Guidance for CFOs and audit committees on reporting and assuring scope 3 greenhouse gas emissions related to asset management. Find out about methods of estimating emissions and common challenges.

ICAEW's Financial Services Faculty has worked with members from within the sector and experts from the Partnership for Carbon Accounting Financials (PCAF) to outline estimation methodologies for those reporting and assuring on greenhouse-gas emissions relating to asset management.

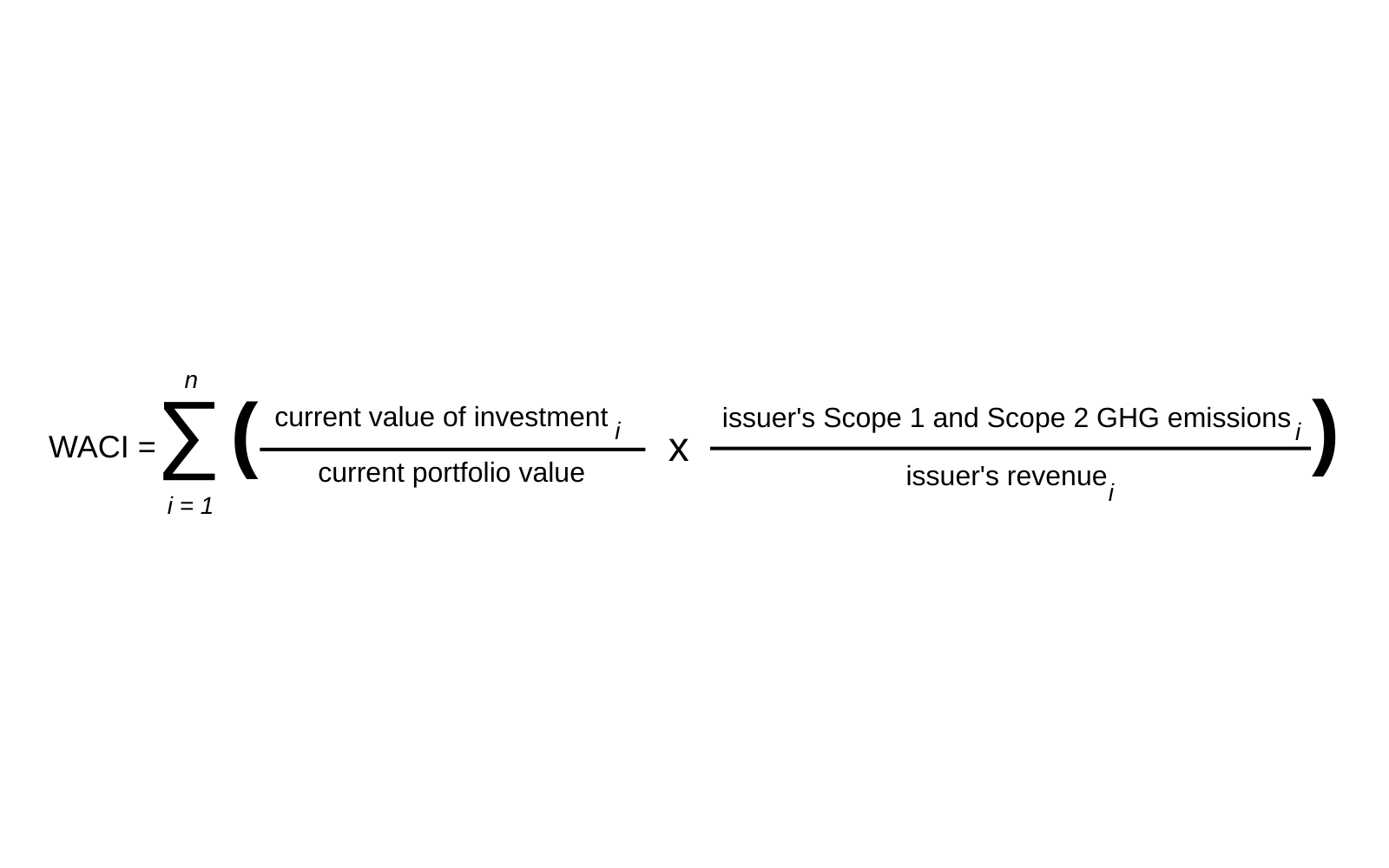

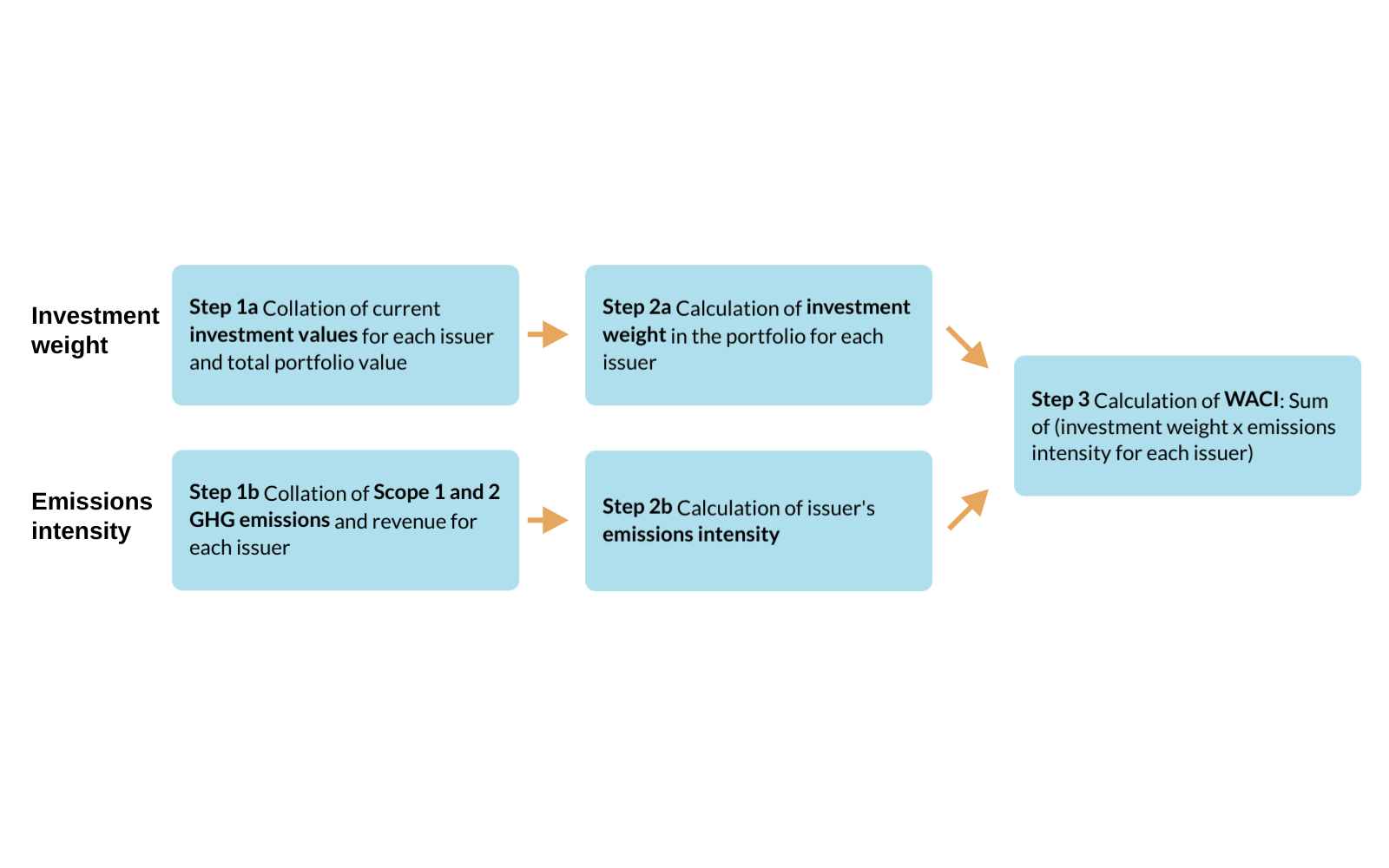

We begin by looking at the process flow for calculating weighted average carbon intensity (WACI) for investment.

Investment WACI process flow

The WACI is expressed as tCO2e/€M or $M company revenue and can be used to understand a portfolio’s exposure to emission-intensive companies.

Note:

- Applicable asset classes: Listed equity and corporate fixed income

- To calculate WACI for sovereign issuers, collate the issuers’ GHG emissions and GDP data instead

| Metric | Purpose | Description |

|---|---|---|

| Absolute emissions | To understand the climate impact of loans and investments and set a baseline for climate action | The total GHG emissions of an asset class or portfolio |

| Economic emission intensity | To understand how the emission intensities of different portfolios (or parts of portfolios) compare to each other per monetary unit | Absolute emissions divided by the loan or investment volume in EUR or USD, expressed as tCO₂e/€M or tCO₂e/$M loaned/invested |

