Q2: Sentiment in the North East slides back into negative territory.

The latest national Business Confidence Monitor (BCM) shows that the Iran War significantly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 13 April to 19 June 2026.

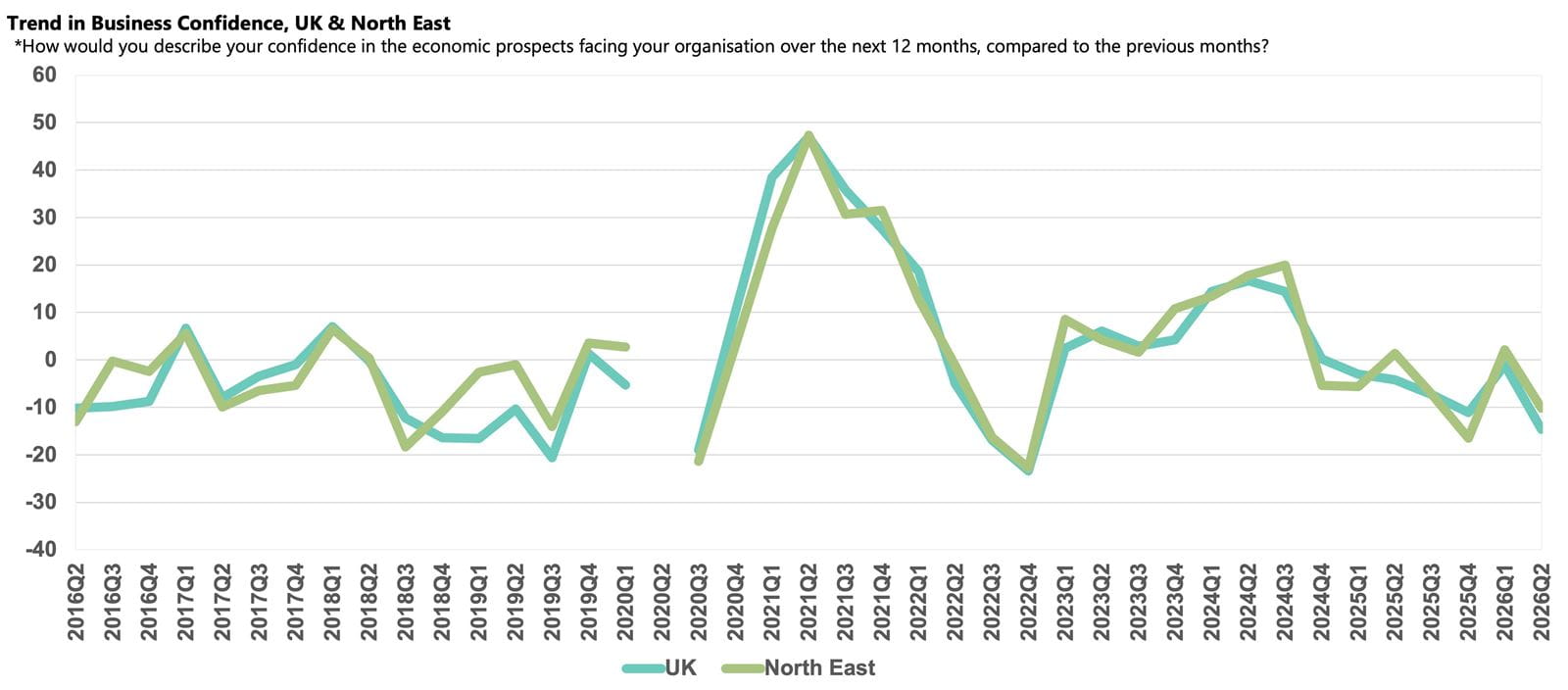

- Business confidence in the North East fell from +2.1 in Q1 2026 to -10.2, but remained above the UK average (-14.6).

- Companies reported strong annual domestic sales growth and are upbeat about prospects for the coming year, however exports growth is set to weaken.

- Labour costs were the most widely cited rising challenge, followed by the tax burden.

- Annual salary growth eased slightly from the previous quarter but remains above the region's historical norm.

- Input price inflation spiked, with the region reporting the sharpest increase in the UK.

- Companies plan to slow capital investment growth but lift R&D budgets at a sharper pace over the next 12 months.

