Q2: Sentiment in London slides back into negative territory amid increased international uncertainty.

The latest national Business Confidence Monitor (BCM) shows that the Iran War markedly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 13 April to 19 June 2026.

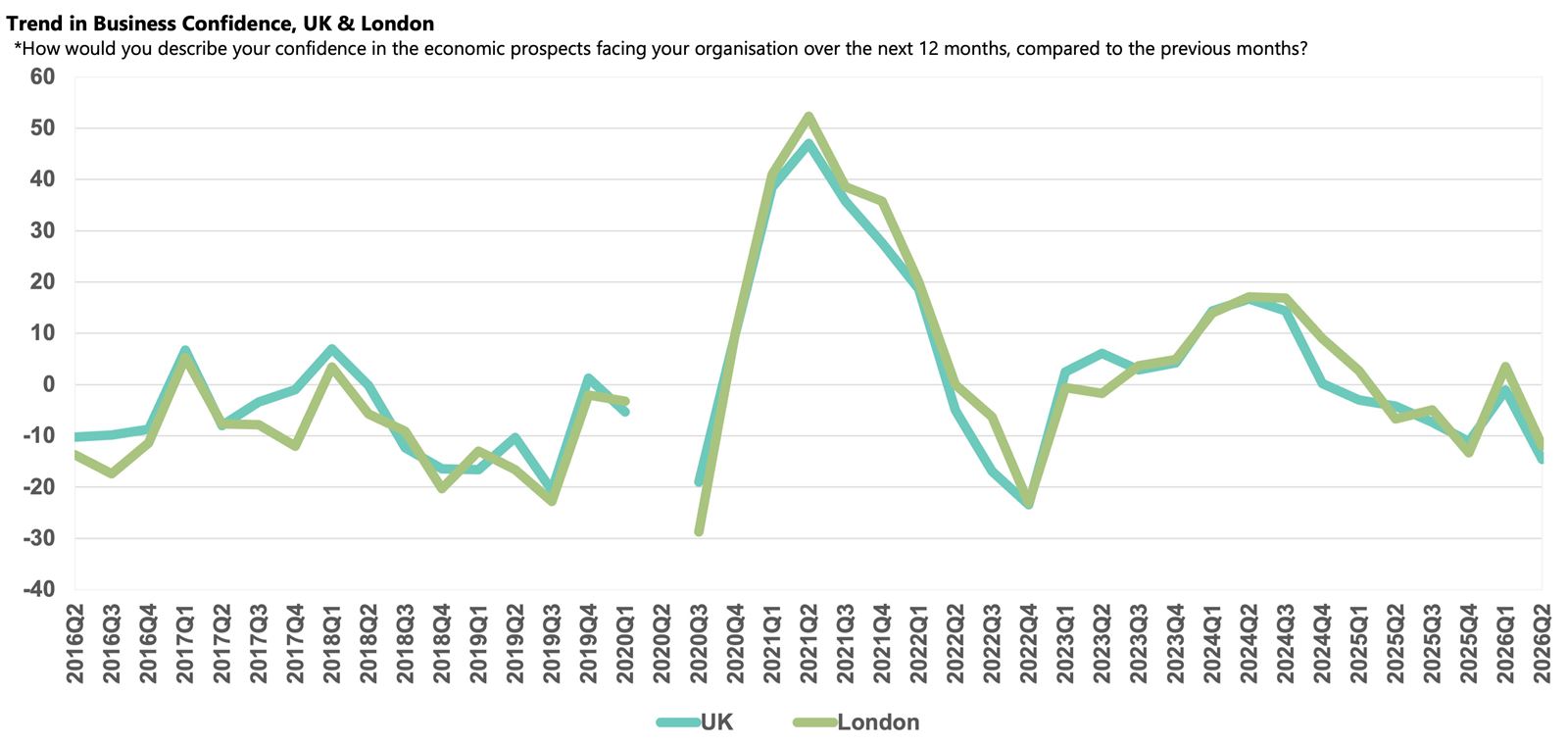

- Business confidence in London dropped into negative territory to -11.9 from +3.5 in Q1, but businesses continue to be more optimistic than the UK average (-14.6).

- Both annual domestic sales growth and exports growth remained above their respective historical norms and are expected to strengthen next year.

- Geopolitical risk — new this quarter — was the most widely cited rising challenge.

- Labour costs remain a prominent issue, with salary growth outpacing most of the UK and only a slight moderation expected next year.

- Annual input price inflation spiked and companies raised their selling prices in response.

- Companies are more cautious about investment and plan to pare back capital investment and R&D budget growth over the next 12 months.

Business confidence in London

Business sentiment fell sharply in London in Q2 2026, with the Business Confidence Index dropping from +3.5 in Q1 2026 to -11.9, markedly below the region’s historical norm (+5.2). Despite this decline, confidence in London remained above the UK average (-14.6).

