Key takeaways

- The UK had a relatively strong Q1 in 2026, driven by services.

- Inflation is unlikely to fall again in 2026 after April.

- Fuel, food and energy pressures are likely to push inflation back up.

- Iran's war has increased the risk of stagflation.

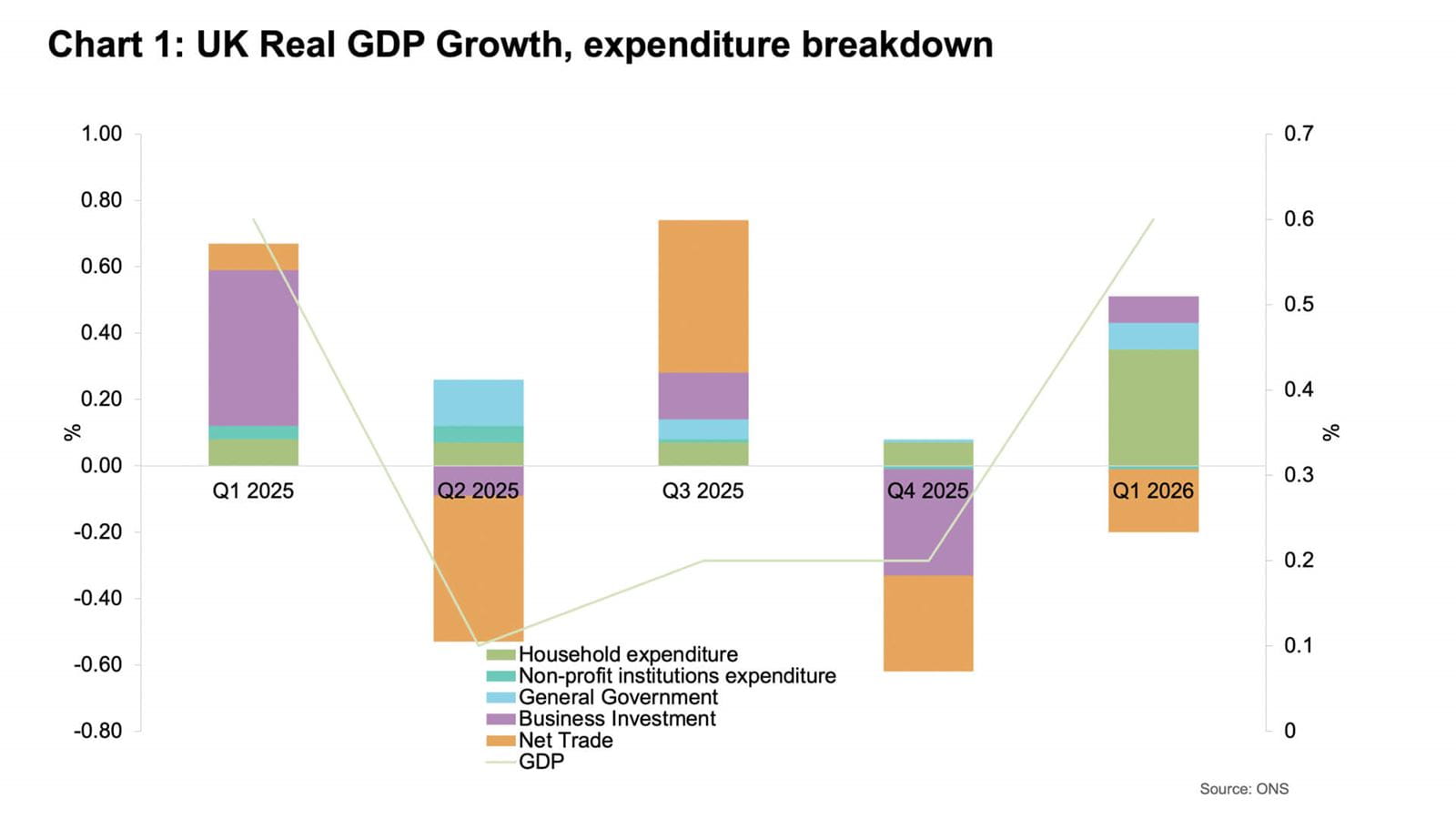

The UK experienced strong first quarter GDP growth

Official figures reveal that UK GDP grew by 0.6% in the first quarter of 2026 (see Chart 1), the fastest growth since Q1 2025 and up sharply from growth of 0.2% in the previous quarter.

