The tax gap is the difference between what HMRC expects the total tax receipts to be and the actual tax received. In its latest annual update on 23 June 2026, HMRC published its estimates for the tax gap for 2024/25 and revised its estimates for earlier years.

Figures should be treated with caution

HMRC’s estimate of the tax gap for 2023/24 has increased from 5.3% (when first published, in June 2025) to 6% of total tax liabilities. HMRC says that this “illustrates the uncertainty around the estimation of tax gaps and highlights why they are best used as a long-term indicator of compliance”.

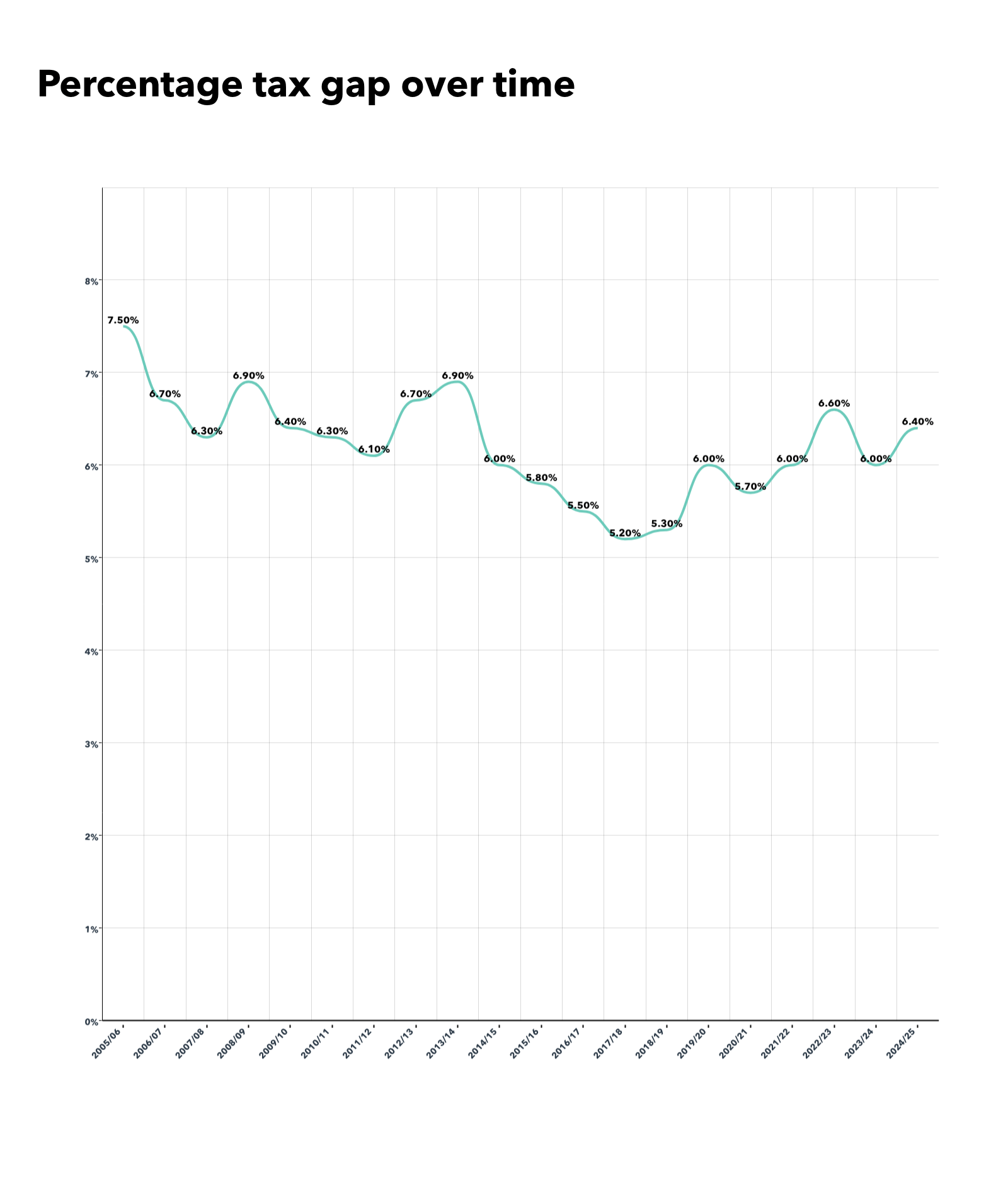

Percentage tax gap

The tax gap has increased as a percentage of tax liabilities, from the revised estimate of 6% for 2023/24 to 6.4% for 2024/25. Although the tax gap for 2024/25 is lower than that for 2005/06 (7.5%), it exceeds the figures for the years before the COVID-19 pandemic (eg, the low point of 5.2% for 2017/18). However, HMRC notes that “there is emerging evidence that the small businesses Corporation Tax gap may be understated for years before 2019 to 2020”.

