Guidance for CFOs and audit committees on reporting and assuring scope 3 greenhouse gas emissions related to life insurance. Find out about methods of estimating emissions and common challenges.

ICAEW's Financial Services Faculty has worked with members from within the sector and experts from the Partnership for Carbon Accounting Financials (PCAF) to outline estimation methodologies for those reporting and assuring on greenhouse-gas emissions relating to life insurance.

The life insurance industry is a global sector primarily focused on providing financial protection through products like life insurance, annuities, and pension plans. These products offer financial support to policyholders in the event of unforeseen life events such as death, disability, or retirement. The industry also functions as a significant institutional investor, managing large portfolios that include equities, bonds, real estate, and other asset classes.

Material elements of scope 3

Typically, there would be disaggregation into the assets (the investments held by the insurer to back the liabilities to policyholders) and the liabilities.

To date, we are not aware of any widely-used examples of estimating the emissions associated with the liability side of a life insurer – this would require modelling the emissions of an individual life, and then attributing a proportion of that to the relevant insurer.

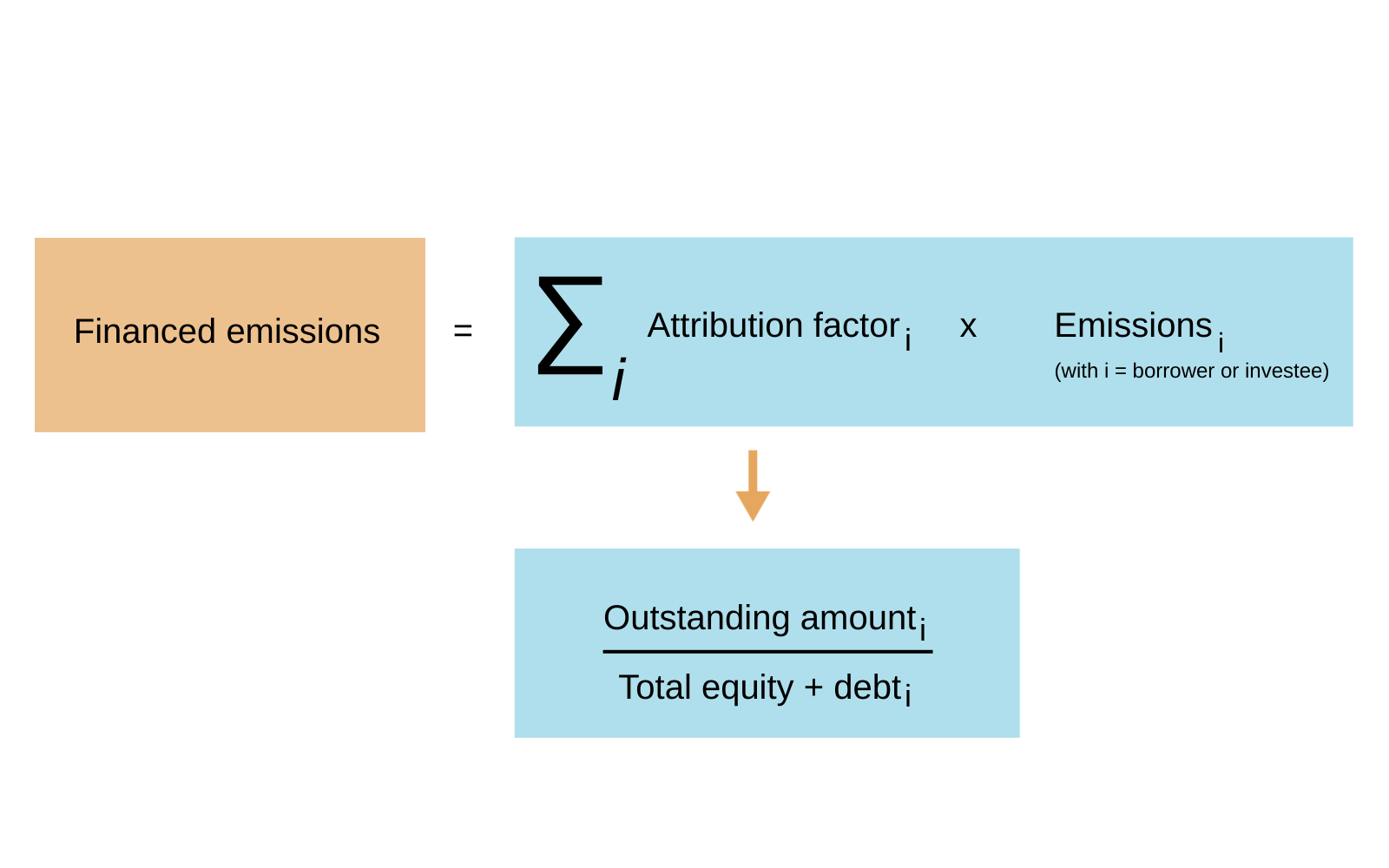

There are significantly more examples of estimating emissions for the assets – typically following the Partnership for Carbon Accounting Financials (PCAF) framework for investment emissions (or financed emissions). We typically see organisations build these on an asset class basis (eg, listed equity and debt, real estate, sovereign debt, private assets).

