Although the Budget itself may have been delayed, the IFS Green Budget 2020 has been published on schedule, with a wealth (if that is the right word in the current context) of analysis on the economy and the public finances.

With £201bn in discretionary measures and a £95bn economic impact from the coronavirus pandemic, the IFS is forecasting that the deficit will reach £350bn in the current financial year. At 17% of GDP, this is a level never before seen in the UK outside of the two world wars.

Unfortunately, the effect of the pandemic on public finances will not be restricted to this financial year. Even if the economy recovers in 2021, or more likely in 2022, tax revenues will be significantly lower and spending significantly higher than they were previously expected to be.

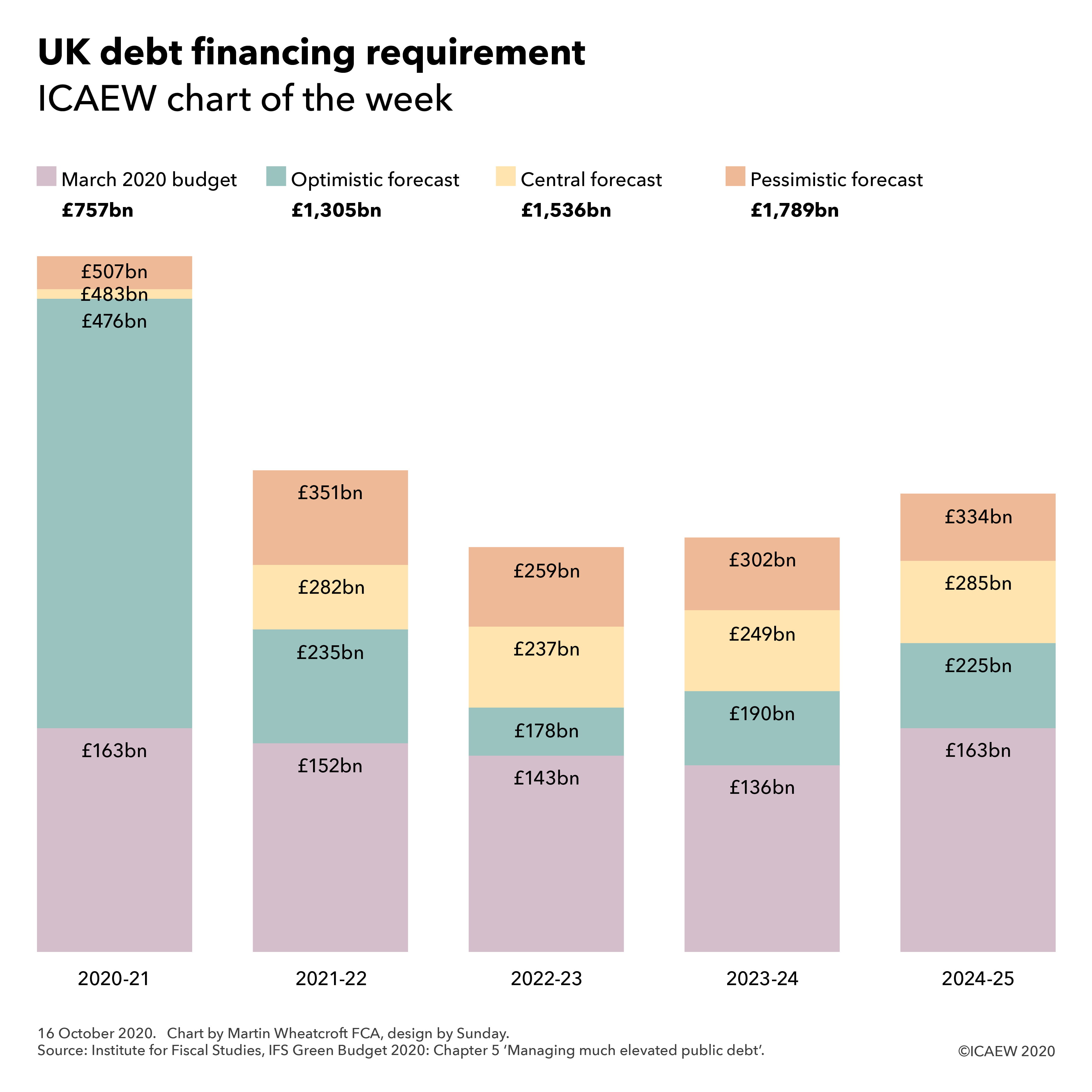

This is perhaps best highlighted by looking at the UK Government’s gross financing requirement – the amount that the UK Debt Management Office (DMO) will be tasked with raising from external debt investors over the next five years to finance the shortfall in taxes compared with spending (the deficit), to finance business and other lending and to repay existing debts as they fall due. This is forecast by the IFS to double to £1.5tn in their central forecast, within a range from £1.3tn in a more optimistic scenario to £1.8tn in a more pessimistic scenario.

As the IFS points out, the enormous amount of debt being issued means that even small differences in financing costs will have a very large impact on the public finances. This is despite the sizeable proportion of debt being issued with long maturities (as long as 50 years in some case) that are locking in extremely low interest rates for decades to come.

Reducing interest costs on debt has provided the Chancellor with room to provide the unprecedented levels of financial support to the UK economy that we saw over the summer. The prospect of negative nominal rates could see investors paying the Government rather than the other way round, providing headroom for further interventions.

There is a downside, of course. The ‘good times’ of ultra-low interest rates may not last for ever, and with a central debt forecast at 31 March 2025 of 112% of GDP significantly higher than the 35% of GDP before the financial crisis a dozen years ago the exposure to changes in interests is that much more significant.

To find out more about the latest forecasts for the economy and the impact that will have on the public finances, please do read the IFS Green Budget 2020.