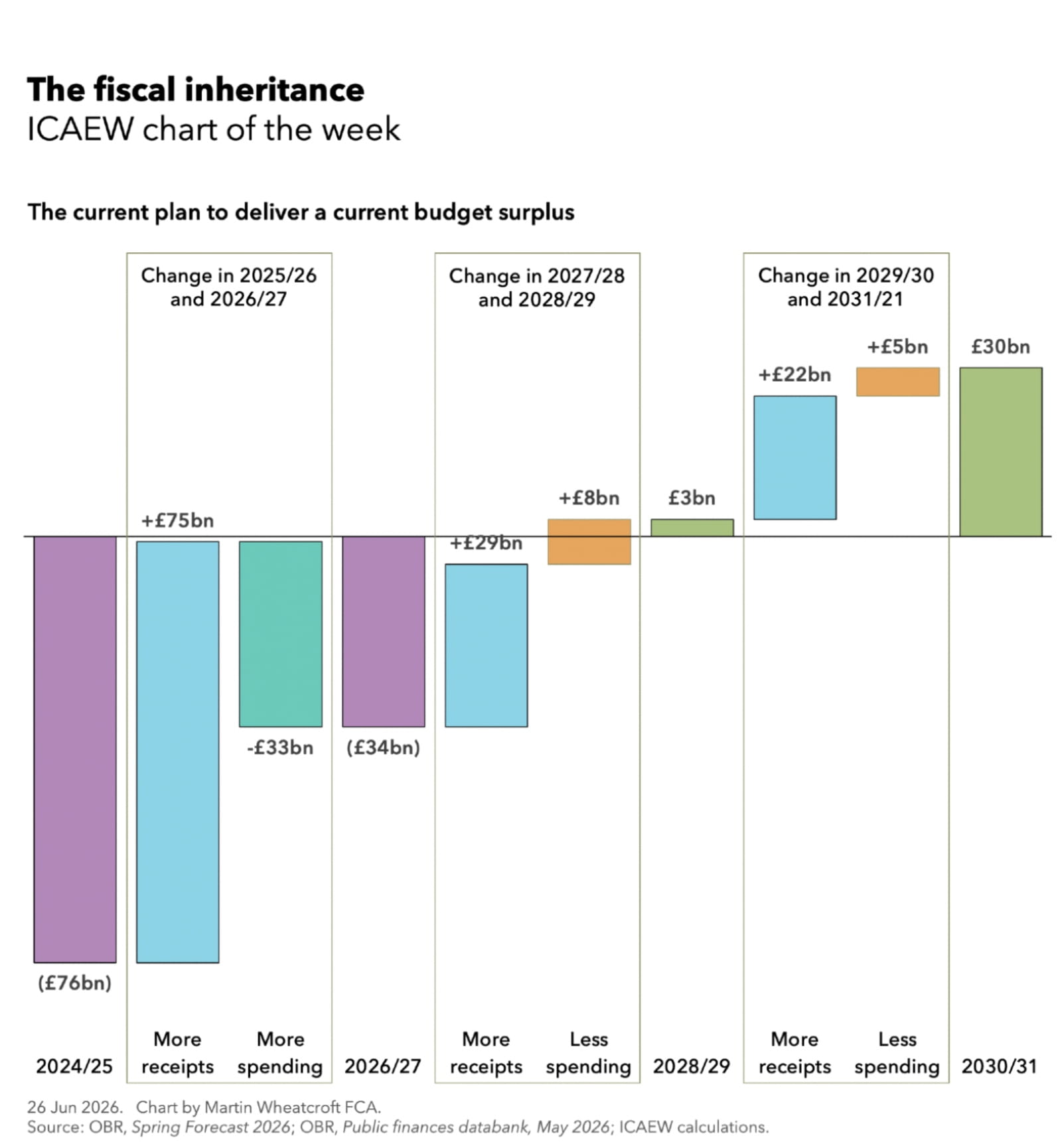

The current plan to deliver a current budget surplus

According to the Office for Budget Responsibility (OBR)’s Spring Forecast 2026, the government is planning to turn the current budget balance from a deficit of £76bn in 2024/25 to a budgeted deficit of £34bn in the current fiscal year, a surplus of £3bn in 2028/29 and a surplus of £30bn in 2030/31.

The current budget balance is equal to tax and other receipts less day-to-day spending, which by definition excludes net investment. (The overall deficit including net investment was £151bn in 2024/25, is budgeted to be £115bn in 2026/27, and is forecast to be £86bn in 2028/29 and £59bn in 2030/31.)

The planned swing of £106bn a year in the difference between annual receipts and annual current spending from negative £76bn in 2024/25 to positive £30bn six years later is highly ambitious at a time when economic growth is weak, spending pressures are rising and the public finances are exposed to adverse shocks.

The base year in our chart is the year ended 31 March 2025, the financial year during which the government changed.

2025/26 and 2026/27

The Chancellor’s first Budget in October 2024 involved significant tax rises coming into force from April 2025, in particular a substantial rise in employer national insurance.

