This consultation is likely to be of interest to all ICAEW members, ICAEW member firms and regulated firms, accountancy and legal sector regulators and ICAEW's oversight regulators.

Please respond using the online form or post your response to ICAEW Regulatory Practice and Policy Team. Details are provided under the section: Responding to the consultation.

Purpose of the consultation

We are committed to ensuring our decisions are appropriate, proportionate and evidence-based. The purpose of this consultation is to provide an opportunity to consider the proposed changes to the wording of ICAEW provisions under the fundamental principle of professional behaviour in sub-section 115.1 A2 of the ICAEW Code of Ethics (ICAEW Code).

We use consultations to ensure that we consider the views and experiences of all our stakeholders. There are eight questions for you to consider, and we also welcome your general comments on any aspect of the proposed changes.

Background

Our role as an improvement regulator is to strengthen trust in ICAEW Chartered Accountants and firms. We do this by enabling, evaluating, and enforcing the highest standards of ethical behaviour in the profession.

Professional accountants are expected to demonstrate the highest standards of professional behaviour. They must uphold values of integrity, objectivity, professional competence and due care, confidentiality, and professional behaviour. This is because they play a key role in ensuring public trust in financial reporting and business practices and maintaining the reputation of the accountancy profession.

The current version of the ICAEW Code has been in place since 1 January 2020. It sets out the fundamental principles of ethical behaviour expected of all professional accountants and reflects the profession's duty to act in the public interest. It does this by defining our values, and the standards of behaviour expected of those who represent it. The ICAEW Code applies to all professional and business activities, whether remunerated or voluntary.

There are five fundamental ethical principles which guide behaviour:

- Integrity

- Objectivity

- Competence

- Confidentiality

- Professional behaviour

These principles set out the standard of behaviour expected of a professional accountant. Members are responsible for assessing threats to complying with these principles and for implementing safeguards where threats are significant.

Professional accountants are accountable for their actions and failure to follow the ICAEW Code may result in a member becoming subject to disciplinary action.

Professional behaviour

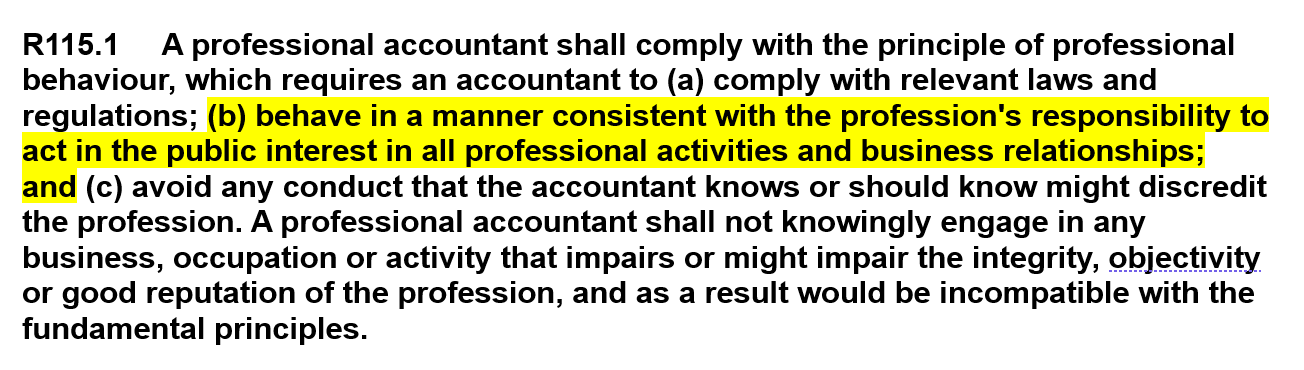

The fifth ethical principle sets out that professional accountants should 'comply with relevant laws and regulations and avoid any conduct that the professional accountant knows or should know might discredit the profession.'

It includes the following provisions:

| R115.1 | A professional accountant shall comply with the principle of professional behaviour, which requires an accountant to comply with relevant laws and regulations and avoid any conduct that the accountant knows or should know might discredit the profession. A professional accountant shall not knowingly engage in any business, occupation or activity that impairs or might impair the integrity, objectivity or good reputation of the profession, and as a result would be incompatible with the fundamental principles. |

| 115.1 A1 | Conduct that might discredit the profession includes conduct that a reasonable and informed third party would be likely to conclude adversely affects the good reputation of the profession. |

| 115.1 A2 | The concept of professional behaviour implies that it is appropriate for professional accountants to conduct themselves with courtesy and consideration towards all with whom they come into contact when performing their work. |

IESBA

As a member of the International Federation of Accountants (IFAC), ICAEW adopts the International Code of Ethics for Professional Accountants published by the International Ethics Standards Board for Accountants (IESBA). There is also ICAEW add-on material which provides additional requirements and guidance for UK-specific issues.