The government has announced a package of measures intended to close the tax gap at recent fiscal events, including at the Spring Statement 2025. In a press release published alongside the figures, the government says that “measures to close the tax gap, announced by the government since Autumn Budget 2024, will raise a further £10 billion a year by 2029 to 2030”.

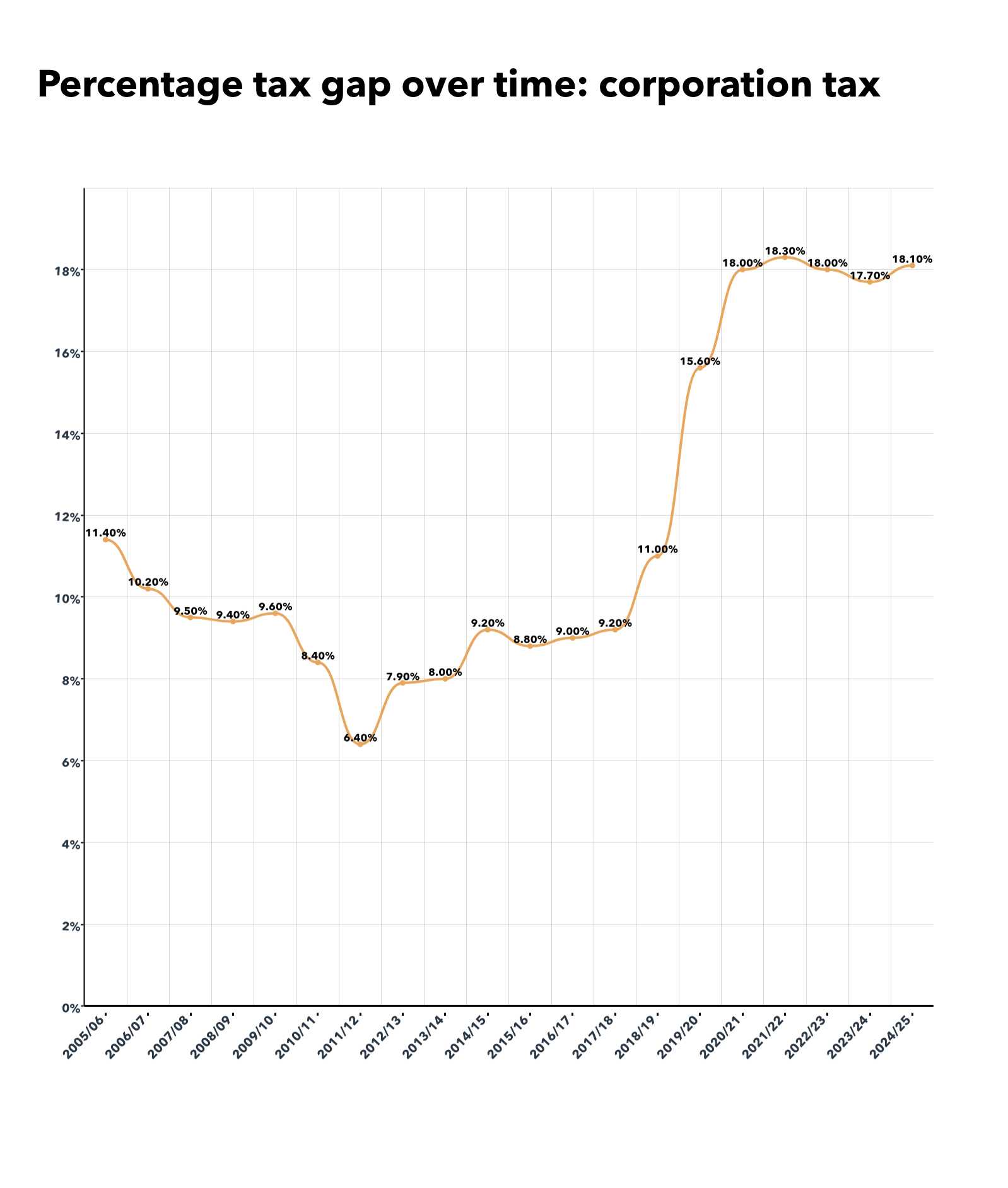

Tax gap by type of tax

The tax gap for most taxes has followed a downward trend since 2005/06. However, the percentage tax gap for corporation tax had increased significantly in recent years and is estimated to be 18.1% for 2024/25. It has been as low as 6.4% in 2011/12. Corporation tax accounted for 35% of the tax gap for 2024/25.