- Further tax rises were announced in her first Spring Statement in March 2025 and in her second Budget in November 2025, although several are scheduled to come into force in later years. Freezing tax allowances also means there is fiscal drag causing tax receipts to rise at faster rate than the underlying income that is being taxed.

- Combined with other structural features of the tax system that cause tax receipts to rise at a faster or slower rate than the economy and rising investment income, the result is an increase in receipts of £75bn over and above the growth in nominal GDP in 2025/26 and 2026/27 (the latter on a budgeted basis).

- Of this, £47bn was delivered in the last financial year ended 31 March 2026 (based on provisional outturn numbers) and £28bn is budgeted to be delivered in the current financial year to 31 March 2027.

- Not all of this increase was used to improve the bottom line, with current spending going up by £33bn over and above growth in the economy: £18bn in the last financial year and a budgeted increase of £13bn this year.

- The extra spending reflects significant increases in departmental budgets in 2025/26 and in 2026/27 (the first year of the three-year spending review period), the rising cost of debt interest, and higher state pension and welfare payments among other factors.

2027/28 and 2028/29

A further fiscal consolidation is expected to occur in 2027/28, the middle year of the current spending review period.

- There are £25bn more receipts pencilled into the fiscal forecasts out of the £29bn two-year total shown in our chart.

- The government is hoping to bring down public spending by £8bn when compared with growth in the economy over the last two years of the spending review, with £4bn less in 2027/28 and £4bn less in 2028/29.

- These reductions in spending will still be advertised as large increases in cash terms. However, growing spending on pensions and welfare as more people live longer, together with inflation, salary rises and supplier price rises, will absorb much of the incremental cash increase. This will result in very tight operating budgets for most government departments and require significant efficiency savings, including headcount reductions.

If delivered, these plans should turn the current budget balance from a budgeted deficit of £34bn this year to a forecast surplus of £3bn in 2028/29, a year ahead of the Chancellor’s primary fiscal rule.

2029/30 and 2030/31

The next two years of the plan are more provisional, pending the spending review in 2027 that will revise departmental budgets for 2028/29 (the last year of the current spending review, which becomes the first year of the following review) and set departmental budgets for 2029/30 and 2030/31.

- The plan then relies on £22bn of additional receipts in 2029/30 and 2030/31, together with £5bn of lower spending over the two years relative to economic growth, to arrive at a current budget surplus of £30bn in 2030/31.

- This is split between a £21bn planned improvement in 2029/30 (£16bn more receipts and £5bn less spending) and a £6bn planned improvement in 2030/31 (£6bn more receipts and spending rising in line with growth in the projected size of the economy).

- This current fiscal rule test year of 2029/30 – the fourth year of the fiscal forecast where the current budget surplus is projected to be £24bn – will remain the test year at Budget 2026 in the autumn, when it will be the third year of the next fiscal forecast (after which it will roll forward by a year each time at future Budgets from 2027 onwards).

A challenging inheritance

The incoming prime minister and chancellor will inherit a fiscal plan that already looks difficult to achieve, with spending pressures mounting and the current budget deficit £6bn over budget in the first two months of the financial year.

- The plan depends on substantial tax rises and spending restraint over the rest of the forecast period, based on economic assumptions set before the conflict with Iran.

- The most immediate risks are defence, health, pensions and welfare, inflation and interest rates, and the repeated difficulty of turning planned efficiency savings into lower overall spending.

- At the same time, political pressure to fund priorities such as student loan reform will make the consolidation harder to deliver.

It's all about growth

Boosting the economy is therefore likely to be the main focus of the incoming PM.

Not because slightly stronger growth would solve the fundamental weaknesses facing the public finances – which will require a more comprehensive long-fiscal strategy to resolve – but because a relatively small amount of extra money would make life so much easier.

Sir Keir Starmer discovered this to his cost when he lost his Defence Secretary over just a couple of billion quid a year.

The risk is that the OBR’s autumn numbers may be worse than the Spring Forecast 2026 projections, reflecting energy prices, inflation, debt interest, lower net migration, and possible adverse economic effects from employment and landlord reforms coming into force this year.

However, there is a potential upside if the government’s reforms to planning, infrastructure, housing, welfare, skills, energy costs, AI and net zero start to boost economic activity later in the forecast period.

The concern is that the country could again face three or four months of uncertainty ahead of the Budget this autumn, causing businesses to again hold back on investment and paralysis in government. Let’s hope the incoming PM and chancellor can avoid a repeat this time around.

Latest charts

Further resources

ICAEW Community

Public Sector Community

The go-to place for guidance on issues affecting finance professionals working in and with the public sector. With a range of dynamic services, ICAEW provides valuable tools, resources and support tailored to the public sector.

Resources

Economy explainers

ICAEW experts offer simple guides to help understand the technical, economic jargon that is discussed when talking about public finances and the economy.

Find out moreICAEW support

Training and events

Browse upcoming and on-demand ICAEW events and webinars offering support on technical areas, such as assurance, reporting and tax, as well as personal development.

Events and webinars A-Z of courses