We are obliged to adopt the IESBA Code in full and are not permitted to change its provisions, only add to them. However, sub-section 115.1 A2 is ICAEW add-on material and therefore we can change or add to this material if we consider changes are required.

In addition to the changes we are considering to sub-section 115.A2, IESBA itself has already identified, within its project looking at the 'Role and Mindset of Professional Accountants', the need for changes to the Code, including a change to the fundamental principle of professional behaviour. The change from the IESBA project is to include some additional text to R115.1 as highlighted below:

This additional text will be incorporated into the ICAEW Code as part of the next update, likely to take place in the second quarter of 2024.

While the new specific reference to acting in the public interest may be welcomed, we do not believe that it assists with the interpretation of what are appropriate or inappropriate behaviours of members, either within the workplace or outside of the workplace. The change is a general statement that does not reference any specific types of behaviour. We therefore consider that further changes are required in addition to the IESBA change to R115.1.

Proposed ICAEW amendments

The proposed amendments to the provisions under the fifth fundamental ethical principle, professional behaviour, are as follows:

Current wording

115.1 A2 The concept of professional behaviour implies that it is appropriate for professional accountants to conduct themselves with courtesy and consideration towards all with whom they come into contact when performing their work.

Proposed new wording

115.1 A2 The concept of professional behaviour implies that professional accountants should act in accordance with the standards that society expects in all professional and business relationships. For example, professional accountants should treat others fairly, and with respect, and not harass, bully, or unfairly discriminate against them.

Purpose of the proposed changes

Our proposed changes are intended to update and strengthen the principle of professional behaviour and clarify the standards of behaviour that are expected of a professional accountant.

We consider that they will achieve the following benefits in the public interest to:

- encourage high standards of ethical behaviour;

- strengthen trust in Chartered Accountants;

- promote a more inclusive Chartered Accountancy profession;

- protect the health and wellbeing of the Chartered Accountancy profession; and

- clarify the circumstances in which a member may be liable to disciplinary action.

We want to make it clear to those subject to the ICAEW Code that they must treat all those they encounter in professional and business relationships fairly, with respect, and not harass, bully, or unfairly discriminate against them. This is because:

- unfair or inappropriate treatment can affect the health and wellbeing of colleagues and impact on their ability to practise. This in turn can also have an impact on the quality of services received by consumers;

- unfair or inappropriate treatment can also mean that those who may not be competent are put in positions of responsibility, rather than being appointed on merit;

- incidences of bullying behaviour in the workplace or related environments can influence ethical behaviour. For instance, it could lead to covering up mistakes or acts of dishonesty, rather than being open and transparent; and

- unwelcome and inappropriate conduct by colleagues in professional or work-related environments or on social media is highly damaging to victims, the profession, and its reputation.

By making our expectations around professional behaviour clear, we hope that this will also help others to raise concerns about unethical behaviour or identify inappropriate practices. This will allow us to take appropriate action, if necessary, when we receive complaints or otherwise become aware of the conduct.

Q1. Do you agree with the proposed amendment to sub-section 115.1 A2? Please explain the reasons for your answer.

Rationale

'The standards that society expects'

In defining our expectations of the professional standards of our members (and all who are subject to the ICAEW Code), we have carefully considered how we can ensure the standards achieve appropriate outcomes. We propose to replace the existing reference to 'courtesy and consideration' with the broader concept of the 'standards that society expects'.

Courtesy and consideration are important values for professional accountants. However, they are narrow concepts that do not capture all the types of behaviour we consider are important for Chartered Accountants.

Defining standards of ethical behaviour with reference to the shared social norms that members of a society understand and accept, provides increased flexibility and clarity. It emphasises that professional behaviour must meet the objective expectations of a professional member of society. This also allows for prevailing societal attitudes to be considered, both over time and with reference to the location an individual lives and works in.