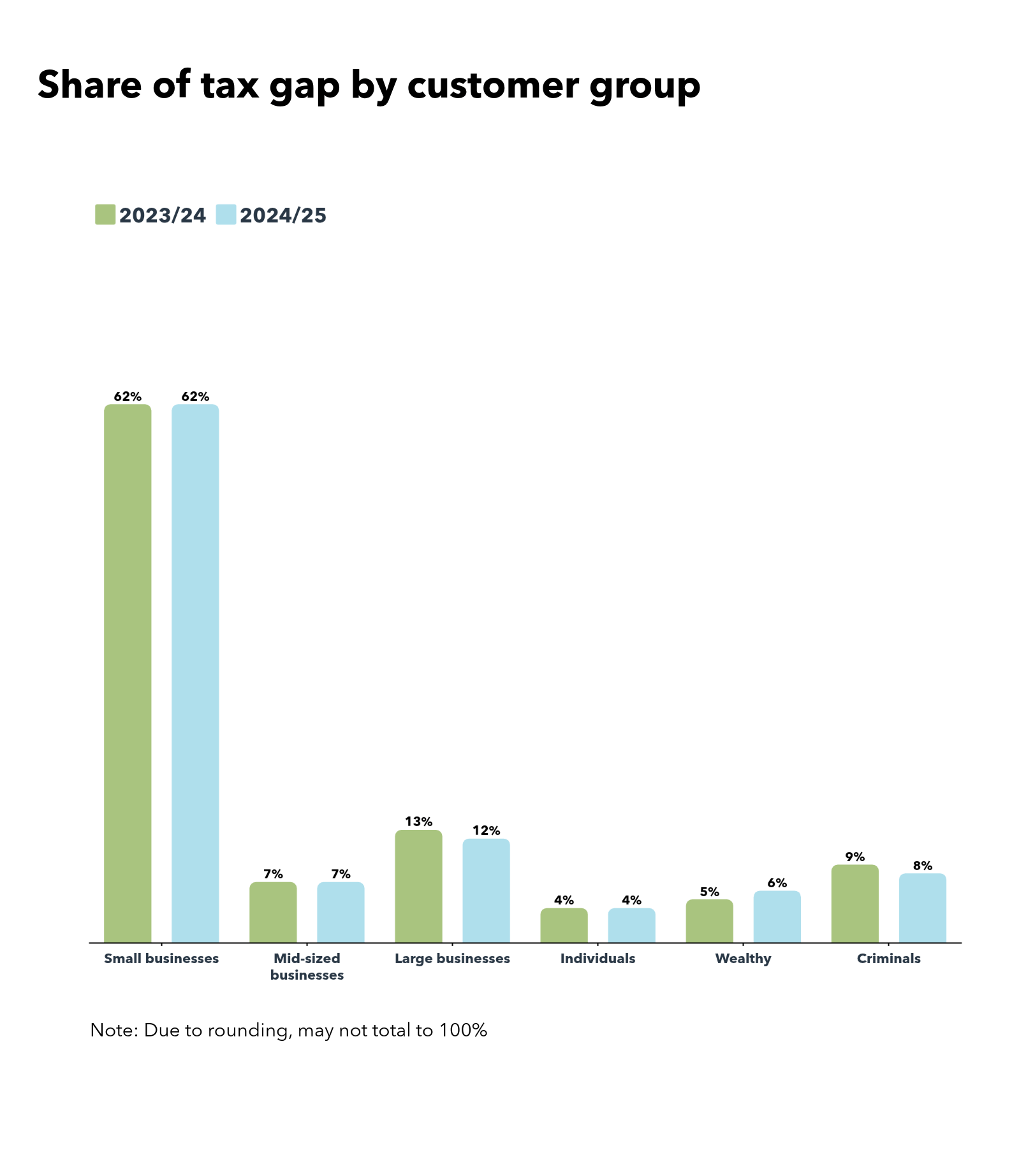

Tax gap by customer group

The share of the tax gap attributed to small businesses has increased in recent years, from 40% of the overall tax gap for 2017/18 to 62% for 2024/25 (although, as noted above, HMRC suspects that the small business corporation tax gap may have been understated for earlier years).

HMRC believes that 55% of small companies may be submitting incorrect returns, with 34% of small companies submitting returns that contain inaccuracies where the additional tax payable is more than £1,000. What the data does not reveal is whether there are any specific causes or trends behind these errors.

