Guidance for CFOs and audit committees on reporting and assuring scope 3 greenhouse gas emissions related to corporate bank investments. Find out about methods of estimating emissions and common challenges.

ICAEW's Financial Services Faculty has worked with members from within the sector and experts from the Partnership for Carbon Accounting Financials (PCAF) to outline estimation methodologies for those in corporate investment. This example focuses on corporate bond issuances. Other financial instruments such as government bonds and short-term money market instruments are not included.

Facilitated Emissions are the emissions associated with primary capital market issuance activities (debt and equity). It involves arranging transactions generally without direct capital exposure and thus no transaction recorded on the financial institutions’ balance sheet. There is no direct capital risk (except when the facilitator of a capital market instrument has underwritten any part of the issuance).

Given that no direct funding is provided by the facilitator to the company producing emissions; along with the very short-term role facilitators have in their roles as arrangers, a unit of facilitated emissions is not equal to a unit of financed emissions. For these reasons, a 33% weighting factor is applied to reflect the less direct impact on emissions.

Estimation methodologies

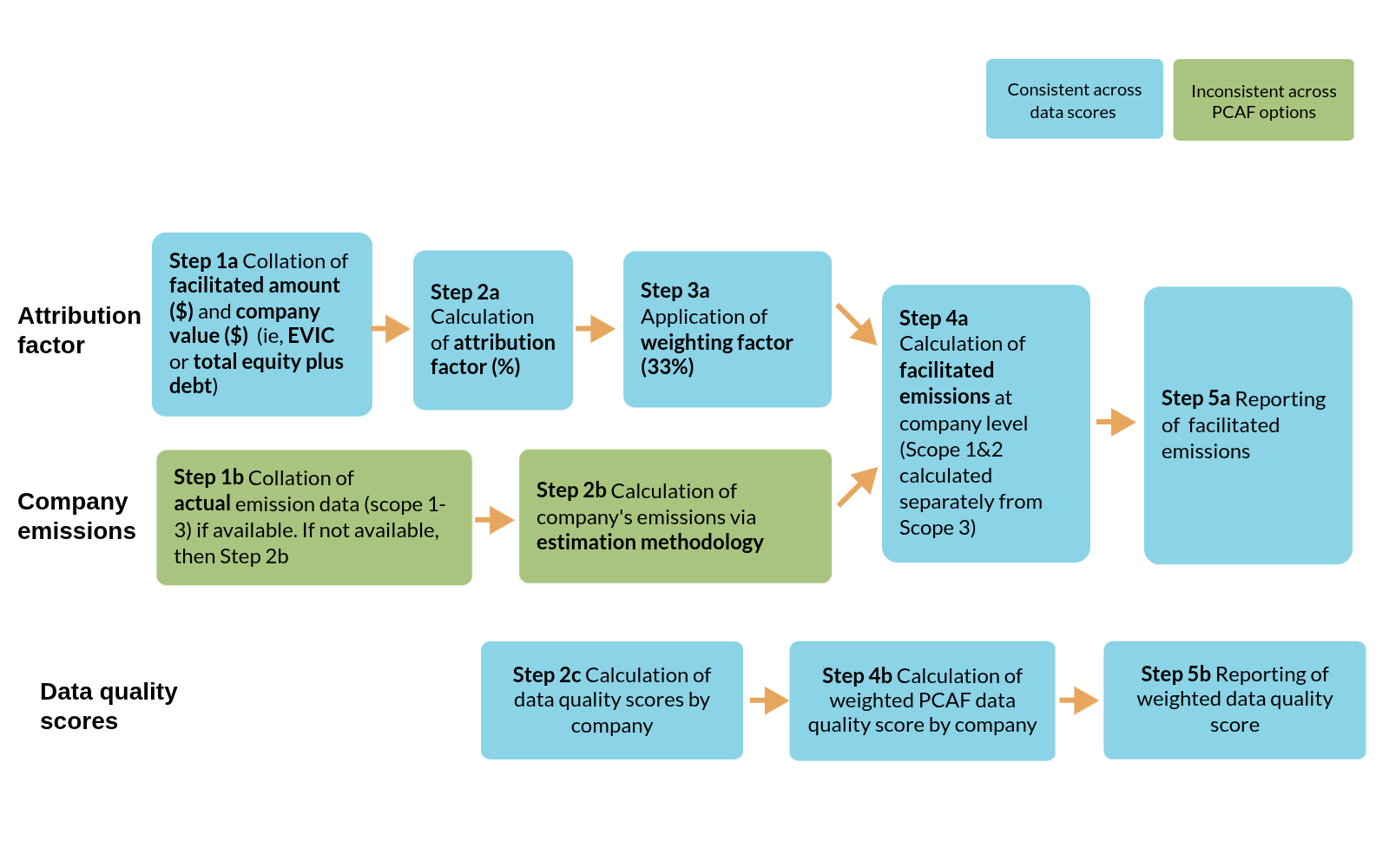

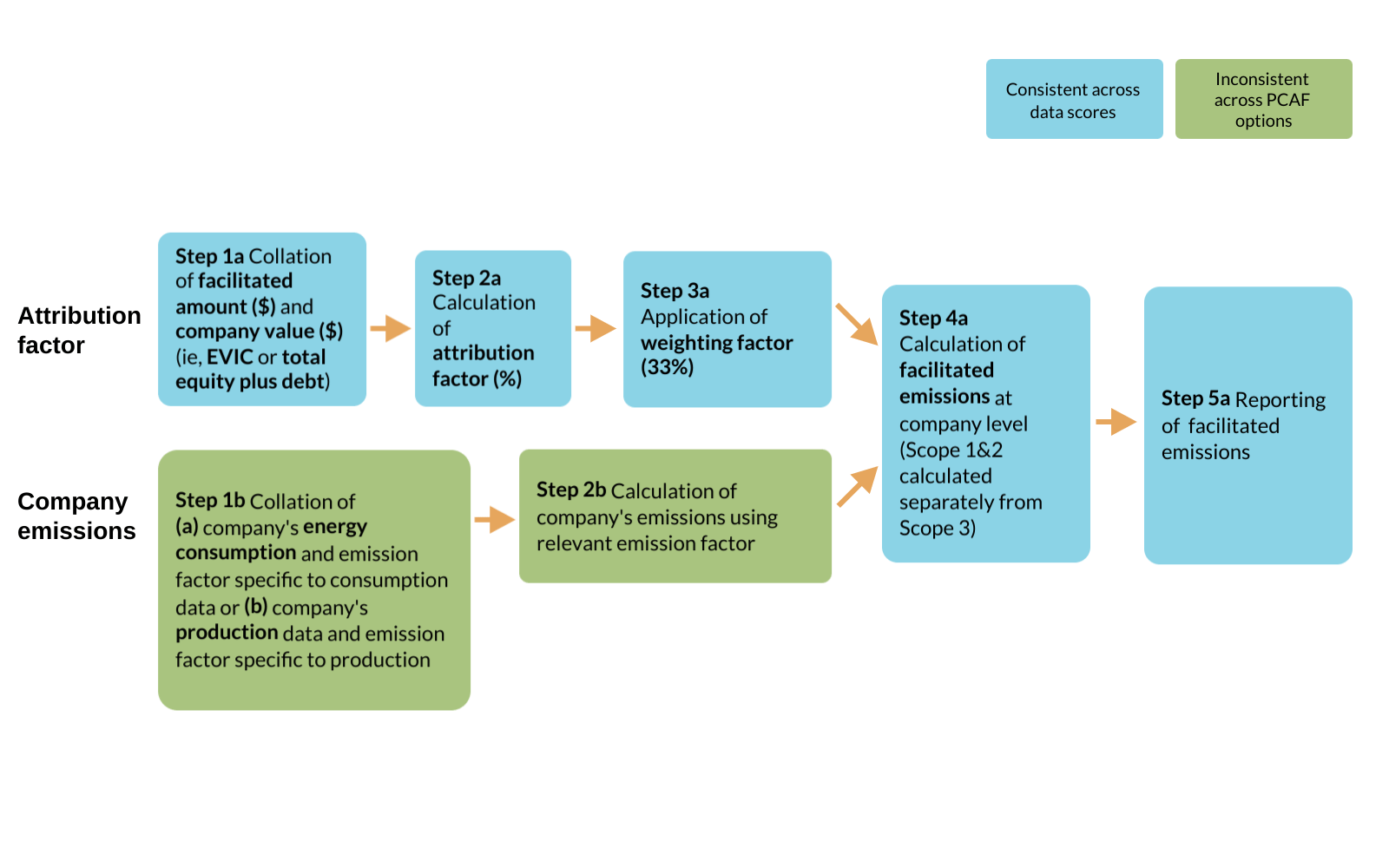

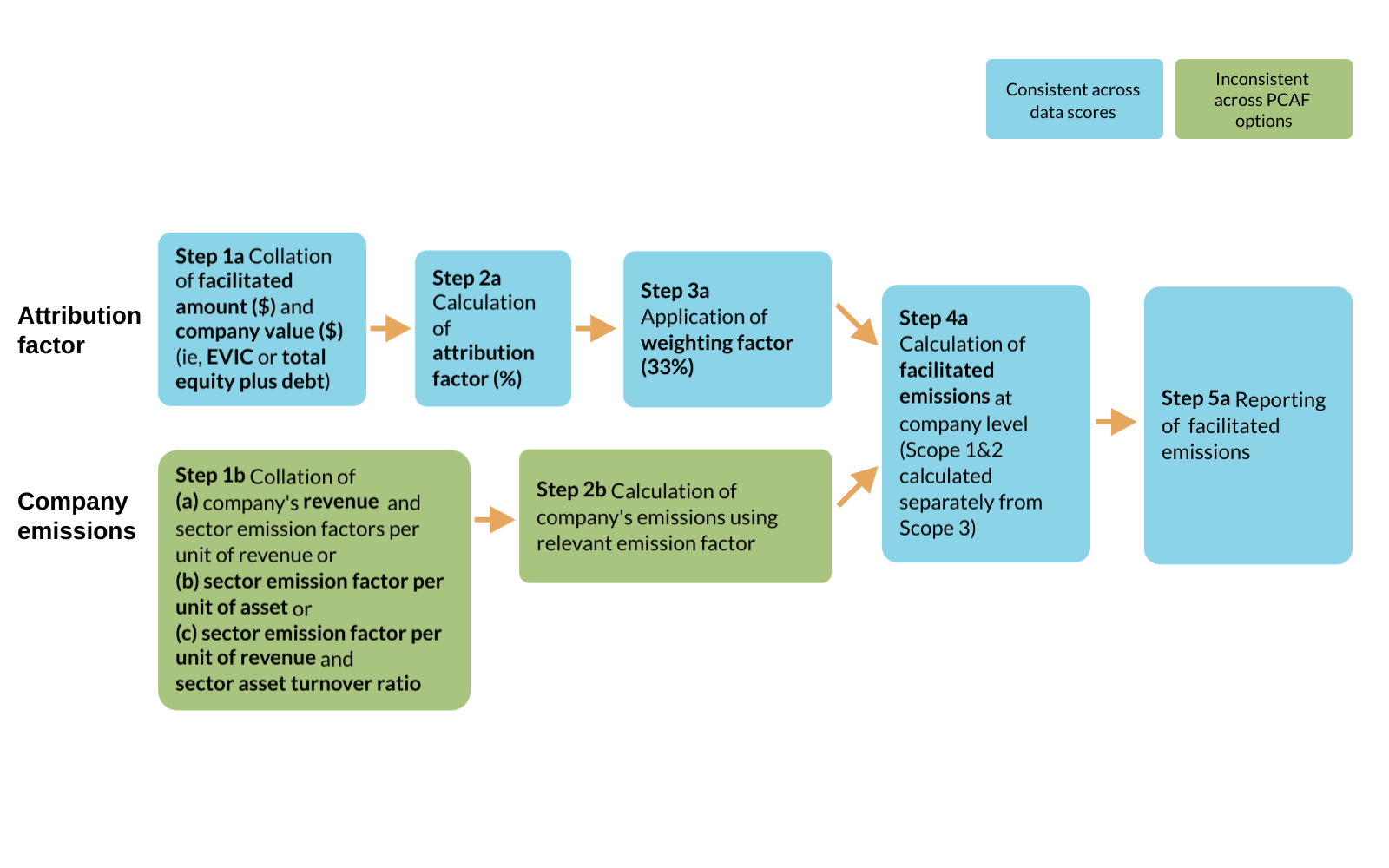

Overall process flow

This figure outlines the overall process flow for the calculation of financed emissions from debt capital markets (across all PCAF options).