This improvement was driven predominantly by the services sector, growing by 0.8%. Wholesale, computer programming and advertising firms all enjoyed a particularly strong start to the year.

Prefer to listen?

This audio file was produced by AI and has been adapted from the original article for audio purposes.

The production sector is estimated to have grown by 0.2% in Q1, down from 1.3% growth in the previous quarter, while construction output returned to growth of 0.4%, following a contraction of 2.8% in Q4 2025.

Business investment is estimated to have increased by 0.7% in the first quarter – still 1.8% lower than it was in the same quarter a year ago. Growth in household spending picked up in Q1 to 0.6%, from 0.1% in the previous quarter.

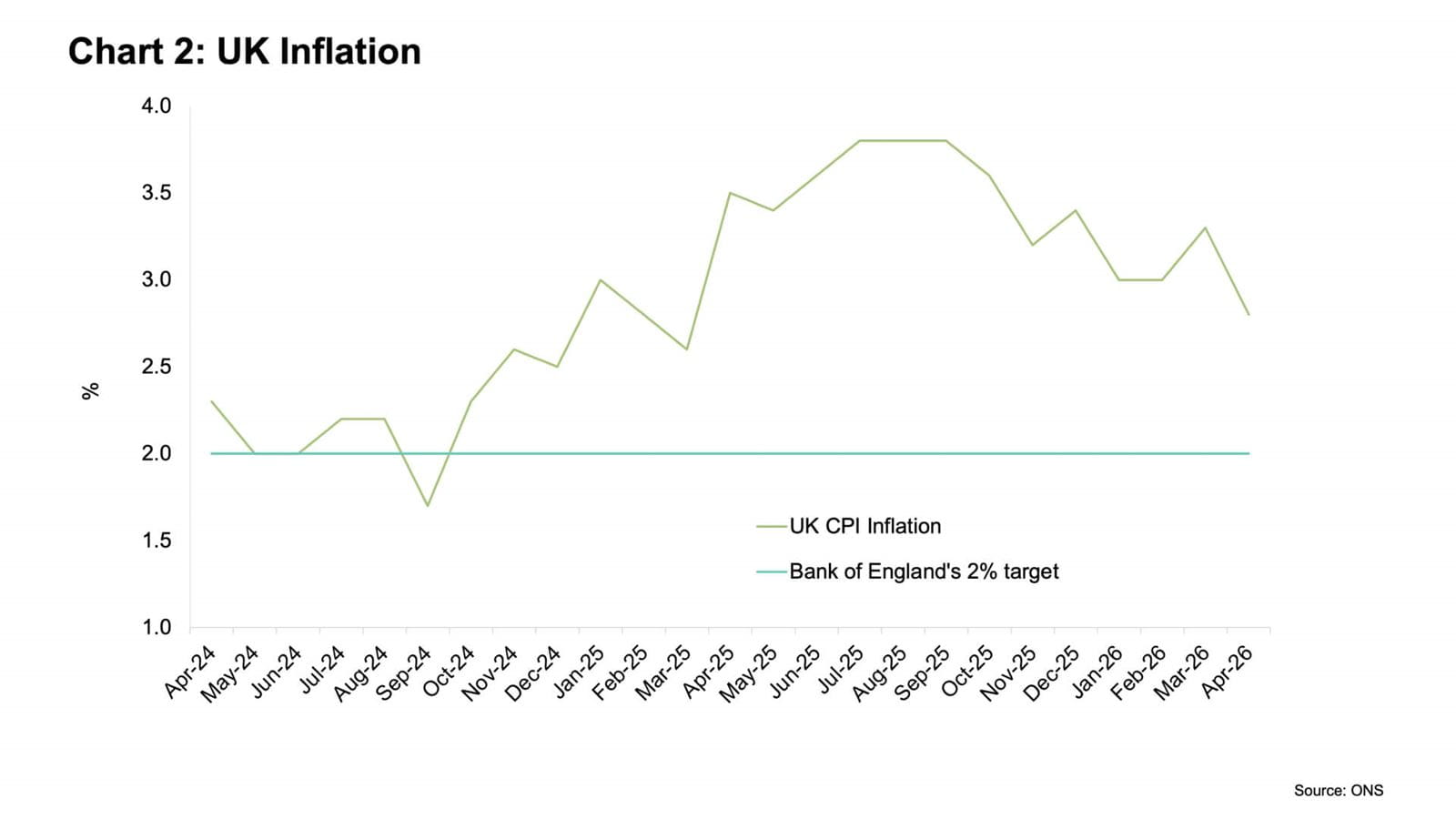

April’s inflation fall is only a temporary respite

UK Consumer Price Index (CPI) inflation stood at 2.8% in April 2026, down from 3.3% in March (see Chart 2). This slowdown was largely driven by lower electricity and gas prices. The cut to green levies announced in November’s Budget and lower wholesale energy prices – before the Iran conflict started – led to a notable reduction in April’s Ofgem Energy Price cap.

The largest upward pressure on inflation came from fuel costs. The average price of petrol stood at 156.8 pence per litre in April 2026, the highest price since November 2022, when it was 163.6 pence per litre following Russia’s invasion of Ukraine.

This could be the final fall in inflation this year, with surging fuel and food costs expected to push inflation to 4% this summer. On top of this, July’s Ofgem price cap reset will lead to significant increases in household energy bills.

