Q2: Business confidence in the West Midlands deteriorates as the Iran War weighs on the outlook.

The latest national Business Confidence Monitor (BCM) shows that the Iran War significantly dented confidence as it dropped to a near four-year low and suffered its sixth successive negative quarterly score. Companies reported rising costs pressures, weaker expected sales and profits growth for the coming year, while late payment concerns hit a five-year high.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 13 April to 19 June 2026.

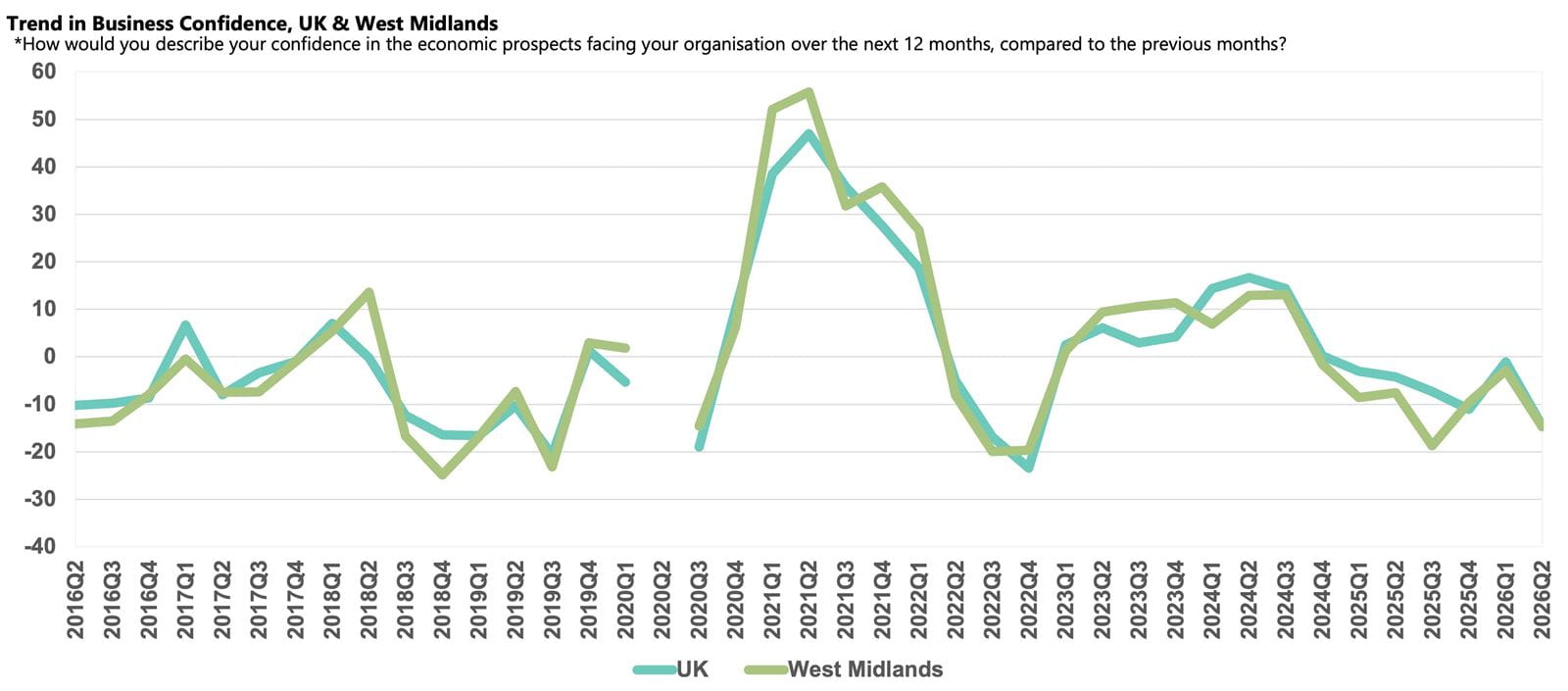

- Business confidence in the West Midlands fell to -14.7 from -2.9 in Q1 2026, broadly in line with the UK average (-14.6).

- Annual domestic sales growth strengthened, while exports growth slowed, with companies forecasting lower exports growth than the UK average next year.

- Geopolitical risk was the most widely cited rising challenge, followed by energy costs.

- Wage growth continues to ease but remains above the historical norm, with businesses expecting salaries to rise at the same rate over the next 12 months.

- Input costs are expected to rise more quickly next year, with companies also intending to increase their selling prices at a faster rate.

- Businesses plan to reduce the rate they expand both capital investment and R&D budgets over the next 12 months.

Business confidence in West Midlands

Business sentiment in the West Midlands fell sharply in Q2 2026, with the Business Confidence Index dropping from -2.9 in Q1 2026 to -14.7, closely matching the UK average score (-14.6) but again falling short of the regional historical average (+3.9).