Key source: PCAF Standard Part B - The Global GHG Accounting and Reporting Standard for Capital Markets.

Notes:

- EVIC (enterprise value including cash) is either sourced directly or calculated using known company financials.

- PCAF data quality scores should be calculated and disclosed separately for Scope 1 and 2, and Scope 3.

Data quality scores

Within its Global GHG Accounting and Reporting Standard for Capital Markets (table 5-2 on p36), the PCAF further splits possible data quality scores into three different 'options' depending on data availability which are outlined in the table below:

Data quality |

Options to estimate the facilitated emissions |

When to use each option |

|

|---|---|---|---|

Score 1 |

Option 1: Reported emissions |

1a |

Facilitated amount and EVIC or total equity plus debt are known. Verified emissions of the company are available. |

Score 2 |

Option 1: Reported emissions |

1b |

Facilitated amount and EVIC or total equity plus debt are known. Unverified emissions calculated by the company are available. |

Score 2 |

Option 2: Physical activity-based emissions |

2a |

Facilitated amount and EVIC or total equity plus debt are known. Reported company emissions are not known. Emissions are calculated using primary physical activity data for the company's energy consumption and emission factors specific to that primary data. Relevant process emissions are added. |

Score 3 |

Option 2: Physical activity-based emissions |

2b |

Facilitated amount and EVIC or total equity plus debt are known. Reported company emissions are not known. Emissions are calculated using primary physical activity data of the company's production and emission factors specific to that primary data. |

Score 4 |

Option 3: Economic activity-based emissions |

3a |

Facilitated amount and EVIC or total equity plus debt, and the company's revenue are known. Emission factors for the sector per unit of revenue are known (eg, tCO2e per euro or dollar of revenue earned in a sector). |

Score 5 |

Option 3: Economic activity-based emissions |

3b |

Facilitated amount is known. Emission factors for the sector per unit of asset (eg tCO2e per euro or dollar of asset in a sector) are known. |

Score 5 |

Option 3: Economic activity-based emissions |

3c |

Facilitated amount is known. Emission factors for the sector per unit of revenue (eg tCO2e per euro or dollar of revenue earned in a sector) and asset turnover ratios for the sector are known. |

Notes:

- verified emissions (ie, assured) are awarded a PCAF data quality score of 1.

- unverified emissions calculated by the company (ie, unassured) are awarded a PCAF data quality score of 2.

Option 2: physical activity-based emissions

Notes:

- Estimated emissions using energy consumption are awarded a data quality score of 2.

- Estimated emissions using production data are awarded a data quality score of 3.

Option 3: economic activity-based emissions

Notes:

- Estimated emissions using company's revenue data and sector emission factors are awarded a data quality score of 4.

- Estimated emissions using sector emission factors per unit of asset are awarded a data quality score of 5.

- Estimated emissions using sector emission factors per unit of revenue and sector asset turnover ratio are awarded a data quality score of 5.