The concept of the standards that society expects is intended to encourage members to use their professional judgement to reflect on how they should be behaving. In terms of disciplining poor conduct, it allows our Conduct Committee and Disciplinary Tribunals to apply their judgement on whether a member's conduct is sufficiently far from the standards that society would expect of a professional. Rather than focusing on the narrower concept of courtesy and consideration.

Q2. Do you agree with the inclusion of the concept 'the standards that society expects'? Please provide any additional comments or details of concerns.

'In all professional and business relationships'

We want to clarify the circumstances and situations in which members, and all who are subject to the ICAEW Code, need to be cognisant of their professional behaviour. The existing wording of 'in all whom they come into contact when performing their work' could imply that high standards of professional behaviour are only required when directly performing client work. However, the ICAEW Codes applies in all aspects of a member's professional life.

The wording 'professional and business relationships' is intended to explain that a member's conduct in broader contexts such as work-related events, or on social media, is relevant to their professional body, as well as in the workplace. The term 'professional and business relationships' does, however, place a boundary by not straying into matters wholly in a member's private life.

It is important to note however that conduct of a criminal nature would always be of disciplinary interest to ICAEW as a professional body, and the ICAEW Code requires members to comply with all relevant laws and regulations. This is the case whether the conduct is wholly in a member's private life, or not.

Clarifying the scope of the professional behaviour provisions in the ICAEW Code will ensure it highlights the types of poor behaviour that should be reported to our Conduct Department. This will also bring our rules on professional conduct in closer alignment to those imposed by other regulators (see Appendix). This sends a clear message that poor professional conduct is not acceptable in any forum, without straying too far into a member's private life.

Q3. Do you agree with the proposed scope of 'professional and business relationships'? Please provide any additional comments or details of concerns.

Q4. Do you have any comments on the wording or any suggested amendments? Please provide any additional comments or details of concerns.

'For example, professional accountants should treat others fairly, and with respect, and not harass, bully, or unfairly discriminate against them'

Professional accountants have an important role in promoting an ethical culture. We want to ensure that professional accountants clearly understand the expectations that come with their professional role.

The proposed inclusion of examples in the Code aims to explain what the expectations are in terms of professional behaviour by ICAEW members and others subject to the ICAEW Code. This wording also covers many of the types of poor behaviour that are reported to ICAEW's Conduct Department. However, while the list of examples is intended to highlight some relevant types of inappropriate behaviour, it is not overly prescriptive or exhaustive. This means that ICAEW can address seriously poor conduct of any kind that takes place in a professional or business context and ensure consistency in regulatory and disciplinary outcomes.

As part of the implementation of the proposed changes to sub-section 115.1 A2, further guidance or definitions would be provided for the examples of behaviour listed above.

Q5. Do you think the examples sufficiently capture the types of behaviour and concerns relevant to a modern profession? Please explain why.

Q6. Do you have any suggested changes to the list of proposed examples?

Impact analysis

Regulatory impact

We do not consider that these proposals will impose significant further costs or have an onerous regulatory impact on members or firms.

By being clear about the standards of behaviour that are expected of Chartered Accountants we will promote further transparency and consistency in member conduct.

This change may encourage new self-reports and complaints to be submitted. We act in the public interest, and it is part of our role to ensure our members and member firms act with integrity and to the highest standards. We will consider all complaints in accordance with our disciplinary processes.

Some firms may have to introduce new policies and procedures to ensure colleagues are aware of our expectations. However, it is our view that firms should already be taking reasonable steps to ensure that colleagues are treated fairly. If this is not the case, then our rules will encourage these firms to take active steps to prevent unfair and inappropriate conduct.

Equality and diversity impact assessment

We do not consider that these proposals will result in a negative or disproportionate impact on protected groups or on diversity and inclusion, but consultees may have different insights.

The changes clarify the behaviour we all expect as members of society to promote and support equality, diversity, and inclusion in practice. Stating our expectations about treating others fairly and with respect provides a clear message about our shared values as a profession. This should have the positive effect of fostering an inclusive and diverse profession.

We will consider any consultation feedback relating to diversity and inclusion impacts and will continue to monitor and respond to any emerging impacts.

Q7. Do you feel that the proposed changes outlined in this consultation could have an impact on matters relating to equality, diversity or inclusion? If so, please provide any additional comments or details of concerns.

Q8. Do you have any other general comments on the proposed changes to the ICAEW Code of Ethics provisions on professional behaviour?