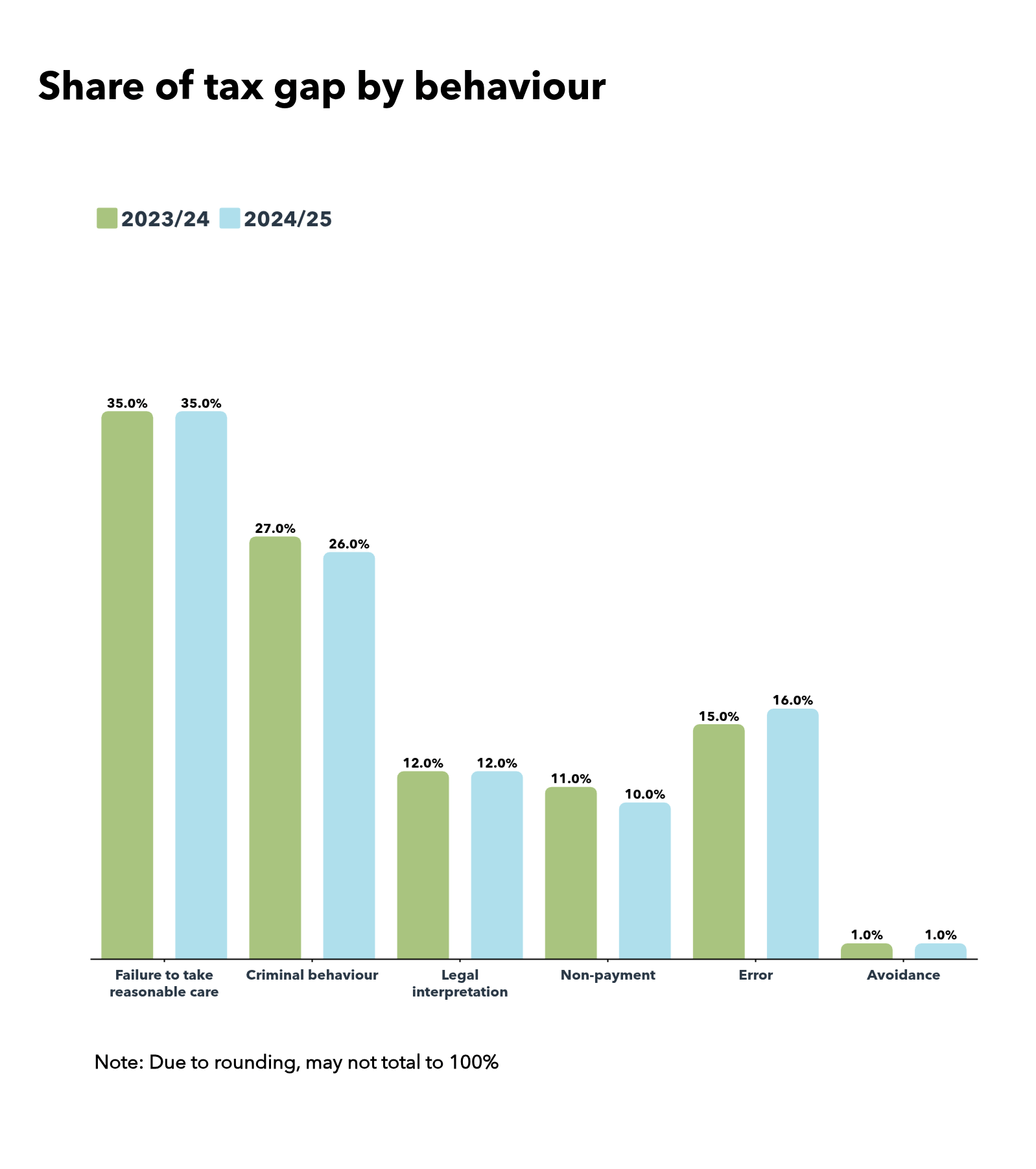

Tax gap by behaviour

Failure to take reasonable care is the largest component of the tax gap by behaviour, at 35% for 2024/25 – the same figure as for 2023/24.

What ICAEW views as criminal behaviour is subdivided by HMRC into evasion, criminal attacks and the hidden economy. These have been combined as ‘criminal behaviour’ in the chart below and are equivalent to 26% of the tax gap for 20024/25, down from 27% for 2023/24.

The Tax Faculty

ICAEW's Tax Faculty is recognised internationally as a leading authority and source of expertise on taxation. The faculty is the voice of tax for ICAEW, responsible for all submissions to the tax authorities. Join the Faculty for expert guidance and support enabling you to provide the best advice on tax to your clients or business.

Further resources

Latest news

TAXwire and Tax Track

Stay up to date with the latest developments by signing up to the Tax Faculty's weekly enewsletter and listening to the Tax Track podcast series.

Listen now Newsletter sign upPractical guidance

Tax Faculty resources

The Tax Faculty offers expert guidance and support enabling you to provide the best advice on tax legislation to your clients or business. We offer clear direction in taxing times. Membership is open to everyone.

ICAEW support

Training and events

Browse upcoming and on-demand ICAEW events and webinars focused on developments in tax practice and policy.

Events and webinars CPD courses and more