This case study aims to support those in the banking sector considering how to approach the reporting and assurance of scope 3, category 15 emissions in relation to sectors, such as metal production. It outlines estimation methodologies for 'physical-intensity-based finance emissions'.

ICAEW's Financial Services Faculty has worked with members from within the sector and experts from the Partnership for Carbon Accounting Financials to outline estimation methodologies for those reporting and assuring on greenhouse-gas emissions relating to corporate banks' business loans and unlisted equity.

Outlined below is the calculation methodology for portfolio-level physical-intensity finance emissions. While the methodology is agnostic across sectors it is particularly appropriate for sectors where the ambition is for activity to become more efficient per unit of selected physical activity, for example metal production (ie aluminium or steel) and power utilities.

Other methodologies for lending that falls within the asset class 'business loans and unlisted equity' by corporate banks, include absolute financed emissions (most appropriate for fossil fuel sectors) and alignment delta based financed emissions (most appropriate for shipping and aviation sectors).

Estimation methodologies

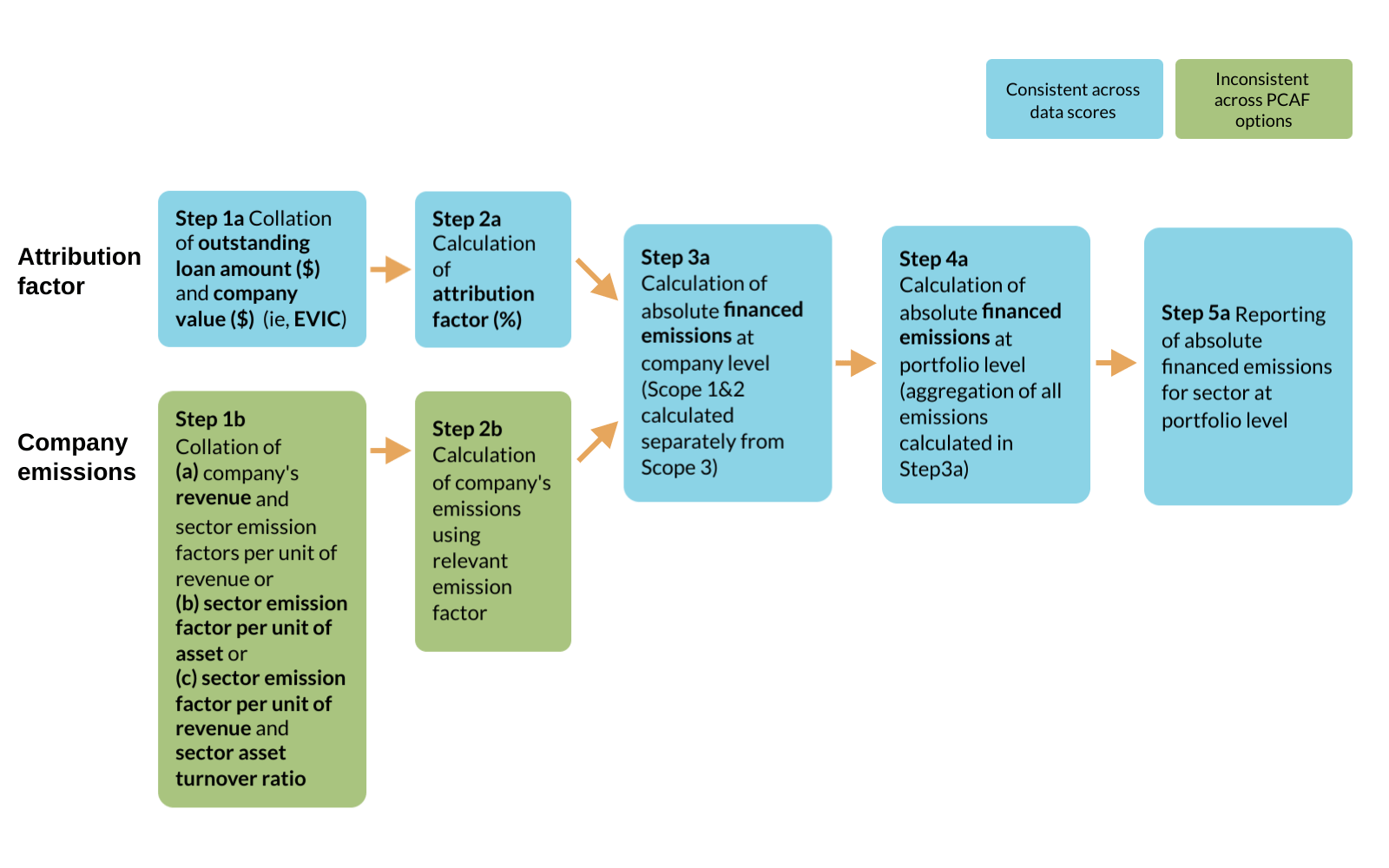

Overall process flow

This figure outlines the overall process flow for calculation of financed emissions for business loans and unlisted equity using a physical-intensity based financed emissions methodology.

Note: PCAF Data quality scores should be calculated and disclosed separately for Scope 1 and 2, and Scope 3.

Data quality scores

Within its Global GHG Accounting and Reporting Standard for the Financial Industry, the PCAF shows data quality scores, defined based on the source of company emissions used, which are outlined in the table below:

Data quality |

Options to estimate the financed emissions |

When to use each option |

|

|---|---|---|---|

Score 1 |

Option 1: Reported emissions |

1a |

Outstanding amount in the company and total company equity plus debt are known. Verified emissions of the company are available. |

Score 2 |

Option 1: Reported emissions |

1b |

Outstanding amount in the company and total company equity plus debt are known. Unverified emissions calculated by the company are available. |

Score 2 |

Option 2: Physical activity-based emissions |

2a |

Outstanding amount in the company and total company equity plus debt are known. Reported company emissions are not known. Emissions are calculated using primary physical activity data for the company's energy consumption and emission factors specific to that primary data. Relevant process emissions are added. |