Like the rest of the UK, the Iran War and the closure of the Strait of Hormuz fostered widespread uncertainty and significantly undermined confidence among London’s businesses. And like many other parts of the UK, with energy costs rising, businesses reported that their input costs rose in the quarter, but London’s largely service-based economy was somewhat insulated from the full impact, and business reported healthy annual sales growth in the quarter, while anticipating further expansion in the year ahead. However, significant downside risks persist. In particular, developments in US–Iran relations will be key to whether these expectations are realised. Political uncertainty could also play a part as the UK awaits the appointment of its fifth Prime Minister in as many years.

Domestic sales and exports growth

Businesses in London reported that annual domestic sales growth reached a three-year high in Q2 2026, at 4.5%, outpacing the UK average (3.6%) and the historical norm (3.0%). Much of this strength is likely linked to the marked uplifts reported by the abundant IT & Communication (5.3%) and Banking, Finance & Insurance companies (6.1%) in the region. Looking ahead, businesses in the capital expect further improvements over the next 12 months, with a projected rise of 5.1%, which is among the strongest forecasts in the UK, and above the UK projection (4.7%).

Annual exports growth in London moderated in Q2 2026, to 3.9%, though this increase was still ahead of both the 3.1% rate recorded nationally and the capital’s historical norm (3.5%). Businesses expect growth will continue at a similar rate over the coming year, with the predicted uplift of 4.0% in line with the national average forecast.

Business challenges

The Iran War and the prolonged closure of the Strait of Hormuz put geopolitical risk – a new challenge added this quarter – to the forefront of concerns for businesses in London in Q2 2026. The issue was cited as a rising challenge by 68% of businesses in the region and was more prevalent among London companies than the national average (65%). With the disruption to shipping, concerns about transport problems (19%) rose above their historical norm (13%) and the associated spike in oil and gas prices led 50% of businesses in London to report energy costs as a rising challenge. This proportion was below the national average (55%), reflecting London’s lower exposure to heavy energy-consuming sectors such as Manufacturing & Engineering.

Rising wage bills are another prominent concern, with the consecutive uplifts in the National Living Wage alongside increased employer National Insurance Contributions key contributors. As a result, labour costs were cited as a rising challenge by 55% of businesses in the region, only marginally below the national average (58%).

The Renters’ Reform Act and Employment Rights Act have each brought additional responsibilities for landlords and employers, and regulatory requirements were cited as a rising challenge by 47% of businesses in London, above the region's historical norm (44%) and in line with the national average (47%).

There was also some indication from BCM that some businesses in London may be exposed to greater financial stress, with reports of late payments gradually rising over recent quarters. In Q2 2026, 24% of businesses cited the issue which is above the regional survey average (20%).

Labour market

Annual employment growth in London improved to 1.6% in Q2 2026, matching the region’s historical average, and outperforming the 1.4% rate recorded nationally. Businesses remain cautious about recruitment but plan a modest pick-up to 1.8% over the next 12 months, above the UK average projection (1.5%).

Businesses reported that they increased salaries by 3.4% in the year to Q2 2026, higher than the national average increase (3.1%) and the second highest rate in the UK. Companies expect pay growth to moderate to 2.9% over the year ahead, exceeding both the national projection (2.7%) and the region’s historical norm (2.1%).

Despite some evidence of strengthening labour demand and ongoing pay pressures in the region, concerns about the availability of skills remain below their norms.

Input prices, selling prices and profits growth

London businesses reported that annual input price inflation increased to 4.1% in Q2 2026, matching the UK average rise. Companies expect input price growth to slow to 3.2% over the next 12 months, notably lower than the 3.8% rise forecast nationally, but still markedly above the region's historical norm (2.5%).

There was evidence from BCM that businesses in London have passed some of the rise in their input costs on to customers, raising their selling prices by 2.4% in the year to Q2 2026. This was a marked uplift from the previous quarter and far ahead of the region's historical norm (1.3%). Expecting cost pressures to soften, businesses plan to slightly ease the pace at which they raise their prices over the coming year to 2.2%.

Annual profits growth in London was unchanged from the previous quarter in Q2 2026 at 4.4%, with companies in the capital markedly outperforming the 2.8% rate recorded across the UK. Businesses predict a notable acceleration over the next 12 months to 4.8% and further above the historical norm (3.4%).

Capital investment and R&D

Annual capital investment growth in London eased slightly from the previous quarter in Q2 2026, to 2.6%, a broadly similar rate to the UK (2.7%). However, with heightened uncertainty and elevated borrowing costs, businesses remain cautious about investment decisions and are planning to slow growth to 2.2% over the next 12 months. This moderation will bring growth in line with the region’s historical norm but the rate is higher than the national projection (1.8%).

Businesses in London reported a pick-up in annual R&D budget growth to 2.6% in Q2 2026, exceeding the UK average (2.0%). Companies intend to slow R&D expansion over the next 12 months to 2.2%, higher than forecast nationally and the region’s historical norm (both 1.8%).