ICAEW’s thought leadership project ‘So what is economic success? Going beyond GDP and profit’ will explore what we mean by economic success, the role that GDP and profit play in this, and the potential for broader measures of economic success to help us balance our economic priorities, our social goals, and the constraints imposed on us by the natural environment we live in.

The diagram below maps out the questions we are considering and our brochure provides more background. The digital version of the brochure is designed for viewing on a computer or tablet.

We welcome all views on these questions and the project as a whole. Please share your thoughts with us by emailing sustainability@icaew.com.

-

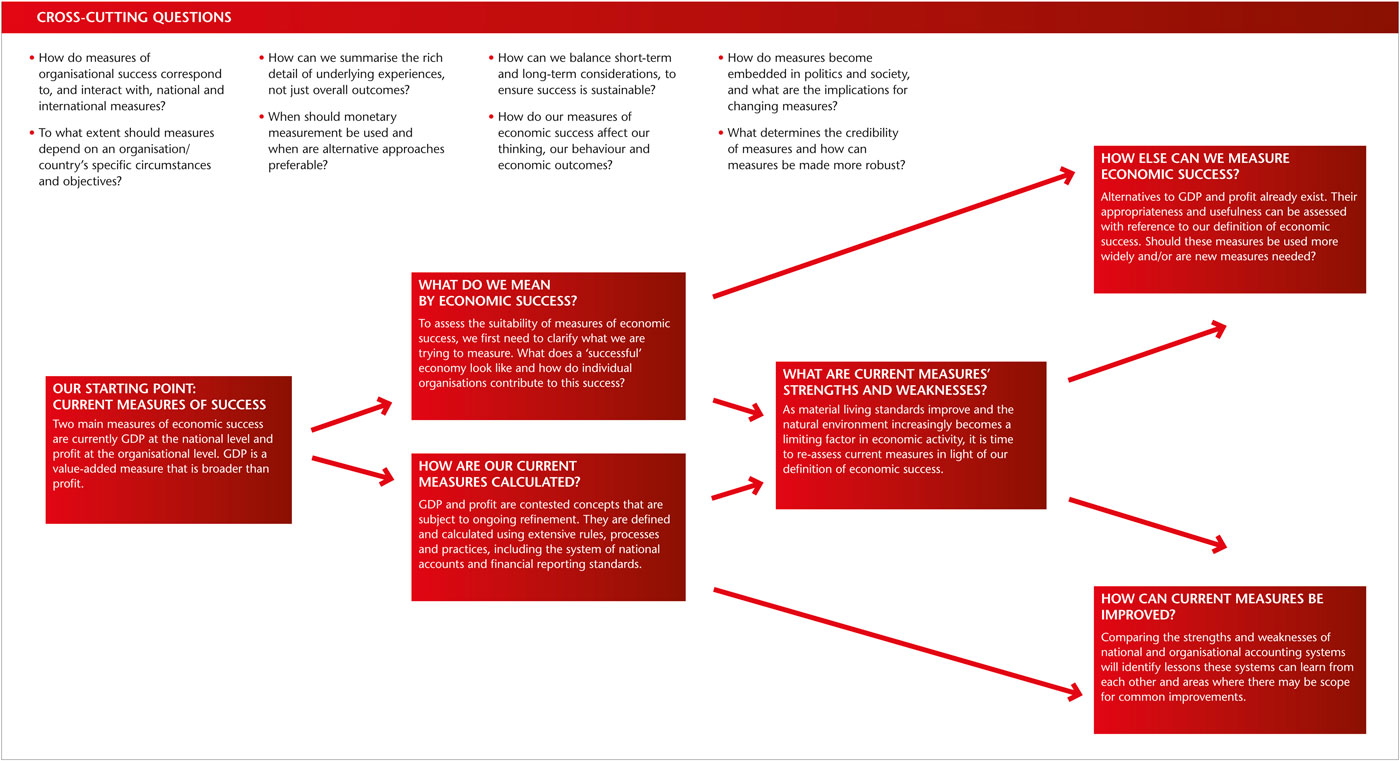

Our starting point: current measures of economic success

Two of the most-used measures of economic success are currently GDP at the national level and profit at the organisational level. GDP is a value-added measure that is broader than profit.

- Read 'Current measures of economic success'

-

What do we mean by economic success?

To assess the suitability of measures of economic success, we first need to clarify what we are trying to measure. What does a ‘successful’ economy look like and how do individual entities contribute to this success?

- Read 'What we do we mean by economic success?'

-

How are current measures of economic success calculated?

GDP and profit are contested concepts that are subject to ongoing refinement. They are defined and calculated using extensive rules, processes and practices, including the system of national accounts and financial reporting standards.

-

What are our current measures’ strengths and weaknesses?

As material living standards improve and the natural environment increasingly becomes a limiting factor in economic activity, it is time to re-assess current measures in light of our definition of economic success.

-

How can current measures of economic success be improved?

Comparing the strengths and weaknesses of national and organisational accounting systems will identify lessons these systems can learn from each other and areas where there may be scope for common improvements.

-

How else can we measure economic success?

Alternatives to GDP and profit already exist. Their appropriateness and usefulness can be assessed with reference to our definition of economic success. Should these measures be more widely used and/or are new measures needed?

-

Cross-cutting questions

Throughout the project we will be considering cross-cutting questions such as:

- How do measures of organisational success correspond to, and interact with, national and international measures?

- To what extent should measures depend on an organisation/country’s specific circumstances and objectives?

- How can we summarise the rich detail of underlying experiences, not just overall outcomes?

- When should monetary measurement be used and when are alternative approaches preferable?

- How can we balance short-term and long-term considerations, to ensure success is sustainable?

- How do our measures of economic success affect our thinking, our behaviour and economic outcomes?

- How do measures become embedded in politics and society, and what are the implications for changing measures?

- What determines the credibility of measures and how can measures be made more robust?