Guidance for CFOs and audit committees on reporting and assuring scope 3 greenhouse gas emissions related to corporate bank loans using alignment delta-based financed emissions metrics. These metrics are often sector specific, where industry guidance may have set net-zero trajectories, such as shipping and aviation.

ICAEW's Financial Services Faculty has worked with members from within the sector and experts from the Partnership for Carbon Accounting Financials to outline estimation methodologies for those reporting and assuring on greenhouse-gas emissions relating to corporate banks' business loans and unlisted equity.

Outlined below is the calculation methodology for portfolio-level alignment data based on financed emissions. Alignment delta-based metrics are often sector specific, where industry guidance for specific sectors may have set net-zero trajectories, and banks financing counterparties in these sectors will report on the alignment of their portfolio to the set emissions trajectory (for example, shipping and aviation).

Other methodologies for lending that falls within the asset class 'business loans and unlisted equity' by corporate banks, include absolute financed emissions (most appropriate for fossil fuel sectors) and physical intensity-based financed emissions (most appropriate for metals production and power utilities)

Estimation methodologies

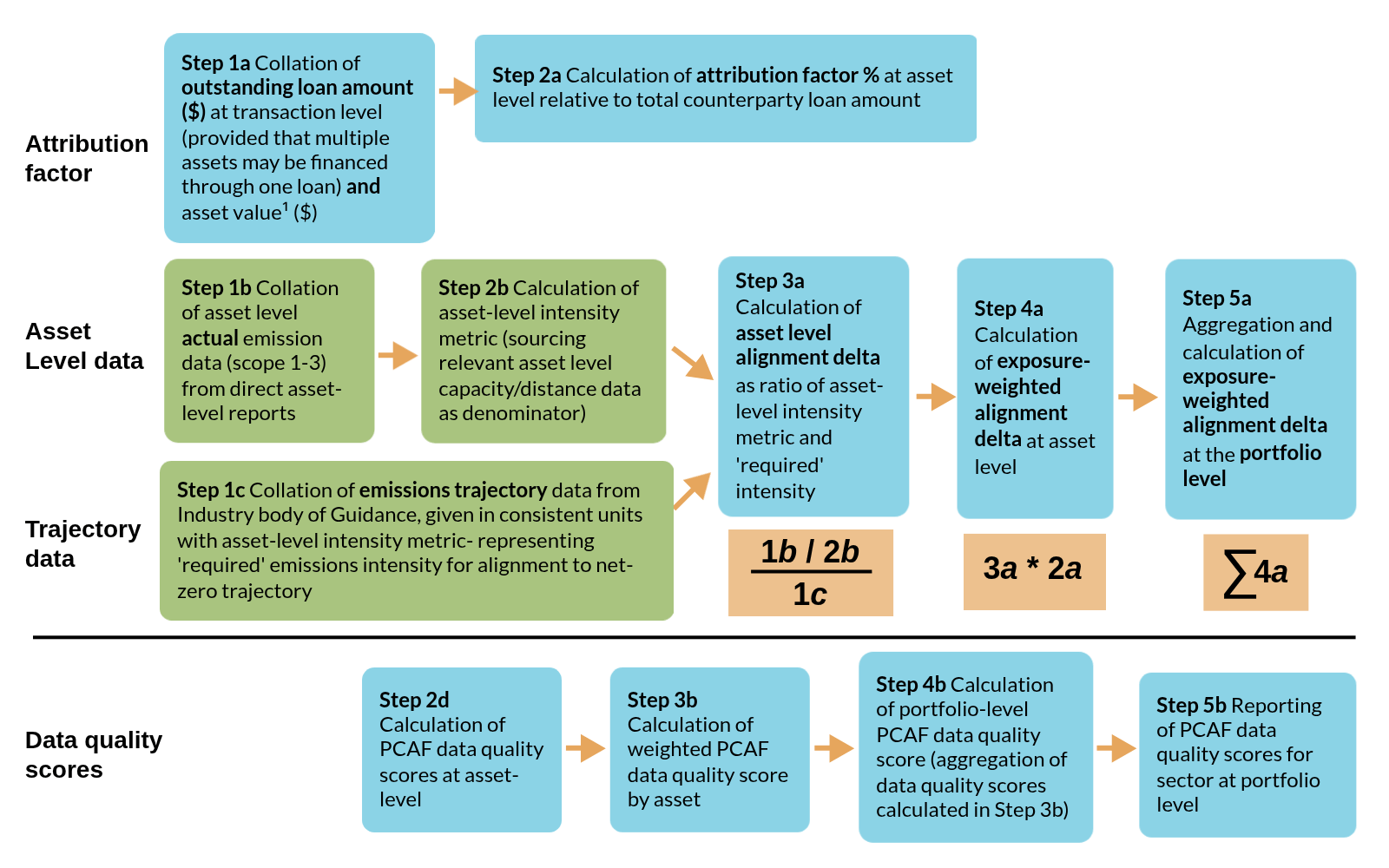

Overall process flow

This figure outlines the overall process flow for calculation of financed emissions for business loans and unlisted equity using an alignment delta-based calculation methodology. This serves as a general example, but preparers should follow available industry guidance to calculate alignment details for differing sectors.

Notes:

- Asset value data is relevant where multiple assets financed through one loan and thus asset values used to apportion loan exposure across the assets.

- PCAF Data quality scores should be calculated and disclosed separately for Scope 1 and 2, and Scope 3.

- Preparers should confirm with data provider the appropriate PCAF data score to apply based on the data submitted by reporting counterparties. Following confirmation, reporters should apply data quality scores to step 2a and sum these for all assets in scope.

Data quality scores

Within its Global GHG Accounting and Reporting Standard for the Financial Industry, the PCAF shows data quality scores, defined based on the source of company emissions used, which are outlined in the table below:

Data quality |

Options to estimate the financed emissions |

When to use each option |

|

|---|---|---|---|

Score 1 |

Option 1: Reported emissions |