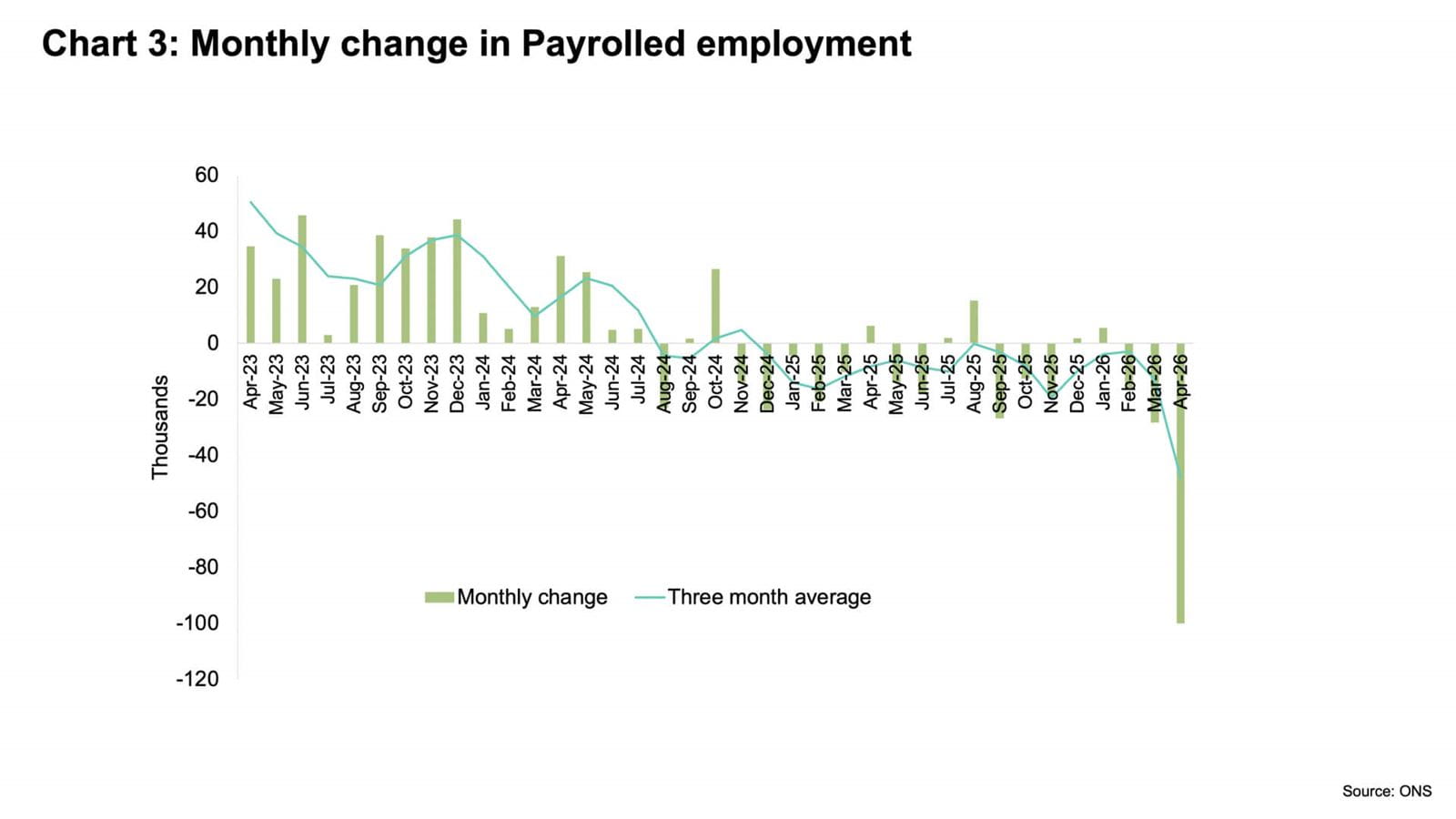

Softening labour market is facing a perilous jobs crunch

In the three months to March 2026, UK’s unemployment rate rose to 5%, from 4.9% in the three months to February. The number of payrolled employees dropped by 100,000 in April (see Chart 3), the largest decline since the early days of the COVID-19 pandemic in May 2020.

The number of job vacancies – a good indicator of labour demand – fell by 28,000 in the three months to March 2026 to 705,000. This is the lowest level of vacancies since 2021. Wholesale and retail trade experienced the largest decrease, down 7,000. The twin financial hit on businesses from skyrocketing energy costs and declining customer demand amid the Iran conflict means that the UK's unemployment rate could reach 6% by the end of this year.

UK interest rates are kept on hold – for now

The Bank of England has held interest rates at 3.75% – still higher than the average rate over the past decade of 1.32%. The Monetary Policy Committee members (MPC) voted eight to one in favour of this outcome, with the one dissenting voter calling for a 25 basis points rise.

The near unanimous backing among rate-setters for this decision suggests that interest rates are currently in a holding pattern as policymakers wait for more insight into the economic fallout from the Iran conflict before deciding whether or when to raise interest rates.

Bank of England’s new forecast scenarios highlight Iran’s potential impacts

The Bank of England also released its quarterly Monetary Policy Report which, given these uncertain times, sets out three scenarios for how the UK economy might react to changes brought about by the war in Iran:

- Scenario A: energy prices fall back and inflation, as measured by the CPI rises to 3.6% at the end of this year, before falling below 3% by autumn next year.

- Scenario B: energy prices fall back more slowly than in Scenario A, inflation rises to 3.7% this year and remains elevated for longer.

- Scenario C: oil prices stay above $120 a barrel for the rest of the year and inflation peaks at 6.2% at the beginning of next year. Such a scenario could see as many as six interest rate rises to 5.5%.