Consultation questions summary

-

Click to see the full list of eight questions for this consultation

Q1. Do you agree with the proposed amendment to sub-section 115.1 A2? Please explain the reasons for your answer.

Q2. Do you agree with the inclusion of the concept 'the standards that society expects'? Please provide any additional comments or details of concerns.

Q3. Do you agree with the proposed scope of 'professional and business relationships'? Please provide any additional comments or details of concerns.

Q4. Do you have any comments on the wording or any suggested amendments? Please provide any additional comments or details of concerns.

Q5. Do you think the examples sufficiently capture the types of behaviour and concerns relevant to a modern profession? Please explain why.

Q6. Do you have any suggested changes to the list of proposed examples?

Q7. Do you feel that the proposed changes outlined in this consultation could have an impact on matters relating to equality, diversity or inclusion? If so, please provide any additional comments or details of concerns.

Q8. Do you have any other general comments on the proposed changes to the ICAEW Code of Ethics provisions on professional behaviour?

Responding to the consultation

Consultation closed 9 February 2024

You can respond to the consultation by completing the online form.

Or post your response to ICAEW Regulatory Practice and Policy Team, Professional Standards Department, Metropolitan House, Avebury Boulevard, Milton Keynes MK9 3FS.

Next steps

Once the consultation closes, we will analyse the responses. They will be considered before deciding on our next steps. Any proposed changes to the ICAEW Code will be put to ICAEW Council for approval.

If responses are published and/or specific feedback is referenced following this consultation, we will not attribute any comments to individuals nor identify individual respondents. Responses are kept anonymous.

Governance requirements

ICAEW Council is the body with responsibility to approve changes to the ICAEW Code, with detailed responsibility delegated to the Ethics Standards Committee. ICAEW's oversight regulators may also need to consider and approve any changes to our regulatory arrangements in advance of such changes coming into effect.

Appendix

Professional behaviour: approach in other professions

-

General Medical Council (GMC)

(Excerpt)

Doctors' use of social mediaExtract: 1

1

In Good medical practice1 we say:36. You must treat colleagues fairly and with respect.

65. You must make sure that your conduct justifies your patients' trust in you and the public's trust in the profession.

69. When communicating publicly, including speaking to or writing in the media, you must maintain patient confidentiality. You should remember when using social media that communications intended for friends or family may become more widely available.

70. When advertising your services, you must make sure the information you publish is factual and can be checked, and does not exploit patients' vulnerability or lack of medical knowledge.

Extract: 2

5. The standards expected of doctors do not change because they are communicating through social media rather than face to face or through other traditional media. However, using social media creates new circumstances in which the established principles apply.

Extract: 3

Respect for colleagues

15. Good medical practice says that doctors must treat colleagues fairly and with respect7. This covers all situations and all forms of interaction and communication. You must not bully, harass or make gratuitous, unsubstantiated or unsustainable comments about individuals online.

16. When interacting with or commenting about individuals or organisations online, you should be aware that postings online are subject to the same laws of copyright and defamation8 as written or verbal communications, whether they are made in a personal or professional capacity9.

Endnotes

1 General Medical Council (2013) Good medical practice London, GMC.

7 General Medical Council (2013) Good medical practice London, GMC, paragraph 36.

8 Defamation is the act of making an unjustified statement about a person or organisation that is considered to harm their reputation.

9 [2008] EWHC 1781 (QB).

-

Solicitors Regulation Authority (SRA)

(Excerpt)

Code of Conduct for Solicitors, RELs and RFLs1: Maintaining trust and acting fairly

1.1 You do not unfairly discriminate by allowing your personal views to affect your professional relationships and the way in which you provide your services.

1.2 You do not abuse your position by taking unfair advantage of clients or others.

1.3 You perform all undertakings given by you, and do so within an agreed timescale or if no timescale has been agreed then within a reasonable amount of time.

1.4 You do not mislead or attempt to mislead your clients, the court or others, either by your own acts or omissions or allowing or being complicit in the acts or omissions of others (including your client).

1.5 You treat colleagues fairly and with respect. You do not bully or harass them or discriminate unfairly against them. If you are a manager, you challenge behaviour that does not meet this standard.

-

Chartered Management Institute (CMI)

(Excerpt)

Code of Conduct and PracticeCreating a positive impact on society

- Treating others fairly and with respect, promoting equality of opportunity, diversity and inclusion, and supporting human rights and dignity.