As a heavily manufacturing and export dependent region, the increase in global uncertainty and disruption caused by events in the Middle East adversely impacted confidence and business performance in the West Midlands in Q2 2026. The disruption added to the existing tariff uncertainties already weighing on exporters. While the month of May saw a welcome rise in UK vehicle production, according to the Society of Motor Manufacturers and Traders (SMMT), vehicle production at the end of the five-month period to May 2026 was down 8.7% on the same period in 2025. Growing political uncertainty following May’s local elections may also have fed into business sentiment in the region.

Domestic sales and exports growth

Businesses in the West Midlands reported stronger annual domestic sales growth in Q2 2026, at 3.6%, maintaining growth above the historical norm (3.1%) and matching the increase recorded across the UK. Companies anticipate an uplift over the next 12 months, projecting a 4.6% rise, broadly in line with the 4.7% rise forecast nationally.

The increase in global uncertainty since the outbreak of the war in Iran has negatively impacted exports sales in the region. Companies reported that annual exports growth slowed to 1.4% in Q2 2026, far below the region’s historical norm (2.5%) and less than half the 3.1% rate recorded nationally. While businesses in the region expect an uplift in growth, the anticipated annual increase of 3.3% is lower than the UK forecast rate (4.0%).

Business challenges

With the Iran War ongoing through much of the survey period, geopolitical risk was cited as a rising challenge by 71% of businesses in the West Midlands. Newly added to the survey this quarter (Q2 2026), this concern was more widely reported than the national average (65%). The sharp rise in oil and gas prices prompted 61% of businesses in the region to register energy prices as a growing challenge, also exceeding the national average (55%). The higher incidence of these challenges in the West Midlands is likely linked to the large concentration of Manufacturing & Engineering businesses and exporters located in the region.

Meanwhile, domestic challenges remain considerable for businesses in the region. Labour costs were reported as a rising challenge by 58% of businesses in the West Midlands, matching the national average (58%), while customer demand was cited by 45% of businesses in the region. This proportion exceeded both the region's historical norm (39%) and the national average (40%). Regulatory challenges, while easing, were reported by 41% of companies with the issue remaining more prominent than the regional norm (38%).

Labour market

Employment rose by 1.6% in the year to Q2 2026 in the West Midlands, marginally ahead of both the 1.4% national rate and the region’s historical norm (1.0%). However, amid heightened uncertainty businesses plan to moderate growth slightly to 1.4% over the next 12 months, broadly in line with the UK projection (1.5%).

Companies in the West Midlands recorded the softest annual wage growth of any region in the year to Q2 2026, at 2.3%. The rate of salary growth has been easing across recent quarters though it remains marginally above the region’s historical norm (2.1%). Businesses predict they will increase salaries at the same pace over the next 12 months, lower than the 2.7% rise forecast nationally.

Input and selling prices, and profits growth

Annual input price inflation in the West Midlands picked up slightly to 3.5% in Q2 2026, though the uplift was less severe than the 4.1% rate recorded nationally. However, companies expect a further rise to reach 3.9% over the next 12 months, widening the gap to the region’s historical norm (2.9%) and just ahead of the UK forecast (3.8%).

Businesses in the region reported that they increased their selling prices growth to 2.8% in Q2 2026. This uplift outpaced both the UK average (2.5%) and the regional historical norm (1.6%), suggesting that businesses in the region passed on a larger proportion of the rise in their input costs onto customers than some regions. With cost pressures expected to continue to build, businesses anticipate a further marked uplift in their selling prices over the coming year, with a projected rise of 3.2%.

Subdued exports growth and rising input costs eroded profits growth in the year to Q2 2026, which slowed to 1.9%. This increase was among the weakest increases in the UK, lagging the national growth rate of 2.8%. However, companies forecast a marked uplift over the coming year, with growth expected to climb above the 2.8% historical norm and reach 4.6%, broadly tracking the 4.7% rise predicted for the UK.

Capitial investment and R&D

Companies in the West Midlands reported stronger annual capital investment growth in Q2 2026, at 3.3%, outpacing the nationwide average (2.7%). However, increased global uncertainty has affected the appetite for capital investment in the West Midlands, and businesses plan to slow growth to just 1.5% over the next 12 months, lagging both the region’s historical norm (1.9%) and the 1.8% expected across the UK.

Annual R&D budget growth in the West Midlands was 2.5% in Q2 2026, unchanged from the previous quarter and still ahead of the 2.0% rate recorded nationally. Companies intend to slow growth over the next 12 months to 1.7%, slightly lower than both the national average projection and the region's historical norm (both 1.8%).