Q2: Sentiment in the North West slides into deep negative territory.

The latest national Business Confidence Monitor (BCM) shows that the Iran War significantly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 13 April to 19 June 2026.

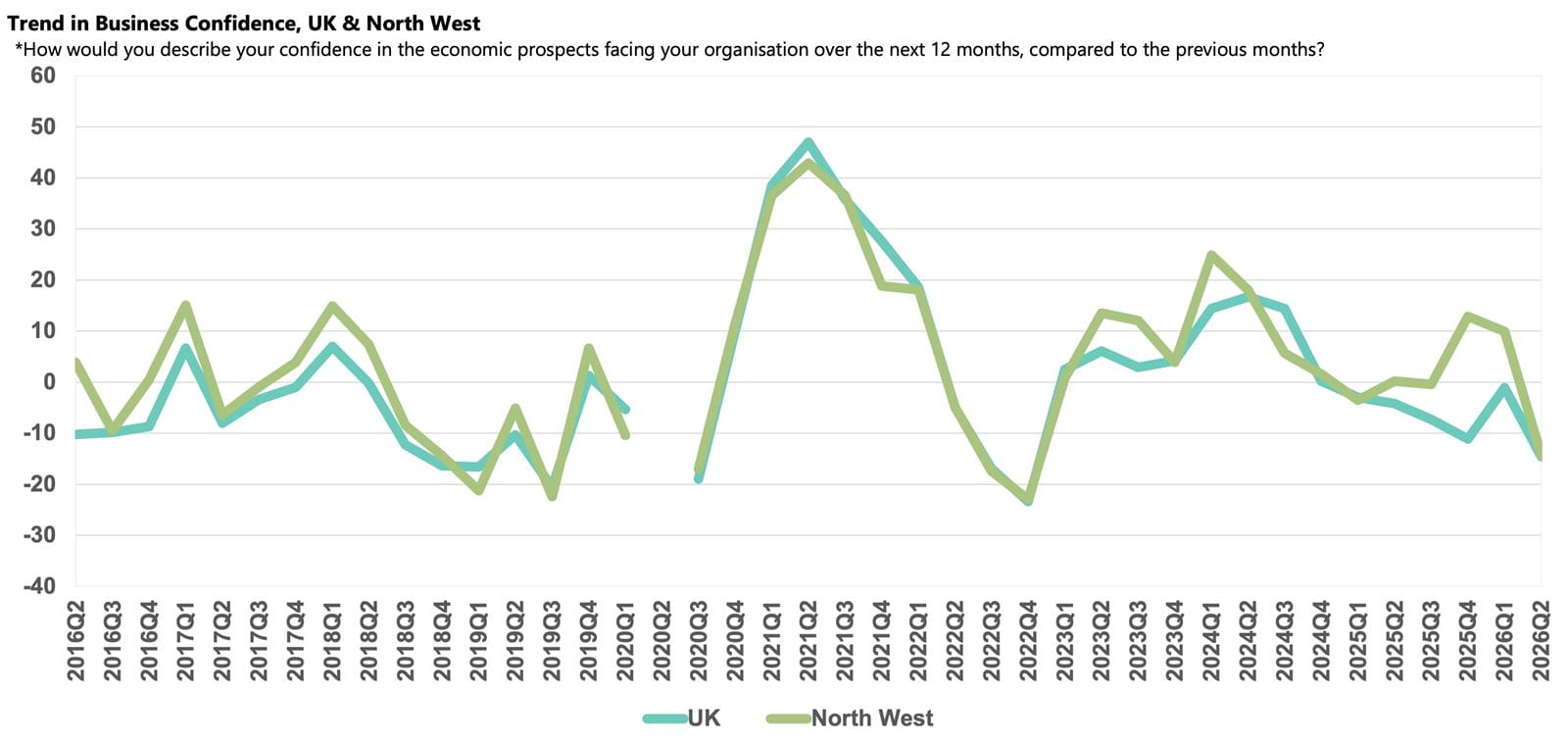

- Business confidence in the North West fell to -14.3 from +9.9 in Q1, broadly in line with the UK average (-14.6).

- Annual domestic sales growth was above the norm, but exports growth slowed sharply, though businesses are optimistic that both will improve next year.

- Geopolitical risk was the most widely cited rising challenge, closely followed by labour costs, while reports of the regulatory burden surpassed all other regions.

- Salary growth rose further above the historical norm and businesses expect the higher rate to be maintained.

- Similarly, businesses predict input price inflation will be sticky and fail to ease over the coming year.

- R&D budget growth is set to remain weak, and companies also plan to scale back their recent robust rate of capital investment growth.