- Addressing the interests and needs of all stakeholders in a balanced manner.

- Ensuring that the environmental impact of your work is as positive as possible.

- Challenging and reporting conduct or behaviour which you suspect to be unlawful or unethical, and encouraging others to do so.

- Recognising and valuing the responsibilities you have to the communities in which you operate.

- Exhibiting personal leadership as a role model for maintaining the highest standards.

Respecting the people with whom you work

- Taking all necessary steps to ensure that individuals are not subjected to harassment, sexual harassment or bullying.

- Supporting colleagues to understand fully their responsibilities, areas of authority and accountability.

- Encouraging and assisting colleagues to develop their skills and progress their careers, valuing the contribution which they make, and recognising their achievements.

- Promoting, enhancing, sharing and encouraging best management practice.

- Acting consistently and fairly when addressing personal performance or standards of behaviour.

- Having regard for the physical and mental health, safety and wellbeing of colleagues, recognising their specific needs and the pressures and problems they face.

- Demonstrating respect in all interactions, whether face-to-face or virtually.

-

Chartered Institute of Legal Executives (CILEx)

(Excerpt)

Code of ConductCore Principles

You must adhere to the following core principles in the work you do and the decisions you make. The principles also help the public to know the standards of behaviour that are expected of you.

You must:

- Uphold the rule of law and the impartial administration of justice.

- Maintain high standards of professional and personal conduct and justify public trust in you, your profession and the provision of legal services.

- Behave with honesty and integrity.

- Comply with your legal and regulatory obligations and deal with your regulators and ombudsmen openly, promptly and co-operatively.

- Act competently in the best interests of your client and respect client confidentiality.

- Treat everyone fairly and without prejudice.

- Ensure your independence is not compromised.

- Act effectively and in accordance with proper governance and sound financial and risk management principles.

- Protect client money and assets.

-

Nursing and Midwifery Council (NMC)

(Excerpt)

The CodePromote professionalism and trust

- You uphold the reputation of your profession at all times.

- You should display a personal commitment to the standards of practice and behaviour set out in the Code.

- You should be a model of integrity and leadership for others to aspire to.

- This should lead to trust and confidence in the professions from patients, people receiving care, other health and care professionals and the public.

20. Uphold the reputation of your profession at all times

To achieve this, you must:

20.1 keep to and uphold the standards and values set out in the Code

20.2 act with honesty and integrity at all times, treating people fairly and without discrimination, bullying or harassment

20.3 be aware at all times of how your behaviour can affect and influence the behaviour of other people

20.4 keep to the laws of the country in which you are practising

20.5 treat people in a way that does not take advantage of their vulnerability or cause them upset or distress

20.6 stay objective and have clear professional boundaries at all times with people in your care (including those who have been in your care in the past), their families and carers

Professional standards of practice and behaviour for nurses, midwives and nursing associates.

All standards apply within your professional scope of practice.

20.7 make sure you do not express your personal beliefs (including political, religious or moral beliefs) to people in an inappropriate way

20.8 act as a role model of professional behaviour for students and newly qualified nurses, midwives and nursing associates to aspire to

20.9 maintain the level of health you need to carry out your professional role

20.10 use all forms of spoken, written and digital communication (including social media and networking sites) responsibly, respecting the right to privacy of others at all times.

-

Headteachers' standards 2020

(Excerpt)

Section 1: Ethics and professional conductAs leaders of their school community and profession, headteachers:

- serve in the best interests of the school's pupils

- conduct themselves in a manner compatible with their influential position in society by behaving ethically, fulfilling their professional responsibilities and modelling the behaviour of a good citizen

- uphold their obligation to give account and accept responsibility

- know, understand, and act within the statutory frameworks which set out their professional duties and responsibilities

- take responsibility for their own continued professional development, engaging critically with educational research

- make a positive contribution to the wider education system.

-

Police Code of Ethics

(Excerpt)

Code of Ethics2 Authority, respect and courtesy:

2.1

According to this standard you must:- carry out your role and responsibilities in an efficient, diligent and professional manner

- avoid any behaviour that might impair your effectiveness or damage either your own reputation or that of policing

- ensure your behaviour and language could not reasonably be perceived to be abusive, oppressive, harassing, bullying, victimising or offensive by the public or your policing colleagues