Q1: Confidence dips deeper into negative territory and slips below the UK average.

The latest national Business Confidence Monitor (BCM) shows that business sentiment slipped deeper into negative territory amid uncertainty about the Budget and rising concern about both the tax burden and regulations. However, companies are optimistic that domestic sales and exports growth will improve over the next 12 months.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 12 January to 16 March 2026.

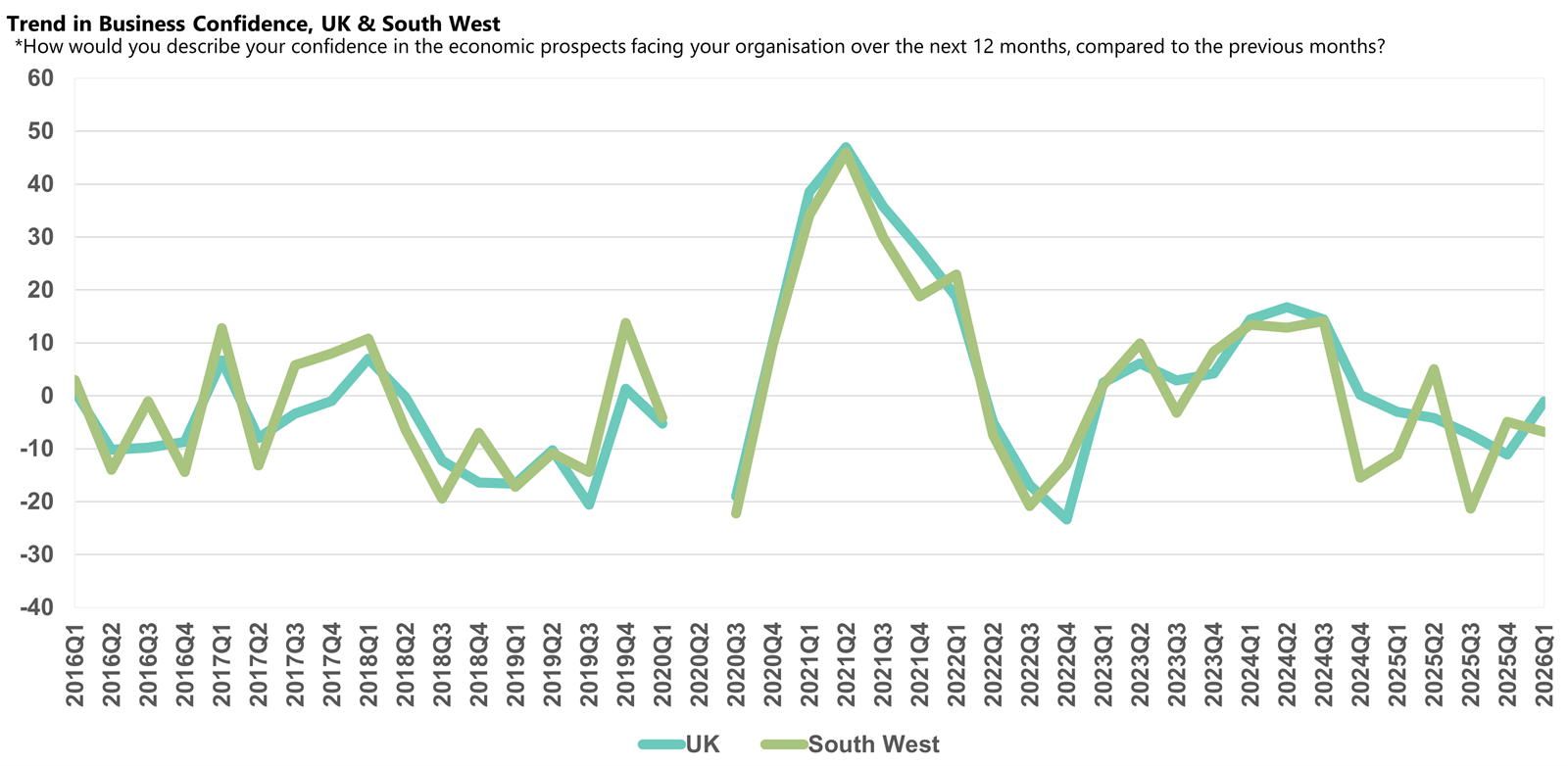

- Confidence among businesses in the South West dipped to -6.8 and below the UK score (-1.1).

- Domestic sales growth improved but exports growth slowed sharply and profits growth remained lacklustre.

- Businesses also reported the highest rate of input cost inflation in the UK.

- However, concern about the tax burden eased from record highs with labour costs now the most prominent rising business challenge.