| Physical emission intensity | To understand the efficiency of a portfolio (or parts of a portfolio) in terms of total GHG emissions per unit of a common output | Absolute emissions divided by a value of physical activity or output, expressed as tCO₂e/MWh, tCO₂e/tonne product produced |

| Weighted average carbon intensity (WACI) | To understand exposure to emission-intensive companies | Portfolio’s exposure to emission intensive companies, expressed as tCO₂e/€M or $M company revenue |

Source: PCAF Standard Part A - The Global GHG Accounting and Reporting Standard for the Financial Industry: Table 2-1 p22 Financed emissions metrics

Carbon footprinting and exposure

The Task Force on Climate-related Financial Disclosures (TCFD) has created a table detailing common carbon footprinting and exposure metrics on pp52-54 of Implementing the Recommendations of the TCFD (2021).

Guidance created with permission from PCAF

This guidance is based, with permission, upon the work of the Partnership for Carbon Accounting Financials (PCAF) including the data quality score tables from The Global GHG Accounting and Reporting Standard for the Financial Industry. Any discussion of implementation challenges, lessons learned, interpretations, or other commentary are the views and experiences of contributors and not those of PCAF. Please refer to the PCAF Standard for complete guidance. In the event of any inconsistency between the guidance and the PCAF standard, the standard should be considered the authoritative source and take precedence.

More support

Read more case studies and a list of common challenges facing financial services organisations when reporting and assuring scope 3 emissions.

Case studiesChallenges