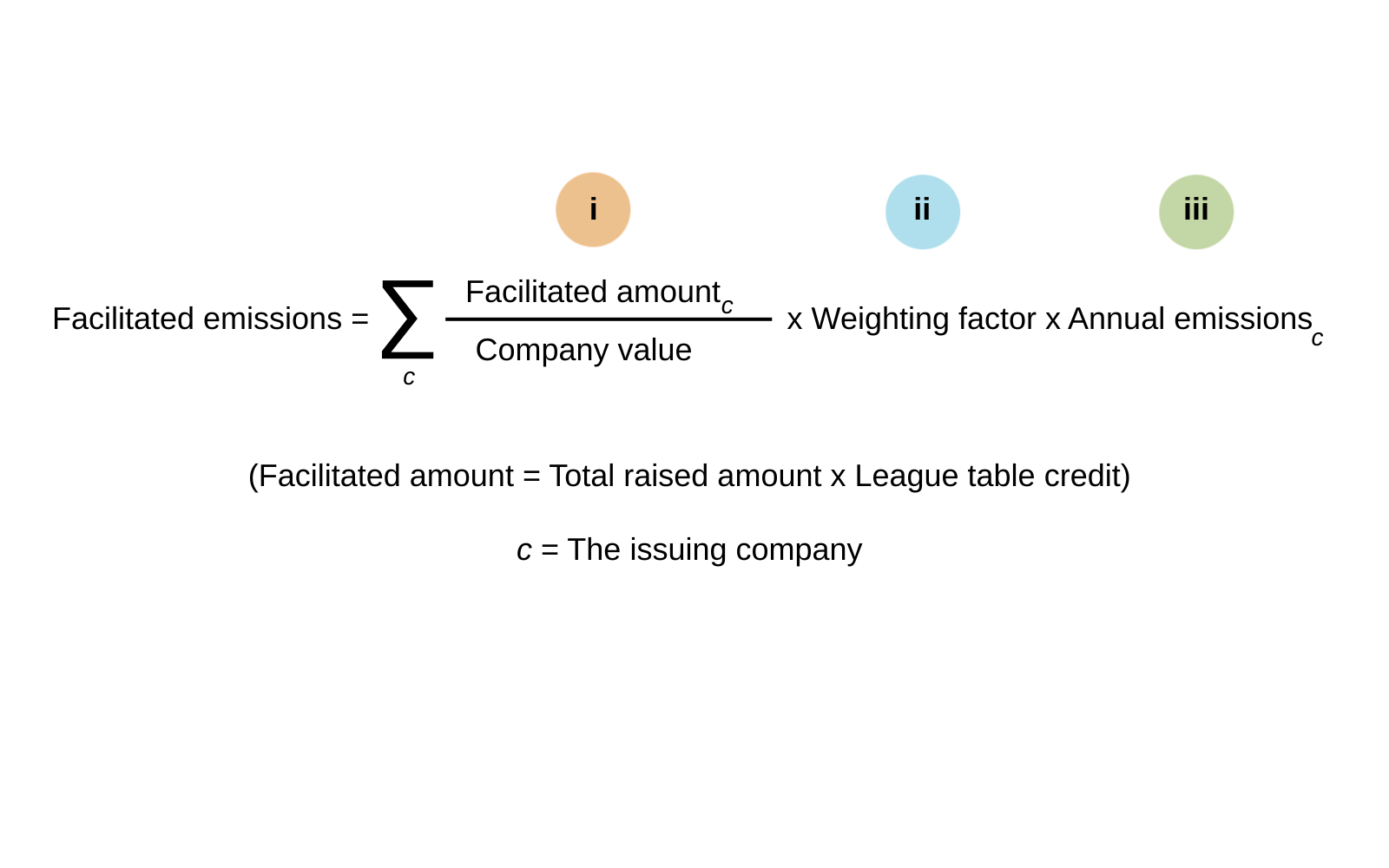

Formula for calculating facilitated emissions

Facilitated emissions from primary issuances of capital market instruments are calculated using the formula below:

The capital market transaction is accounted for in the year the facilitation occurs, using the reported or estimated annual emissions of the issuer in that year.

All the transactions during the year are then aggregated over that one year to calculate the total facilitated emissions.

Where there are multiple facilitators, emissions are split between them based on the proportion of the issuance that is attributable (by volume) to each facilitator for each transaction.

If this data is not readily available, a league table credit is used to attribute the allocation based on fees or volume. For more support you can refer to worked example (Box 5-2) on p.30 of the PCAF Facilitated Emissions Standard for the approach to calculating facilitated emissions through league table credit.

Note:

- Data quality score 5 uses estimated building energy consumption per building based on building type and location-specific statistical data and number of buildings.