Score 3 |

Option 2: Physical activity-based emissions |

2b |

Outstanding amount in the company and total company equity plus debt are known. Reported company emissions are not known. Emissions are calculated using primary physical activity data for the company's production and emission factors specific to that primary data. |

Score 4 |

Option 3: Economic activity-based emissions |

3a |

Outstanding amount in the company, total company equity plus debt, and the company's revenue are known. Emission factors for the sector per unit of revenue are known (eg, tCO2e per euro or dollar of revenue earned in a sector). |

Score 5 |

Option 3: Economic activity-based emissions |

3b |

Outstanding amount in the company is known. Emission factors for the sector per unit of asset (eg tCO2e per euro or dollar of asset in a sector) are known. |

Score 5 |

Option 3: Economic activity-based emissions |

3c |

Outstanding amount in the company is known. Emission factors for the sector per unit of revenue (eg tCO2e per euro or dollar of revenue earned in a sector) and asset turnover ratios for the sector are known. |

Financed emissions calculation

Figure 2 shows the financed emissions calculation methodology, based on the information available to the reporting entity to achieve specific PCAF data quality scores. It shows an indicative approach for an activity-based intensity metric. Data quality scores should be weighted by asset/transaction level exposure.

Notes:

- estimated emissions using energy consumption data are awarded a PCAF data quality score of 2.

- estimated emissions using production data are awarded a PCAF data quality score of 3.

Guidance created with permission from PCAF

This guidance is based, with permission, upon the work of the Partnership for Carbon Accounting Financials (PCAF) including the data quality score tables from The Global GHG Accounting and Reporting Standard for the Financial Industry. Any discussion of implementation challenges, lessons learned, interpretations, or other commentary are the views and experiences of contributors and not those of PCAF. Please refer to the PCAF Standard for complete guidance. In the event of any inconsistency between the guidance and the PCAF standard, the standard should be considered the authoritative source and take precedence.

Scope 3 support

A series of case-studies to help those in financial services understand estimation methodologies for Scope 3 emissions across different asset classes and client industries.

More support

Read more case studies and a list of common challenges facing financial services organisations when reporting and assuring scope 3 emissions.

Case studiesChallenges