The Balanced Scorecard is a framework used for clustering business objectives, measures and targets under four perspectives.

The following BPM tool guide is one of a series produced for ICAEW by Professor Mike Bourne of Cranfield University.

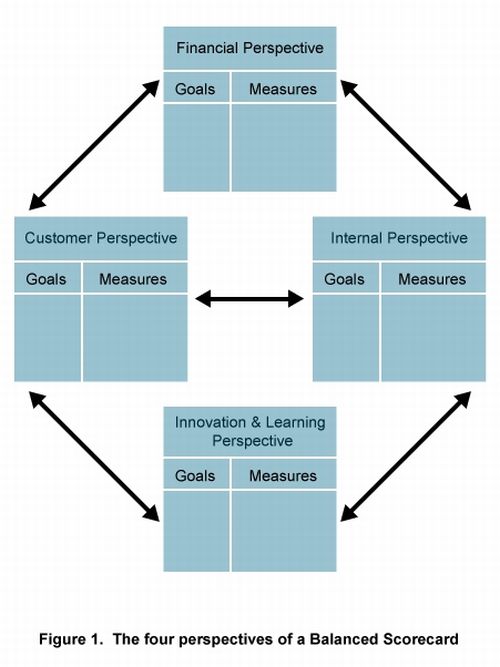

The traditional four perspectives are: -

It is useful to think about these four perspectives through the following questions: -

The format of the Balanced Scorecard is usually depicted as in figure 1.

Background to the Balanced Scorecard

The first “Balanced Scorecard” was developed and used to manage Analog Devices in the USA by Art Schneiderman back in the late 1980s. Whilst he was teaching at Harvard Business School it was taken on by Robert Kaplan and David Norton who ran a research project around the scorecard before publishing their seminal 1992 article in Harvard Business Review.

The idea behind the Balanced Scorecard is that it forces the organisation to look at other perspectives and not just focus on the financial results. It was developed at a time when management accounting was being criticised as not being relevant for managing an enterprise. Besides the reporting and control issues, it was argued that it was too easy to manipulate the short term financial measures in large organisations to present good financial results whilst undermining the long term competitiveness of the business. For example: -

Balanced Scorecard practice

Usage of the Balanced Scorecard has risen and fallen over the years. Most organisations have KPIs (Key Performance Indicators), but many don’t group them into the four scorecard perspectives.

Some organisations found that four perspectives are too limiting, so there have been many five perspective scorecards. For example, ABB (‘global leader in power and automation technologies’) traditionally added Employees as a fifth dimension, deliberately separating employees from innovation and learning. In developing a scorecard for a builders’ merchant, we found that suppliers were too important not to have their own perspective. Similarly, this position is often taken with respect to the regulator in financial services and other regulated industries.

In many organisations the term “balanced” has been dropped and they talk about their scorecard (which may or may not be “balanced”).

Populating the Balanced Scorecard framework with existing measures taken from your organisation is a very prevalent and bad practice. The Balanced Scorecard is supposed to represent the strategy of your company, not just a balance of measures. So creating an effective Balanced Scorecard takes time and effort and requires senior management engagement and support. This lack of attention in many organisations has given the Balanced Scorecard a bad name.

Increasingly scorecards are being automated with RAG (Red Amber Green) traffic lights being used on the key measures. This can reduce administration time, but often means the scorecard is not scrutinised in depth.

The four perspective presentation of the scorecard is being overtaken by the use of Strategy and Success maps which people believe are more useful for depicting strategy. However, from my experience the use of Strategy and Success maps is still not as widespread as I would expect in organisations.

Benefits of a Balanced Scorecard

The balanced scorecard has a number of benefits: -

Issues and pitfalls to be avoided

There are a number of issues to be aware of when adopting a Balanced Scorecard; -

Bibliography

Further guidance

- Balanced Scorecard ICAEW resources

- Special report: Balanced Scorecard

- About the Balanced Scorecard

More support on business

Read our articles, eBooks, reports and guides on Business Performance Management

BPM hubTools, templates and case studiesCan't find what you're looking for?

The ICAEW Library can give you the right information from trustworthy, professional sources that aren't freely available online. Contact us for expert help with your enquiries and research.