Common challenges

Limited guidance

There is limited guidance available on additional financial sector activities and products that are associated with facilitating emissions. This is expected to expand in the coming years.

Moreover, currently there is no harmonized accounting standard is yet in place for facilitators of capital market transactions.

Practical considerations for assurance providers

- Be aware of upcoming changes to the PCAF facilitated emissions guidance.

- Assess whether the model is consistent with PCAF and differences are adequately disclosed.

Obtaining and sourcing data

It can be difficult to gather accurate data from various financed assets, insured assets and investments. This often involves dealing with multiple data sources and varying data quality. While larger counterparts may produce Scope 1 and 2 data, many small and medium-sized companies do not.

Practical considerations for assurance providers

- Clarity and completeness of data inputs in the model.

- Importance of walkthroughs up front – do they stack up with documented model?

- Third parties and management oversight – how are management comfortable with information from these sources?

Use of proxies and estimates

As a result of the lack of direct data available relating to certain financed assets, insured assets and investments, reporting companies frequently rely on proxies and estimates, often from third-party data providers. This can lead to inconsistencies and less reliable reporting.

There may be a time lag in data availability given that emissions data will typically be available 12-15 months after the calendar year-end. This can lead to a mismatch between financial holdings and underlying emissions.

Practical considerations for assurance providers

- Ensure hierarchy of data, proxies and estimates are adequately disclosed in the model.

- Clarity of estimation uncertainty in model and disclosures.

- Clarity of data quality in model and disclosures.

Scope 3 reporting

Reporting of Scope 3 emissions is phased-in depending on the sector in which they are active, ie, where they earn revenues over time.

There is an inherent degree of double counting that is assumed in carbon accounting. Because financial services firms are typically exposed to a broad range of sectors and companies, including scope 3 of financed emissions can introduce a much higher degree of double counting.

Practical considerations for assurance providers

- Difficulty in understanding and interpreting scope 3 of financed emission, particularly “scope 3 of 3” disclosures.

Consistency and comparability

Ensuring that the presentation of emissions data is consistent and comparable across different reporting periods and entities is a significant challenge. Given the evolving standards relating to Scope 3 emissions, prior year adjustments and re-baselining exercises are often required. There is also the challenge of assessing how material prior-year errors and adjustments are and whether these need to be re-reported or not.

Given the multiple different data inputs and variables in financed emissions calculations, it can be difficult to understand whether movements are due to portfolio decisions, movements in financial data, improving data quality or other factors.

These challenges need to be appropriately navigated by reporting companies such that assurance practitioners are able to reach a conclusion on the data.

ISAE 3000 (Revised) is the typical assurance standard under which sustainability-related assurance is obtained at present, with ISAE 3410 the standard for assurance engagements on greenhouse-gas statements.

However, the International Standard on Sustainability Assurance (ISSA 5000) is effective for assurance engagements on sustainability information reported for periods beginning on or after 15 December 2026; or as at a specific date on or after 15 December 2026.

This will see ISAE 3000 (Revised) and ISAE 3410 withdrawn, and no longer applicable for sustainability assurance engagements after that effective date.

Many firms may already be in the process of updating methodology so that they can deliver assurance engagements under ISSA 5000.

The UK version of the standard, ISSA (UK) 5000, was published by the FRC in November 2025, and, as with the international version of the standard, early adoption of ISSA 5000 is permitted – IAASB encourage this, and ICAEW is supportive.

Guidance created with permission from PCAF

This guidance is based, with permission, upon the work of the Partnership for Carbon Accounting Financials (PCAF) including the data quality score tables from The Global GHG Accounting and Reporting Standard for the Financial Industry. Any discussion of implementation challenges, lessons learned, interpretations, or other commentary are the views and experiences of contributors and not those of PCAF. Please refer to the PCAF Standard for complete guidance. In the event of any inconsistency between the guidance and the PCAF standard, the standard should be considered the authoritative source and take precedence.

More support

Read more case studies and a list of common challenges facing financial services organisations when reporting and assuring scope 3 emissions.

Case studiesChallenges