The OBR published its latest forecast evaluation report on 2 June 2026, analysing the differences between its five-year, two-year and one-year fiscal deficit forecasts and the outturn for the year ended 31 March 2025 (2024/25).

Our chart illustrates the OBR’s evaluation of its one-year fiscal forecast published in March 2024 alongside that year’s Spring Budget, a few months before the general election in July 2024.

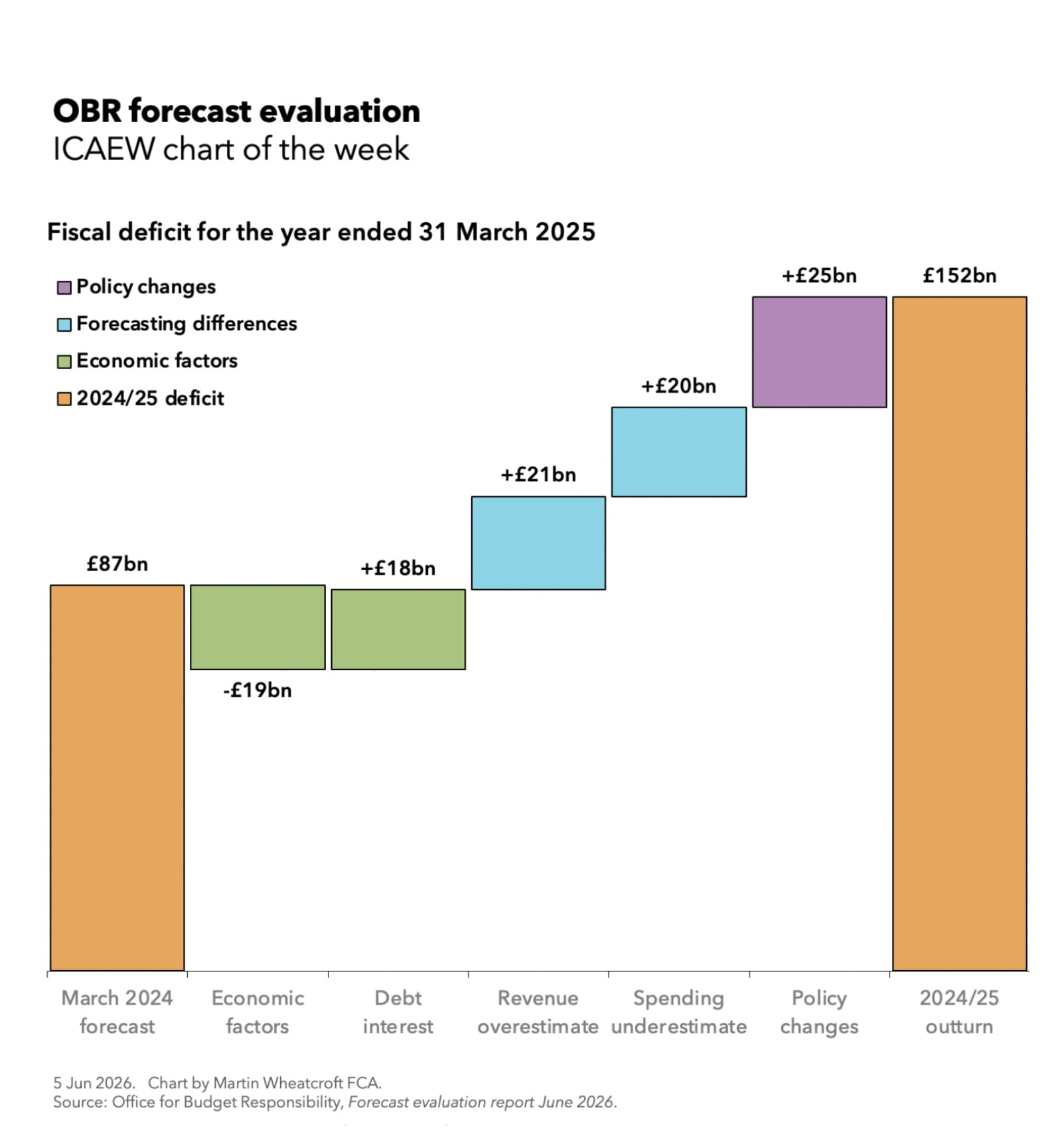

As our chart shows, the OBR forecast a deficit of £87bn for the 2024/25 financial year. Economic factors increased receipts and reduced the deficit by £19bn but this was mostly offset by higher debt interest costs of £18bn. After adjusting for differences in these core economic assumptions, the OBR concluded that their revenue forecast was overestimated by £21bn and their spending forecast was underestimated by £20bn, with policy changes – principally by the incoming Labour government – adding a further £25bn to the deficit.

The outturn deficit of £152bn was 75% higher than forecast, a significant difference given that the forecast was prepared a couple of months before the start of the financial year concerned.

About the forecast differences

According to the OBR’s analysis, the £19bn difference from economic factors comprised £13bn from higher than forecast nominal earnings and employment boosting income tax and national insurance contributions, £2bn from higher corporate profits boosting corporation tax, and £6bn from other economic factors increasing investment income and stamp duty receipts, less £1bn from slightly lower consumption affecting VAT receipts and £1bn from rounding.

The £18bn in higher debt interest charges mainly reflected economic factors too, with higher inflation adding £10bn to the cost of inflation-linked gilts and interest rates reducing at a slower pace than forecast adding £3bn to interest payments and £5bn to the cost of unwinding quantitative easing.