Business confidence in North West

Business sentiment in the North West fell sharply in Q2 2026, with the Business Confidence Index dropping from +9.9 in Q1 2026 to -14.3, and while the score was broadly in line with the UK average (-14.6), it sat significantly below the regional historical average (+5.6).

Similar to many regions, the outbreak of the Iran War towards the end of the first quarter dominated business concerns in the North West in Q2 2026. The closure of the Strait of Hormuz drove a sharp rise in energy and oil prices and created supply-chain disruption which appears to have already dented exports growth in the region and driven up input costs and selling prices, with companies expecting these pressures to remain over the coming year. Local and national political developments increased business uncertainty, with the early-May elections leading to a by-election victory for Andy Burnham, a subsequent Manchester mayoral contest, and the resignation of Prime Minister Keir Starmer.

Domestic sales and exports growth

Businesses in the North West reported annual domestic sales growth of 3.6% in Q2 2026, matching the national growth rate and moving back above the region’s historical norm. Companies anticipate a notable uplift over the next 12 months to 4.9%, just above the UK forecast rate of 4.7%.

Increased global uncertainty dampened demand across external markets over the survey period as energy costs soared and the price of transporting goods surged. Companies in the North West appear to have been particularly impacted as they recorded the weakest annual exports growth of any UK region in Q2 2026, at 1.3%, markedly lagging both the region’s historical norm (2.6%) and the UK average (3.1%). Businesses expect conditions to improve over the next 12 months, with an anticipated increase of 3.9% which is broadly in line with the 4.0% rise forecast nationally.

Business challenges

With the Iran War ongoing through much of the survey period, geopolitical risk was cited as a rising challenge by 65% of businesses in the region. Newly added to the survey this quarter (Q2 2026), this concern was reported as widely as the UK average (65%), while energy costs were report by half (50%) of businesses, up from last quarter but below the UK average (55%).

The increases in National Living Wage over recent years alongside the uplift in employers’ National Insurance Contributions have significantly added to wage bills across the region. In Q2 2026, labour costs were cited as a rising challenge by 61% of businesses in the North West, marginally above the national average (58%). Concerns about the tax burden have eased but were noted by 50% of businesses, a higher incidence than UK-wide (45%).

The implementation of the Employment Rights Act and the Renters' Reform Bill continue to drive concern as companies adjust to the new requirements. The proportion of businesses citing regulations as a rising challenge increased to 53% in Q2 2026. This was the highest rate since Q1 2020, and the issue was more widely reported than in any other UK region. Meanwhile, reports of late payments have been steadily rising in recent periods and they edged above the historical norm (21%) to 24% this quarter.

Labour market

Annual employment growth in the North West increased by 1.8% in Q2 2026, running ahead of the 1.4% rate recorded nationally. Businesses anticipate growth to slow to 1.5% over the next 12 months, in line with the national average but still ahead of the historical norm (1.3%).

Amid significant concern about labour costs, companies in the region reported that annual salary growth increased to 2.9% in Q2 2026, widening the gap to the historical average (2.2%). Businesses predict wage growth will remain at 2.9% over the coming year, above the 2.7% rise forecast nationally.

Input and selling prices, and profits growth

The spike in oil and gas prices following the closure of the Strait of Hormuz caused annual input price inflation in the North West to rise to 4.0% in Q2 2026, broadly mirroring the 4.1% national uplift. Companies expect growth to continue at a similar pace over the next 12 months, with a projected increase of 3.9%, again similar the 3.8% rise forecast nationally, but still markedly above the region's historical norm (2.7%).

Despite rising input inflation, businesses held selling price inflation steady at 2.5% in Q2 2026, broadly unchanged from 2.6% last quarter, and matching the rate recorded nationally. Companies intend to maintain a similar rate of price growth over the next 12 months, expecting a 2.4% rise, which is consistent with the UK-wide projection.

Businesses in the North West reported an uplift in annual profits growth to 2.3% in Q2 2026, though this was lower than the 2.8% rate recorded nationally. Companies in the region anticipate a marked acceleration, projecting profits to rise by 4.8% over the next 12 months, marginally exceeding the 4.7% rise forecast nationally and climbing above the region's historical norm (2.9%) if achieved.

Capital investment and R&D

Companies reported robust annual capital investment growth of 4.1% in Q2 2026, far exceeding both the 2.7% rate recorded nationally and the region’s historical norm (2.2%). However, this strong rate of expansion is not expected to be sustained, and businesses plan a notable moderation to 2.3% over the coming year, yet this projection still exceeds the UK forecast (1.8%).

Businesses in the North West reported softer annual R&D budget growth in Q2 2026, at 0.9%, less than half the 2.0% rate recorded nationally and the region’s historical norm (1.9%). Companies plan to maintain growth at this pace over the next 12 months, with the region set to underperform the national projection of 1.8%.