The ethics advisory team has developed this Decision Tree to help members resolve ethical issues as they arise. It should be used in conjunction with the ICAEW’s Code of Ethics.

Introduction

This helpsheet has been issued by ICAEW’s Technical Advisory Service to help ICAEW members resolve ethical problems they may face.

Members may also wish to refer to the following related guidance:

Framework

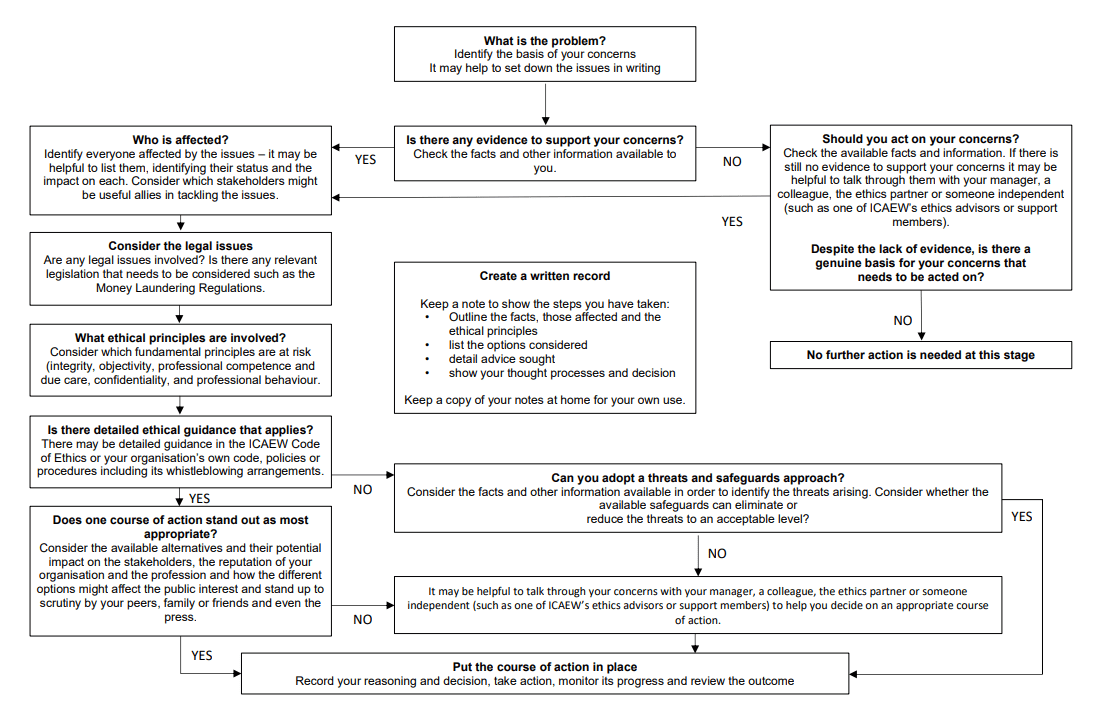

When trying to resolve an ethical problem you may find it useful to consider the following questions and flowchart for resolving ethical problems.

Gather the relevant facts and identify the problems

- Do I have all the facts relevant to the situation?

- If it’s not possible to obtain all relevant facts you may be able to obtain more background information by referring to the organisation’s policy, procedures, code of conduct and previous history and/or discussion the matter with trusted managers and colleagues.

- What assumptions am I currently making? Are these reasonable and could I support these with additional facts and/or evidence?

- Do I have primary responsibility for this issue or could I seek guidance from someone else?

Identify the relevant parties

- Who are the individuals, organisations and other key stakeholders affected?

- How are these stakeholders affected? Are there financial as well as ethical implications?

- Are there conflicts between these stakeholders?

- Which stakeholders are likely to sit on which side of the issue? Are any of the stakeholders likely to be an ally?

Consider the ethical issues involved

- What are the professional, organisational and personal ethics issues?

- Have you referred to ICAEW Code of Ethics and documented which sections might contain relevant guidance?

- Would these ethical issues affect the reputation of the accountancy profession?

- Would these ethical issues affect the public interest?

Identify which fundamental principles are affected and the threats to them

Section 110 of the ICAEW Code of Ethics outlines the fundamental principles. Which of these fundamental principles are affected?

- Integrity

- Objectivity

- Professional competence and due care

- Confidentiality

- Professional behaviour

Paragraph 120.6 A3 of the ICAEW Code of Ethics outlines the types of threats to the fundamental principles.What are the threats to compliance with the fundamental principles?

- Self interest

- Self-review

- Advocacy

- Familiarity

- Intimidation

Are the threats to compliance with the fundamental principles clearly insignificant? If not, are there safeguards which can eliminate or reduce the threats to an acceptable level?

Consider the employing organisation's internal procedures

- Do your organisation's policies and procedures provide guidance on the situation?

- How can you escalate concerns within the organisation? Who should be involved, in what role and at what stage? It may be useful to discuss with the following parties:

- Your immediate superior

- The next level of management

- A corporate governance body, for example the audit committee

- Other departments in the organisation which include, but are not limited to, legal, audit and human resources departments. - Does the organisation have a whistleblowing procedure?

- Would it be appropriate to refer to external sources of help such as the ICAEW Ethics Advisory Service?

Consider and evaluate alternative courses of action

You should consider:

- Your organisation's policies, procedures and guidelines

- Applicable laws and regulation

- Universal values and principles generally accepted by society

- Consequences

When evaluating the suggested course of action, you should test its adequacy by considering whether:

- All consequences associated with the course of action been discussed and evaluated?

- There is any reason why the suggested course of action will not stand the test of time?

- A similar course of action would be undertaken in a similar situation?

- The suggested course of action would stand scrutiny from peers, family and friends?

Implement the course of action and monitor its progress

When faced with an ethical issue, it is in your best interests to document your thought processes, discussions and the decisions taken. Written records will be useful if you need to justify your course of action in the future.

Below is a flowchart which can be used in conjunction with the questions above to aid in resolving an ethical problem.

Decision tree

If in doubt seek advice

ICAEW members, affiliates, ICAEW students and staff in eligible firms with member firm access can discuss their specific situation with the Ethics Advisory Service on +44 (0)1908 248 250 or via webchat.

© ICAEW 2026 All rights reserved.

ICAEW cannot accept responsibility for any person acting or refraining to act as a result of any material contained in this helpsheet. This helpsheet is designed to alert members to an important issue of general application. It is not intended to be a definitive statement covering all aspects but is a brief comment on a specific point.

ICAEW members have permission to use and reproduce this helpsheet on the following conditions:

- This permission is strictly limited to ICAEW members only who are using the helpsheet for guidance only.

- The helpsheet is to be reproduced for personal, non-commercial use only and is not for re-distribution.

For further details members are invited to telephone the Technical Advisory Service T +44 (0)1908 248250. The Technical Advisory Service comprises the technical enquiries, ethics advice, anti-money laundering and fraud helplines. For further details visit icaew.com/tas.

Download this helpsheet

PDF (250kb)

Access a PDF version of this helpsheet to print or save.

Download-

Update History

- 01 Aug 2014 (12: 00 AM BST)

- First published

- 03 Feb 2022 (03: 30 PM GMT)

- Changelog created, helpsheet converted to new template

- 03 Feb 2022 (03: 31 PM GMT)

- Change of links for referrals to CCAB guidance.