Q2: Yorkshire & Humber is the most confident region in the UK in Q2 2026.

The latest national Business Confidence Monitor (BCM) shows that the Iran War significantly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 13 April to 19 June 2026.

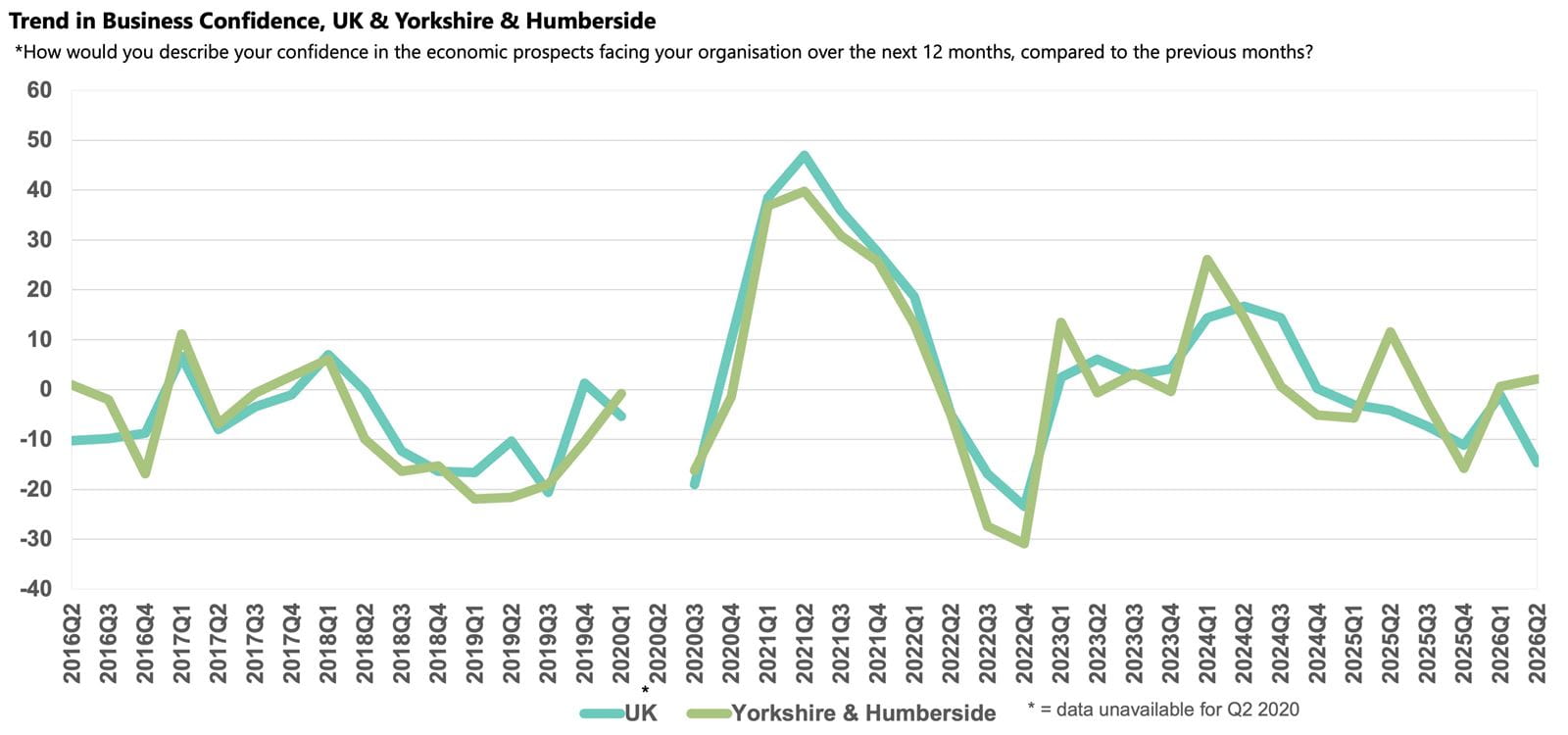

- Business confidence in Yorkshire & Humber rose to +2.1 from +0.6 in Q1, the strongest reading of any UK region and above the UK average (-14.6).

- Annual domestic sales and exports growth were both above their respective historical norms in the year to Q2 2026, and both are forecast to strengthen further.

- Geopolitical risk was the most widely cited rising challenge, alongside labour costs and energy costs.

- Annual pay growth is forecast to ease next year but remain above the historical norm.

- Input price inflation spiked and is expected to rise at the same pace next year, with companies planning to raise their selling prices in response.

- Businesses plan to scale back both capital investment and R&D budget growth over the next 12 months.

Business confidence in Yorkshire & Humberside

Yorkshire & Humber was the only region to report an uplift in confidence in Q2 2026, with the Business Confidence Index rising from +0.6 in Q1 2026 to +2.1. The region was also the most confident in the UK, remaining above the UK average (-14.6), but was again below its regional historical average (+4.6).