- Labour demand is weak but companies remain upbeat about employment growth prospects.

- Investment and R&D growth increased significantly but businesses plan to slow expansion next year.

Business confidence in South West

Sentiment in the South West dipped in Q1 2026 with the score falling to -6.8 from -4.9 in the previous quarter, and below the UK average, which improved to -1.1. Confidence in the region remains well below its historical average (+3.4) and the South West is among the more pessimistic regions. The drop in confidence is likely linked to disappointing exports sales and profits growth alongside the highest reported input price inflation of any part of the UK.

Domestic sales and exports growth

Domestic sales growth edged further ahead of the historical average (3.1%), rising by 3.3% in the year to Q1 2026, although this was slightly weaker than the national average (3.5%). Companies maintained their optimism for the year ahead, again predicting domestic sales growth of 5.5%, comparable to the national projection (5.4%).

Reported annual exports growth however, at 0.9%, was relatively disappointing in Q1 2026, representing a sharp slowdown compared to the previous quarter (2.9%) and below the regional historical norm (2.7%). Projected growth of 3.8% for next year, although below the national average prediction (4.1%), would mark a significant improvement. However, businesses’ projections for domestic and exports sales were largely formed ahead of the outbreak of the Iran war and softened in the final weeks of the survey.

Input price, selling prices and profits growth

While input price inflation edged down in Q1 2026, annual growth of 4.0% was the highest reported in any region and significantly ahead of the UK average of 3.6%. Businesses anticipated inflation to ease further to 3.3% in the coming 12 months but the spikes in oil and gas prices due to the Middle East conflict increase the risk around these predictions.

Businesses lifted their selling prices by 2.9% in the year to Q1 2026, faster than the national average (2.3%) and significantly above the historical norm (1.7%). They anticipated prices would rise by 3.0% in the year ahead, above the UK average (2.3%) but rising costs could place further upward pressure on prices across all regions.

Profits growth remains subdued in the South West. Despite edging up to 2.3% in the year to Q1 2026, it remains short of the historical average (3.0%) and the national average (3.1%). While businesses predicted an improvement to 4.1% in the coming 12 months, it is the weakest projection of any region.

Labour market

Employment growth slowed to just 0.5% in the region in Q1 2026, but businesses remain upbeat about recruitment prospects for the year ahead, planning growth of 2.1%. While jobs growth in the region lagged the UK average (1.1%) over the past year it is expected to grow ahead of most regions and outperform the projected national rate (1.3%).

Alongside the highest reported input cost rises, salary inflation also ticked up for businesses in the South West. They reported that wages rose by 3.4% in the year to Q1 2026, outpacing the UK average (3.2%). Companies anticipate that the upward pressure on pay will ease to 2.7% in the coming 12 months, close to the national expectation (2.9%) but notably above the regional historical norm (2.2%).

While the proportion of businesses citing the availability of management skills as a rising challenge dropped sharply in Q1 2026, the availability of non-management skills (17%) remains a prominent issue for businesses in the South West, with only the West Midlands reporting a higher rate (18%).

Business challenges

Concern about the tax burden eased in the South West in Q1 2026, with 49% of businesses citing the issue as a growing challenge compared to 71% in the previous quarter. It is likely that the record survey high reported last quarter reflected the widespread uncertainty and speculation ahead of the November Budget. A similar trend was recorded across the UK, and the South West is now close to the UK average (53%).

The greatest concern for companies in the South West in Q1 2026 was labour costs, with the challenge reported by 68% of businesses, the highest rate across all UK regions. It was the first time the challenge was included in the survey, and the high rate likely reflects the rise in employer National Insurance Contributions last year and the rise in minimum wages, alongside concerns about the potential costs associated with the Employee Rights Act.

Among other widespread concerns, reports of regulations (47%) nudged down, while customer demand (45%) edged up. However, both remain above their respective regional historical norms. Companies were also asked about energy costs for the first time in the survey and the issue was reported as a growing challenge by 36% in the South West, comparable with the UK average (35%).

Investment

Annual capital investment improved again in Q1 2026, rising to 3.4% and comfortably above the regional historical norm (2.0%). The rate was among the fastest reported across all UK regions, second only to the East Midlands (4.4%). Businesses plan to slow growth to 2.0% next year, broadly comparable to the national projection (1.9%).

R&D budget growth improved from the slump reported last quarter and, at 1.9% in the year to Q1 2026, was close to the regional historical average (2.0%) and UK average (2.1%). However, in common with most parts of the UK businesses are pessimistic about the coming year and plan to slow expansion to just 1.5%, close to the UK projection (1.4%).