Calculation methodology

Organisations should refer to the guidance available in the PCAF Standard (Part A) which provides overarching principles and specific guidance by asset class.

Key source: PCAF Standard Part A - The Global GHG Accounting and Reporting Standard for the Financial Industry

Typically, organisations disclose absolute financed emissions, financed emissions intensity (the absolute number divided by the amount invested) and a PCAF data quality score. It is also common to provide the weighted average carbon intensity or WACI which demonstrates a portfolio’s exposure to carbon-intensive industries.

Reliance on third-party data vendors - report data

Typically reporting organisations rely on a data vendor (or vendors) to provide investee level data (both financial data such as revenue and EVIC, and non- financial data such as emissions). There is limited visibility as to how data vendors have extracted/determined these amounts based on public company reporting, including adjustments that the vendor may make over and above what has been reported.

Practical considerations for assurance providers

- It is challenging for assurance practitioners to perform testing over reported data. The results of testing usually show differences, which require follow up and engagement with the data provider to understand whether the differences represent misstatements.

- There is no controls report / shared assurance comfort in place over the major data vendors.

- It is often difficult to obtain underlying evidence or perform even a basic ‘sense check’ on the completeness of Scope 3 data.

- When an asset class contains a mix of actual and estimated data, and completeness is uncertain, there is discretion as to how the estimated portion should be treated.

- Without a clear understanding of the full population, it may not be possible to reach a clean or even qualified conclusion.

- In some cases, the level of uncertainty may warrant the use of a disclaimer rather than a conclusion.

- While data quality scores may partially reflect this uncertainty, there is a need for clearer guidance to support preparers and reviewers in navigating these grey areas.

Reliance on third-party data vendors - modelled data

Where public reporting is not available or is not reliable for a particular investee, data vendors will use their proprietary model to estimate an emissions value. There is limited visibility over the specific methodologies and data inputs used by vendors to determine these values.

Practical considerations for assurance providers

- It is challenging for assurance practitioners to design appropriate tests and to challenge the accuracy of estimates prepared by data vendors.

- There is no controls report / shared assurance comfort in place over the major data vendors.

Time lag for investee level emissions data

Given the publication timeframe for investee level emissions, there is usually at least a one-year time lag between the reporting of an individual issuer and the reporting of the life insurer that holds the asset. This can lead to a mismatch between financial holdings and underlying emissions.

Manual and complex processes

Scope 3 calculations are often highly manual and complex, requiring diverse data inputs from across the value chain, which are not always readily available or reliable. This process is not only time-intensive but also prone to error. Manual processes, especially for non-liquid assets.

Manual processes are particularly more prevalent in more illiquid asset classes (for example, infrastructure, private debt), data is gathered and calculations are performed in spreadsheets. This reflects the generally more manual and less systemised control environment for these asset classes.

Practical considerations for assurance providers

- Manual processes and use of spreadsheets with complex formulae introduce additional risks of error and inaccuracy.

Consistency and comparability

Ensuring that the presentation of emissions data is consistent and comparable across different reporting periods and entities is a significant challenge. Given the evolving standards relating to Scope 3 emissions, prior year adjustments and re-baselining exercises are often required. There is also the challenge of assessing how material prior-year errors and adjustments are and whether these need to be re-reported or not.

Given the multiple different data inputs and variables in financed emissions calculations, it can be difficult to understand whether movements are due to portfolio decisions, movements in financial data, improving data quality or other factors.

Scope 3 reporting

Reporting of Scope 3 emissions is phased-in depending on the sector in which they are active, ie, where they earn revenues over time.

There is an inherent degree of double counting that is assumed in carbon accounting. Because financial services firms are typically exposed to a broad range of sectors and companies, including scope 3 of financed emissions can introduce a much higher degree of double counting.

Practical considerations for assurance providers

- Difficulty in understanding and interpreting scope 3 of financed emission, particularly “scope 3 of 3” disclosures.

Regular changes mean restatements

Regular changes to methodologies and data sources are leading to a high number of restatements. The reporting of financed emissions is immature and is changing at pace – this can lead to a relatively high incidence of restatement or rebaselining.

Practical considerations for assurance providers

- Can reduce confidence in and usefulness of information to stakeholders.

Guidance created with permission from PCAF

This guidance is based, with permission, upon the work of the Partnership for Carbon Accounting Financials (PCAF) including the data quality score tables from The Global GHG Accounting and Reporting Standard for the Financial Industry. Any discussion of implementation challenges, lessons learned, interpretations, or other commentary are the views and experiences of contributors and not those of PCAF. Please refer to the PCAF Standard for complete guidance. In the event of any inconsistency between the guidance and the PCAF standard, the standard should be considered the authoritative source and take precedence.

More support

Read more case studies and a list of common challenges facing financial services organisations when reporting and assuring scope 3 emissions.

Case studiesChallenges