While businesses in most other regions have seen their confidence deeply affected by the outbreak of the Iran war, companies in Yorkshire remain comparatively optimistic. They project marked increases in both domestic sales and exports growth over the coming year, and as a result their profits growth outlook remains strong. However, significant downside risks persist. In particular, developments in US–Iran relations will be key to whether these expectations are realised, alongside growing political uncertainty, as the UK awaits the appointment of its fifth Prime Minister in as many years.

Domestic sales and exports growth

Annual domestic sales growth slowed to 3.7% in Q2 2026 and, while broadly in line with the national average (3.6%), remained above the historical norm (2.9%). Companies in the region remain optimistic about the coming year, anticipating a marked uplift to 5.8%, above the 4.7% rise forecast nationally.

The rise in global uncertainty dampened demand across external markets over the survey period as energy costs spiked and the cost of transporting goods soared. Consequently, annual exports growth in Yorkshire & Humber moderated to 3.0% in Q2 2026, close to the UK average (3.1%). Despite the slowdown, businesses in the region are the most optimistic about exports growth prospects in the UK, with the anticipated increase of 5.7% far exceeding both the region’s historical norm (2.7%) and the national average projection (4.0%).

Business challenges

As in most other regions, with the Iran War and the closure of the Strait of Hormuz ongoing through much of the survey period, geopolitical risk – a new challenge added this quarter – was at the forefront of concerns for Yorkshire & Humber businesses in Q2 2026. Of the companies surveyed in the region, 66% reported the issue as a rising challenge and comparable to the national average (65%). The impact of the associated spike in oil and gas prices was evident in BCM, with energy costs cited by 66% of businesses as a rising challenge, far surpassing the national average (55%).

Rising wage bills, the National Living Wage uplift and higher employer National Insurance Contributions have all caused employment costs to rise in recent months. Yorkshire & Humber’s sectoral composition and greater reliance on lower-paid roles means it is more exposed to the impacts of these increases compared to some other regions. This trend is reflected in the fact that labour costs were also cited as a rising challenge by 66% of companies in the region, notably above the national average (58%).

Concerns about the tax burden, while fading, remain significant at 51%, while regulatory requirements (43%) remain above the historical norm. Reports about late payments were more prevalent among companies in Yorkshire & Humber than in any other region.

Labour market

Annual employment growth in the region slowed to 0.7% in the year to Q2 2026, half the 1.4% rate recorded nationally. Businesses foresee a modest pick-up over the next 12 months, though the projected increase of 0.9% is among the weakest anticipated uplifts of any UK region, lagging both the region’s historical norm of 1.0% and the 1.5% rise forecast nationally.

Annual wages growth in Yorkshire & Humber was 3.1% in Q2 2026, matching the national average. Companies predict wage growth will soften over the next 12 months to 2.8%, comparable to the 2.7% rise forecast nationally, and above the region's historical norm (2.3%). Concern about the availability of non-management skills was reported by a quarter of businesses in the region — more widely cited than in any other UK region and above the region's historical norm (19%).

Input and selling prices, and profits growth

The closure of the Strait of Hormuz caused oil and gas prices to spike over the survey period, with businesses in Yorkshire & Humber reporting that annual input price inflation increased to 4.9% in Q2 2026, its sharpest increase since Q3 2023.This uplift was second only to the 5.0% rise reported in the North East and markedly above the region’s historical norm (2.8%). Companies expect input costs to rise at the same pace over the next 12 months, higher than any other region and significantly ahead of the UK average projection (3.8%).

Yorkshire & Humber businesses increased their selling prices in line with the national average in the year to Q2 2026, with an average uplift of 2.5%. Businesses plan to pass on a larger proportion of the rise in input costs onto consumers in the year ahead by raising their selling prices by 2.9% over the next 12 months, widening the gap to the region’s historical norm (1.6%) and exceeding the prediction of almost all other UK regions.

With increased cost pressures and slowing sales growth in the year to Q2 2026, businesses in Yorkshire & Humber reported annual profits growth of 2.4%, lagging both the region’s historical norm and the national average (both 2.8%). Businesses are optimistic of improvements in the coming year, predicting profits expansion of 5.7% over the year ahead, notably higher than the 4.7% forecast nationally.

Capital investment and R&D

Annual capital investment growth in Yorkshire & Humber eased slightly from the previous quarter in Q2 2026, to 2.7%, matching the national increase. However, with heightened global uncertainty and elevated borrowing costs, businesses question the likely return on their investment and are planning to slow growth to 1.7% over the next 12 months, below both the region’s historical norm (2.0%) and the 1.8% rise forecast nationally.

Annual R&D budget growth in Yorkshire & Humber was 2.5% in Q2 2026, ahead of the 2.0% rate recorded nationally. Companies plan to bring growth in line with the historical norm over the next 12 months, to 1.7%, broadly matching the UK projection (1.8%).