace over the coming year, with the projected increase of 2.4% set to exceed the 1.5% rise forecast nationally.

Annual wage growth in the sector slowed to 3.0% in Q2 2026, just below the 3.1% rate recorded nationally, but it remains above the sector’s historical norm (2.5%). While the national forecast is set to moderate slightly to 2.7% over the coming year, companies in the Energy, Water & Mining sector expect salary inflation will edge up to 3.1% over the next 12 months.

Selling and input prices, and profits growth

Like most other sectors, businesses reported a rise in input cost inflation this quarter, linked to the disruption in the Middle East. Annual input prices rose by 4.1% in Q2 2026, matching the 4.1% national rate. Companies are optimistic that it will moderate over the coming year, dropping below the sector’s historical norm (2.9%), to 2.7% y/y. This annual uplift is the lowest expected increase of any sector, well below the 3.8% projected UK-wide.

Companies in the Energy, Water & Mining sector increased their prices at the sharpest rate of any UK sector in the year to Q2 2026, with a 4.2% increase, double the sector’s historical norm (2.1%). With the 13% increase in the OFGEM energy price cap from July, companies in the sector expect to continue to raise their prices at a sharper pace than all other sectors in the economy, with the forecast rise of 3.6% significantly exceeding the national average projection (2.4%).

Strong exports sales growth, accompanied by the sharp uplift in selling prices, facilitated an uplift in annual profits growth for businesses in the Energy, Water & Mining sector in Q2 2026, to 3.0%. This uptick brought profits growth in line with the sector’s historical norm and marginally surpassed the national average increase of 2.8%. Companies expect a further pick-up over the coming year to 5.3%, and above the national average projection (4.7%).

Business challenges

With the outbreak of the Iran War and the prolonged closure of the Strait of Hormuz causing wholesale oil and gas prices to spike over the survey period, it is no surprise that geopolitical risk was cited as a rising challenge by 69% of businesses in the Energy, Water & Mining sector. Newly added to the survey this quarter (Q2 2026), this concern was more widely cited than the national average (65%). Energy costs themselves were cited as a rising challenge by 50% of businesses in the sector, with the issue less prevalent compared to the national average (55%).

Amid higher levels of global uncertainty and concerns about securing UK energy supplies, 28% of businesses reported government support as a growing challenge, over twice the historical average (13%), and more widely cited than in any other sector.

Meanwhile, Energy, Water & Mining companies were less likely than the UK average in Q2 2026 to cite the most common challenges for UK businesses such as labour costs (44%), regulatory requirements (39%), the tax burden (32%), customer demand (25%) and market competition (19%), reflecting stronger optimism in the sector.

Investment

The Energy, Water & Mining sector reported higher annual capital investment growth than almost any other sector in the year to Q2 2026, with a rise of 5.2%, and nearly double the UK average (2.7%). While companies expect to slow capital expenditure growth slightly to 4.5% over the coming year, the increase is stronger than projected by all other sectors and above the sectoral historical average (3.0%).

Annual R&D budget growth slowed for the third consecutive quarter in Q2 2026, easing to 0.8%, and lagged both the national average (2.0%) and the sector’s historical norm (1.8%). Businesses plan to curb R&D budget growth further over the next 12 months, with the anticipated increase of 0.4% less than a quarter of the 1.8% predicted nationally, with only businesses in Transport & Storage and Construction sectors reporting weaker forecasts.