1a |

Outstanding amount in the company and total company equity plus debt are known. Verified emissions of the company are available. |

Score 2 |

Option 1: Reported emissions |

1b |

Outstanding amount in the company and total company equity plus debt are known. Unverified emissions calculated by the company are known. |

Score 2 |

Option 2: Physical activity-based emissions |

2a |

Outstanding amount in the company and total company equity plus debt are known. Reported company emissions are not known. Emissions are calculated using primary physical activity data for the company's energy consumption and emission factors specific to that primary data. Relevant process emissions are added. |

Score 3 |

Option 2: Physical activity-based emissions |

2b |

Outstanding amount in the company and total company equity plus debt are known. Report company emissions are not known. Emissions are calculated using primary physical activity data for the company's production and emission factors specific to the primary data. |

Score 4 |

Option 3: Economic activity-based emissions |

3a |

Outstanding amount in the company, total company equity plus debt, and the company's revenue are known. Emission factors for the sector per unit of revenue are known (for example, tCO2e per euro or dollar of revenue earned in a sector). |

Score 5 |

Option 3: Economic activity-based emissions |

3b |

Outstanding amount in the company is known. Emission factors for the sector per unit of asset (for example, tCO2e per euro or dollar of asset a sector) are known. |

Score 5 |

Option 3: Economic activity-based emissions |

3c |

Outstanding amount in the company is known. Emission factors for the sector per unit of asset (for example, tCO2e per euro or dollar of asset a sector) are known and asset turnover ratios for the sector are known. |

Guidance created with permission from PCAF

This guidance is based, with permission, upon the work of the Partnership for Carbon Accounting Financials (PCAF) including the data quality score tables from The Global GHG Accounting and Reporting Standard for the Financial Industry. Any discussion of implementation challenges, lessons learned, interpretations, or other commentary are the views and experiences of contributors and not those of PCAF. Please refer to the PCAF Standard for complete guidance. In the event of any inconsistency between the guidance and the PCAF standard, the standard should be considered the authoritative source and take precedence.

More support

Read more case studies and a list of common challenges facing financial services organisations when reporting and assuring scope 3 emissions.

Case studiesChallenges