The revenue overestimate of £21bn consisted of £7bn in lower income tax and national insurance receipts (principally from weaker income tax self-assessment receipts than expected), £9bn in lower corporation tax receipts (principally from lower taxable profits for small companies than expected), £1bn from less alcohol and tobacco consumption, £1bn from weaker than expected capital gains, and £3bn less than expected across a range of other receipts.

The spending underestimate of £20bn comprises £6bn from overestimating how much government departments would underspend their capital budgets, £5bn from underestimating central government current grants, £3bn from a miscalculation on social housing subsidies, £1bn from higher welfare payments, £4bn on local government current spending, and £1bn in other forecast differences.

Policy changes of £25bn comprise £26bn in spending increases less £1bn from tax compliance measures announced in the Autumn Budget 2024, Labour’s first Budget following the general election. The former reflects increases to departmental budgets to cover the so-called £22bn ‘black hole’ of unfunded net spending pressures identified by the incoming Labour government in the summer of 2024, including £10bn of pressures that were known about by HM Treasury at the time but the OBR were not notified of before they prepared the March 2024 forecast. See the OBR’s review of the March 2024 forecast for department expenditure limits for more detail.

Two- and five-year forecasts

The OBR fiscal evaluation report also looks at the differences between the outturn of £153bn and its March 2023 two-year forecast for a deficit of £85bn in 2024/25 and its July 2020 five-year forecast for a deficit of £116bn in 2024/25.

The OBR did not attempt to review its pre-pandemic March 2020 forecast of a £58bn deficit in 2024/25 given the huge impact that the pandemic had on the public finances that was not known about at that time.

Reality has been disappointing, but so has the forecasting

The OBR’s forecast evaluation report concludes with a section titled ‘Refining our forecasts’, setting out how the OBR could do better in its forecasting.

It is of course pretty difficult to forecast the fiscal deficit accurately, even over a period as short as a year. The deficit is the difference between two very large numbers (£1,139bn receipts and £1,291bn spending in 2024/25), both of which can change significantly depending on inflation, interest rates and economic circumstances even before considering the quality of the forecasting process. The OBR also can’t (for obvious reasons) incorporate policy changes that have not yet been decided on, especially following a change in government.

While economic developments and changes in government policy have been major contributors to the differences between the OBR’s previous forecasts and the outturn for 2024/25, the OBR acknowledges that it could have done better in its forecasting, especially in its two- and one-year forecasts.

For example, it accepts that it underestimated the second-round effects of the 2022 energy shock on inflation, which they assumed would add 25% on top of the direct effect of higher energy prices, but which ended up adding close to 50%. The OBR also failed to reflect the impact the energy shock had on household savings and consumption, on wages over subsequent years, and the level of reduction in business output affected by higher energy costs.

The OBR also concludes that it needs to revise its business investment modelling (a key input into forecasting productivity), expand its use of scenario analysis and how it communicates risks around its central forecast, split out smaller companies from larger companies in how it projects profits and corporation tax receipts, and make further refinements in how it forecasts inflation, interest rates and demographic change.

Data quality and complexity is also a major issue

More concerning are the issues identified with the quality and complexity of the underlying financial information the OBR uses to prepare its forecasts.

In the case of 2024/25, this included information about spending pressures that was not shared with the OBR before the forecast was put together, as well as the requirement to take the government’s spending plans as read. This led to a recommendation for the OBR to be explicitly allowed to forecast overspends in department expenditure limits in addition to forecasting underspends.

Other recommendations include the government providing the OBR with a more detailed department-by-department analysis of risks to spending plans, how central budget reserves are allocated and utilised, and permitting the OBR to speak directly to departmental CFOs.

The OBR identifies issues in the quality of the data it receives on local government finances, and a Local Government Financial Information Taskforce has been established to improve this. It is also looking at the link between unemployment statistics and welfare claims processed by the Department for Work & Pensions (DWP), as well as the quality of the evidence supporting the forecasting of incapacity claims.

Finally, the OBR highlights how a significant element of its near-term forecast errors are explained by underestimates of National Accounts adjustments. These are entries made between the underlying accounting records on a resource accounting basis to reach the national accounts fiscal numbers that the OBR is attempting to forecast.

This highlights a fundamental problem in the use of four different accounting frameworks by the government – accruals-based IFRS for financial statements at all levels of government, hybrid-accruals resource accounting for central government departmental budgeting and financial performance monitoring, hybrid-accruals statutory override adjusted accounting for local government budgeting and financial performance monitoring, and statistical-based national accounts measures for fiscal targets and budgeting at the national level. This means there is no clear line of sight between the fiscal numbers that the OBR are trying to forecast, the numbers used internally by government departments and local authorities, and the numbers reported in public sector financial statements.

In some ways it is perhaps unsurprising that the OBR struggles to forecast the future given the challenges it faces in getting the high-quality data it needs, even before trying to deal with economic and fiscal policy uncertainty!

Latest charts

Further resources

ICAEW Community

Public Sector Community

The go-to place for guidance on issues affecting finance professionals working in and with the public sector. With a range of dynamic services, ICAEW provides valuable tools, resources and support tailored to the public sector.

Resources

Economy explainers

ICAEW experts offer simple guides to help understand the technical, economic jargon that is discussed when talking about public finances and the economy.

Find out moreICAEW support

Training and events

Browse upcoming and on-demand ICAEW events and webinars offering support on technical areas, such as assurance, reporting and tax, as well as personal development.

Events and webinars A-Z of courses