This is before taking account of the government’s decision to freeze repayment thresholds over the next three years, which should reduce the impairment to 38%.

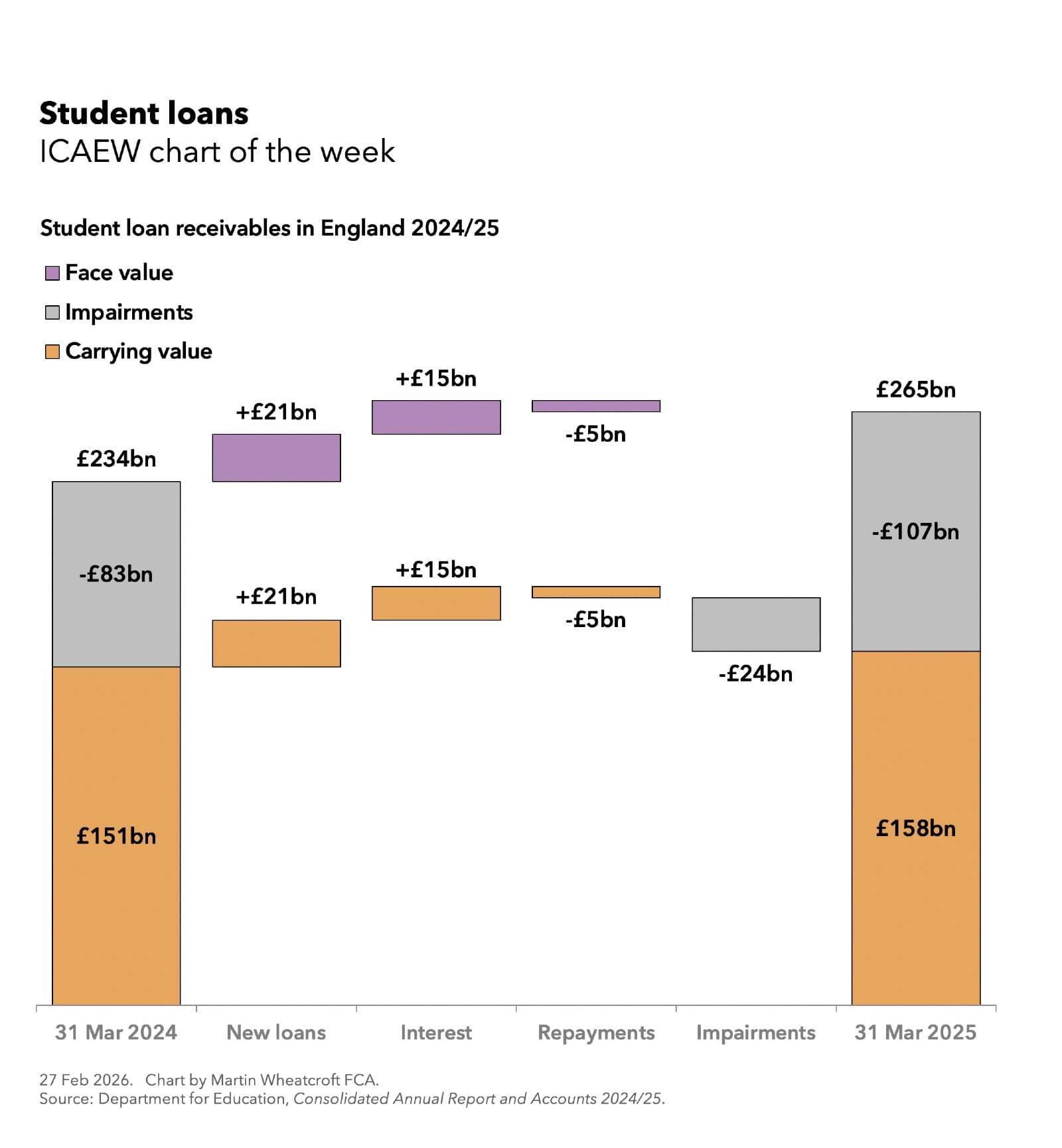

According to the Department for Education’s consolidated annual report and accounts 2024/25, the face value of student loans in England increased from £234bn to £265bn during the year ended 31 March 2025. The movements comprised £21bn in new loans advanced to students during the year and £15bn of added interest less £5bn in repayments.

As our chart also illustrates, the carrying value in the department’s balance sheet increased from £151bn to £158bn, once an impairment of £24bn during the year is taken into account – increasing the cumulative impairment from £83bn to £107bn.

This is an increase in the impairment percentage from approximately 35% on 31 March 2024 to 40% on 31 March 2025 based on the fair value of the student loan portfolio calculated by the department.

The £24bn impairment can be analysed between an immediate £6bn impairment on the inception of new loans issued during the year (approximately 30% of their face value) and £18bn from the recalculation of the fair value of loans at the end of the financial year, more than offsetting the interest added to the loans.

The loan portfolio can be broken down between Plan 1 loans for undergraduate courses that started before 1 September 2012 (face value £28bn less £14bn cumulative impairment = fair value £12bn on 31 March 2025), Plan 2 loans for undergraduate courses between 2012 and 31 August 2023 (£216bn - £87bn = £129bn), Plan 3 loans for postgraduates (£7bn - £1bn = £6bn) and Plan 5 loans for undergraduate courses starting from 1 September 2023 onwards (£14bn - £3bn = £11bn).

The recent controversy around student loans has been around the interest rates charged on student loans, and in particular those of Plan 2 loans owed by the majority of former students, which are based on RPI + 3%. In the year from 1 September 2025 the interest rate is 6.2% for those earning £51,245 (£4,270 a month) or more reducing to 3.2% for those earning £28,470 (£2,372 a month) or less.

This often means that the balance outstanding grows by more than the amount repaid. For example, someone earning £42,000 (£3,500 a month) with Plan 2 student loans totalling £50,000 on 1 September 2025 would see £2,490 (at an interest rate fractionally under 5%) added to their loan over the year to 31 August 2026. As their repayments would be equal to approximately £1,220 (being 9% on their earnings above the Plan 2 threshold of £28,470) their debt would rise to £51,270.

Most current undergraduates are under Plan 5, which has a flat interest rate of RPI irrespective on income but a lower £25,000 repayment threshold which could see them pay a lot more over their 40-year terms than those on the 30-year Plan 2 loans. In our example, a graduate on £42,000 a year with £50,000 in Plan 5 loans brought forward would see £1,600 added in interest and repay £1,530 to result in a much smaller increase in their outstanding loan balance.

With the government suggesting that they are going to have another look at the way student loans are designed, many graduates will be hoping that reform is the air.

Explainer: How student loans work

ICAEW’s Tax Faculty explains the scale of student debt, the different types of student loan plan and how repayments are calculated and made.

Latest charts

Further resources

ICAEW Community

Public Sector Community

The go-to place for guidance on issues affecting finance professionals working in and with the public sector. With a range of dynamic services, ICAEW provides valuable tools, resources and support tailored to the public sector.

Resources

Economy explainers

ICAEW experts offer simple guides to help understand the technical, economic jargon that is discussed when talking about public finances and the economy.

Find out moreICAEW support

Training and events

Browse upcoming and on-demand ICAEW events and webinars offering support on technical areas, such as assurance, reporting and tax, as well as personal development.

Events and webinars A-Z of courses