Q2: Business confidence in Retail & Wholesale deteriorates as the Iran War weighs on the outlook.

The latest national Business Confidence Monitor (BCM) shows that the Iran War significantly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker than expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 13 April to 19 June 2026.

- Business confidence in Retail & Wholesale fell to -14.0 from -11.0 in Q1 2026, marginally above the UK average (-14.6).

- Domestic sales growth was steady and is expected to strengthen over the coming year.

- Geopolitical risk was the most widely cited rising challenge, followed by labour costs, energy costs and the tax burden.

- Employment continued to recover, while pay growth eased and is forecast to remain broadly stable.

- Companies reported easing cost and price inflation but expect input cost pressures to strengthen over the coming year.

- Capital investment held firm, while R&D spending continued to lag historical trends and the UK average.

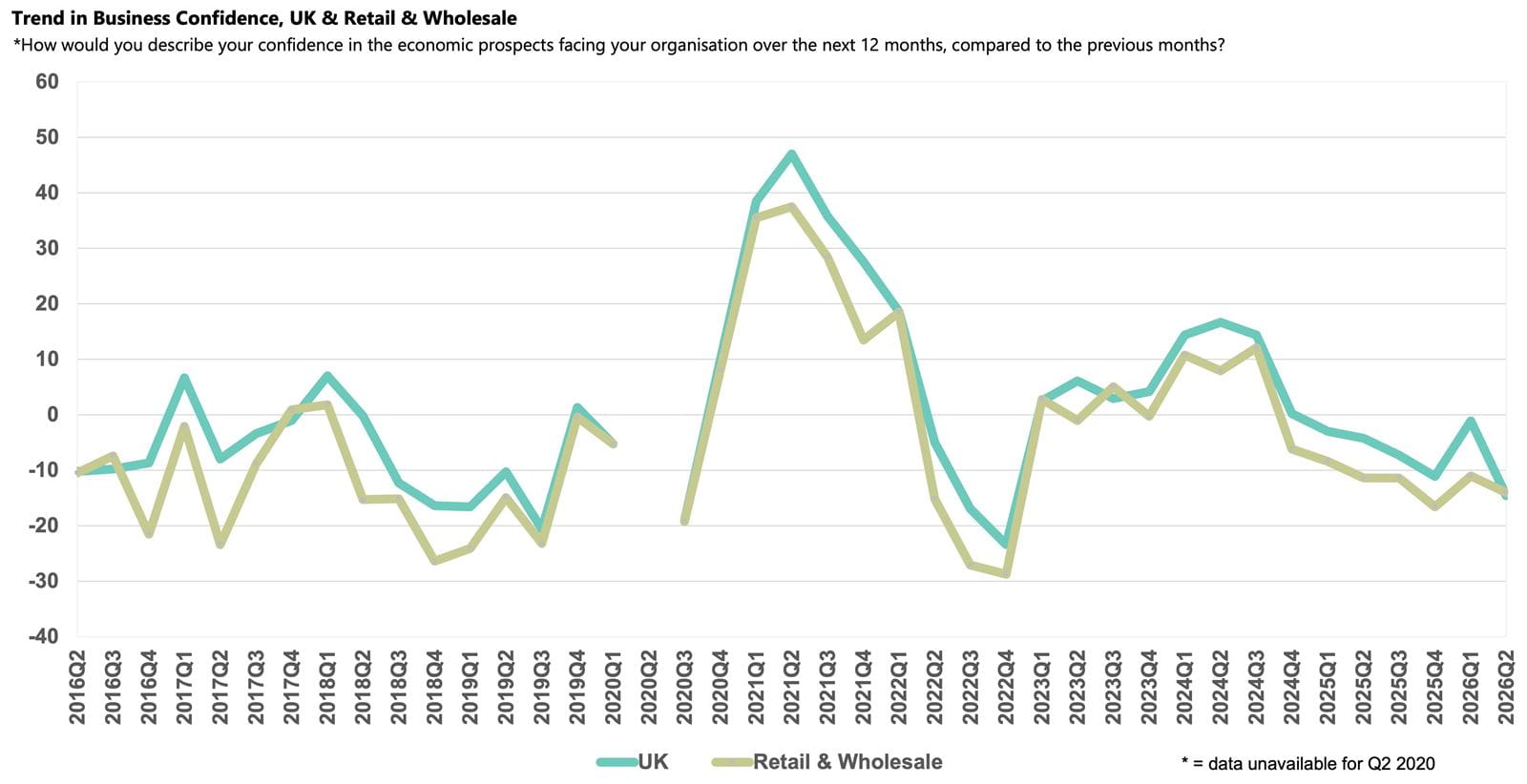

Business confidence in the Retail & Wholesale sector

Sentiment in the Retail and Wholesale sector fell further into negative territory in Q2 2026, dropping from -11.0 in the previous quarter, to -14.0, and widening the gap to the sector’s historical average (-0.7), but broadly comparable to the national average (-14.6).