Business confidence in North East

Business sentiment in the North East fell sharply in Q2 2026, with the Business Confidence Index dropping from +2.1 in Q1 2026 to -10.2. Despite this decline, the North East was one of the most confident regions in the UK, remaining above the UK average (-14.6). However, businesses in the region have been downbeat for an extended period, with this latest reading marking the seventh consecutive quarter that its confidence score sat below the regional historical average (+5.7).

While confidence was likely buoyed by above-average annual domestic sales growth, rising cost pressures appear to be a more significant challenge for businesses in the region than elsewhere. Businesses reported the highest rates of input price inflation in the year to Q2 2026, with labour costs the most widespread growing challenge, followed by the tax burden and energy costs.

Domestic sales and exports growth

Businesses in the North East reported stronger domestic sales growth in the year to Q2 2026, with expansion improving further ahead of the region's historical norm (3.1%), and companies forecast that growth will remain buoyant over the coming year.

In contrast, businesses in the North East reported softer annual exports growth in Q2 2026, at 2.2%, below the 3.1% rate recorded nationally and the region's historical norm (2.5%) and companies expect exports growth to slow over the coming 12 months.

Business challenges

The North East’s larger dependence on typically lower paid roles has left it more exposed to the impacts of rising wage bills, following the successive uplifts in the National Living Wage alongside higher employer National Insurance Contributions. As a result, labour costs were cited as a rising challenge by 70% of businesses in the region, and more widely reported than elsewhere in the UK.

Alongside employment costs, there was other evidence in BCM of growing company concerns about the costs of doing business in the region. The tax burden (61%) was more widely cited as a rising challenge in the North East than elsewhere, and reports of energy costs (53%), were up from the previous quarter, as the impacts of the closure of the Strait of Hormuz were felt by businesses across the region. Geopolitical risks themselves were reported by over half of companies (51%). The incidence of businesses reporting late payments has also been rising across recent quarters, reaching 24% in Q2 2026, and above the historical norm (22%).

At the same time, businesses are still adjusting to the Employment Rights Act and Renter’s Reform Act which have altered previously standard operating practices across the UK, and 51% of businesses cited regulatory requirements as a rising challenge in Q2 2026, significantly above the regional historical norm (39%).

Labour market

Annual employment growth in the North East was 1.2% in Q2 2026, marginally below both the national increase (1.4%) and the region’s historical norm (1.3%). Businesses plan a pick-up over the next 12 months, projecting 2.0% growth, exceeding the 1.5% rise forecast nationally.

Annual wage growth in the North East was 3.0% in Q2 2026, broadly in line with the 3.1% rate recorded nationally. Companies predict wage growth to moderate further over the next 12 months to 2.4%, just below the 2.7% rise forecast nationally, but still ahead of the region's historical norm (2.2%).

Softer labour demand is reflected in the proportion of companies reporting labour market related concerns as growing challenges in Q2 2026. Citations for both the availability of management (8%) and non-management (7%) skills sat significantly below their historical norms in Q2 2026, of 14% and 21% respectively.

Input and selling prices, and profits growth

Businesses in the North East reported the sharpest input price inflation of any UK region in the year Q2 2026, at 5.0%. This was the largest uptick in input costs since Q4 2023 and is notably higher than the 4.1% rate recorded nationally. Companies expect input cost inflation to ease slightly over the next 12 months, though the 4.1% predicted increase is higher than the UK average forecast (3.8%) and the region's historical norm (2.8%).

Companies in the region are not absorbing all the increase in their costs and passing some of it on to customers. They reported that they raised their selling prices by 2.9% in the year to Q2 2026, running ahead of the UK average (2.5%). Businesses intend to maintain similar rates of price inflation over the next 12 months, with a planned increase of 2.8%, far above the region's historical norm (1.7%).

Businesses in the North East recorded strong annual profits growth in Q2 2026. The reported increase of 6.6% was above the region's historical norm (2.9%) and the UK average (2.8%). Companies in the region predict their profits performance will continue to outperform the UK average, reaching 6.9% and above the national average projection of 4.7%.

Capital investment and R&D

Companies in the North East recorded robust annual capital investment growth of 5.1% in Q2 2026, but this rate of growth is not expected to be sustained. Businesses plan to moderate growth to 2.8% over the coming year, which is still above the regional norm (2.3%) and the 1.8% rise anticipated across the UK as a whole.

Businesses in the North East reported softer annual R&D budget growth in Q2 2026, at 1.5%, below the UK average increase of 2.0%. Companies forecast a marked acceleration over the next 12 months, with the anticipated increase of 3.0%, above both the national average forecast and the region’s historical norm (both 1.8%).