Taken together, the Bank’s new forecast scenarios suggest that the probability of interest rate rises – and stagflation – is increasing. Though interest rates could remain at 3.75% for the rest of the year, it will become an increasingly close call, with the vote split among committee members likely to turn more hawkish if inflation starts rising sharply.

Explainer: why is stagflation bad news?

Stagflation is a combination of three big negatives for businesses and households:

- slower economic growth,

- higher unemployment, and

- higher inflation.

It also makes setting policy (including interest rates) to correct these issues very difficult.

Implications for accountants, business owners and the economy

This strong start to 2026 is probably the high point for the economy this year. Output is likely to weaken in the coming months. Surging energy costs and supply chain disruption will suffocate activity, despite a short-term boost from firms stockpiling in anticipation of shortages and price rises.

A prolonged period of domestic political instability would cast another dark cloud over the UK’s economic outlook by further denting confidence and increasing financial market turbulence, likely resulting in notably weaker spending and investment.

What to watch out for next month

- The April 2026 GDP data, to be released on 12 June, is likely to show that the UK GDP growth slowed from 0.3% in March.

- The inflation figures for April, out on 17 June, may see the headline rate rise slightly from the 2.8% recorded in April.

- On 18 June, the Bank of England’s MPC is expected to keep interest rates at their current rate of 3.75%.

Further support

Resources

Economy

Expert analysis on the latest national and international economic issues and trends, and interviews with prominent voices across the finance industry alongside data on the state of economy.

Visit the hubResearch

UK Business Confidence

ICAEW's Business Confidence Monitor is one of the largest and most comprehensive quarterly surveys of business conditions and the health of the UK economy.

Read the latest findingsICAEW support

Training and events

Browse upcoming and on-demand ICAEW events and webinars looking at the global economy and trade.

Events and webinars A-Z of CPD Courses