Geopolitical tensions in the Middle East dampened confidence and performance across Retail & Wholesale businesses this quarter. The latest ONS data show that retail sales volumes continue to be volatile and, following a marked 1.0% m/m decline in April, sales bounced back by 1.2% in May. However, the Bank of England Agents’ summary of business conditions for June 2026 stated that while consumer spending volumes continued to grow, the growth was largely underpinned by uplifts in inflation rather than improving demand. Contacts are also increasingly concerned that higher energy costs and the erosion of real household incomes will further weaken demand, while BCM shows that alongside geopolitical risk, labour costs and taxation remain prominent challenges.

Domestic sales growth and customer demand

Retail & Wholesale companies reported that annual domestic sales growth was unchanged at 3.6% from the previous quarter, matching the national average rate, and remaining ahead of the sector’s historical average (2.9%). While developments in the Middle East will likely shape prospects, businesses in the sector expect growth will improve over the coming year, rising to 4.6%, broadly tracking the UK projection (4.7%).

Customer demand concerns remain significant in Retail & Wholesale. The issue was cited as a rising challenge by 42% of businesses in the sector, down from 47% recorded last quarter, but comparable with both the sector's historical norm (44%) and the national average (40%).

Business challenges

With the Iran War ongoing through much of the survey period, geopolitical risk was cited as a rising challenge by 68% of Retail & Wholesale businesses. Newly added to the survey this quarter (Q2 2026), this concern was more widely cited than the national average (65%). The closure of the Strait of Hormuz also drove a sharp rise in oil and gas prices, prompting 51% of businesses in the sector to report energy costs as a growing challenge, compared to the UK average of 55%. Meanwhile, disruption to supply chains meant the share of Retail & Wholesale businesses reporting transport problems rose from 12% in the previous quarter to 26% in Q2 2026, exceeding the sector’s historical norm of 20%.

The sector’s comparatively large dependence on typically lower-paid and entry-level workers meant Retail & Wholesale companies have been more exposed to the National Living Wage uplifts in recent years and higher employer National Insurance Contributions. As a result, labour costs continue to be widely cited as a rising challenge, with 63% of businesses in the Retail & Wholesale sector reporting the issue, above the national average (58%).

There is a variety of other prevalent challenges among businesses in the Retail & Wholesale sector. The tax burden was cited as a rising challenge by 47% of companies, down from 61% in Q1 2026 but still marginally ahead of the national average (45%), while the proportion citing competition in the marketplace increased to 44% in Q2 2026, above both the sector’s historical norm (40%) and the UK average (38%).

Labour market

BCM indicates that Retail & Wholesale businesses continue to expand headcount following a period of contraction at the end of 2025. Annual employment growth in the Retail & Wholesale sector rose for the third consecutive quarter in Q2 2026, rising from 0.6% in the previous quarter, to 1.2%. This uplift was marginally below the 1.4% national rate but notably above the above the sector's historical norm (0.8%). Businesses expect growth will continue at the same pace over the next 12 months, lower than the UK projection (1.5%).

Annual wage growth in the Retail & Wholesale sector slowed in Q2 2026 to 2.4%, recording the weakest rate since Q4 2021 and closer to the historical norm (2.0%). This increase was the softest of any sector in the economy, below the 3.1% rise recorded nationally. However, companies expect salary inflation to hold relatively steady over the next 12 months, at 2.5%, compared with the 2.7% rise forecast nationally.

Input and selling prices, and profits growth

While most sectors reported rising input price inflation this quarter, the Retail and Wholesale sector reported that it eased to 2.9% from 3.9% last quarter, notably below the 4.1% rise observed across the UK. However, businesses expect cost rises to start to feed through over the coming year and, along with Manufacturing & Engineering, are the only sector forecasting an uptick in input cost inflation over the next 12 months. While their prediction of 3.1% is higher than the historical norm (2.7%), it is notably below the UK projection (3.8%).

With input cost rises yet to feed through, companies in the Retail & Wholesale sector reported softer annual selling price growth in Q2 2026, at 2.3%, down from 2.7% in the previous quarter and marginally below the 2.5% national rate. Businesses expect broadly steady growth over the next 12 months, projecting 2.2%, compared with the 2.4% rise forecast nationally, and above the historical norm (1.6%).

Businesses in the Retail & Wholesale sector reported stronger annual profits growth in Q2 2026, at 3.5%, up from 3.1% in the previous quarter and above the 2.8% rate recorded nationally. Companies anticipate a further modest pick-up in growth in the year ahead and are optimistic that they will increase the growth premium over the sector's historical norm (2.4%), with a projected expansion of 4.2%, though this is weaker than the 4.7% rise expected nationally.

Investment

Annual capital investment growth in the Retail & Wholesale sector increased slightly to 2.0% in Q2 2026 and remains about the historical sector norm (1.7%). While this is lower than the 2.7% rate recorded nationally, businesses in the sector plan to maintain growth at the same pace over the coming year, exceeding the 1.8% rise anticipated across the UK.

R&D budget growth is somewhat subdued, rising by just 0.8% in the year to Q2 2026, lagging the historical norm (1.4%) and the UK average (2.0%). Companies intend to keep growth at a similar pace over the year ahead, with a forecast rise of 0.9%, half the pace of the UK forecast (1.8%)..